It’s been a week of record closes for Wall Street, with the VIX (or fear index) now under 11. This means the market doesn’t fear President Donald Trump’s dream policies. In fact, the love for his tax cuts, which he seems to be pushing ahead faster than most expected, really turbo-charged the love factor on Thursday in the USA and Friday’s trade here.

Overnight, materials, energy and financials led the way, while the safer, interest rate substitute stocks were friendless. This is the reflation trade or a ‘risk on’ situation and if you think this has nothing to do with Mr. Trump, then you have one eye and you’re not making money. A pullback will eventually come because this kick up is too big and too fast but if the US President keeps saying what the market calculates to mean higher profits and therefore share prices, then buying will keep on keeping on.

However, if Trump goes too hard on his protectionist measures, or the Congress pushes back on say the timing of the tax cuts, it would force short-termers to take profit. Of course, I will just say it is another buying opportunity for a market that has more time to run higher.

Why? Well, because the market positivity isn’t all Trump-created but he still has his influence over the other market-helping factors. First, the new US leader’s policies have taken away the expectation that growth is all in the hands of the Fed. Second, more economic growth is expected. And third, higher profits are on the cards.

On the current US reporting season, the growth in earnings is on track for a 7% rise, which a couple of quarters ago was said to have peaked. Now experts such as Thomas Lee of Fundstrat told CNBC that earnings are “mid-cycle”. This is good for someone like me, who thinks stocks can go higher over 2017 and 2018, at least!

I find my own views hard to believe with the Dow, S&P 500 and Nasdaq indexes at record highs but it leaves me with the expectation that the ride higher will have some bumpy moments. I’ll see these as buying opportunities if Donald Trump gets his way on most of his policies and his 20% import tax ends up being a smart Alec negotiating ploy from an experienced entrepreneur, who never really asks for what he really wants!

On the economy, higher energy prices should ensure inflation rises and higher Treasury yields this week say US interest rates will rise this year. However, the pace of these rises could be the bumpiness-creating factor for the stock market, which means the Fed is not totally on the sidelines.

On bumpiness ahead, Lee says his company did a study that showed that in the last four years the US stock market saw the fewest days in history when it was 3% off its market highs! That kind of thing can’t last, so bigger ups could bring bigger downs but as long as Trump policies are pro-market and they look like getting up, then we’re in bull territory.

At home, Trump’s tax titillation and the first real week of profit-reporting, which creamed that stock market optimism, is not misplaced. The S&P/ASX 200 Index rose 0.9% on Friday to be 1.8% higher, which was the best weekly showing for two months.

The big four banks were over 1% higher, which always helps the index,

Of course, not all earnings were rosy, with the likes of Genworth disappointing the market but the housing sector is starting to wobble. However, good earnings stories from the likes of Rio Tinto, CIMIC, AGL and Transurban gave solidity to optimists who believe in stocks right now.

Of course, when talking about the need for company tax cuts, the RBA Governor helped stocks as well. And the Prime Minister (having a good day in Parliament) giving it to Bill Shorten, might be a sign that Malcolm is getting back to his more aggressive roots, as his new and unimproved self has done nothing for his polling or business confidence in Canberra!

Resource stocks were softer for the week but Rio was a stand out, up 2.2%. A good profit report will do that.

What I liked

- The market’s reaction to President Trump’s reference to his ‘phenomenal tax plan’! ( This is a very unusual President and a very unusual stock market nowadays in the USA but the world is going along for the ride.)

- CommSec’s Craig James on the RBA boss: “The Reserve Bank Governor Philip Lowe has delivered his first speech of the year. And Governor Lowe has given his clearest message that interest rates have bottomed.”

- Dr. Phil, again, expects the economy to grow by around 3% over 2017 and 2018, while inflation will lift modestly.

- The Reserve Bank left the cash rate at a record low of 1.5%, maintaining its “neutral stance” – meaning rate hikes are as likely as rate cuts in the period ahead.

- Wall Street went to record highs after President Trump promised to provide details of tax reform over the next two to three weeks.

- New home sales rose by 0.2% in December, after lifting 6.1% from 27-month lows in November. Sales of ‘multi-units’ lifted 6% to 18-month highs. House sales fell 1.6%.

- Retail trade rose by 0.9% in the December quarter – above the decade-average growth pace of 0.7% and suggests that the December quarter growth rate was positive, especially when you throw in the trade surpluses in the quarter.

- Job advertisements rose by 4% in January to 167,164 ads – a five-year high. It was the strongest monthly rise in 2½ years. Job ads are up 7.1% on a year ago.

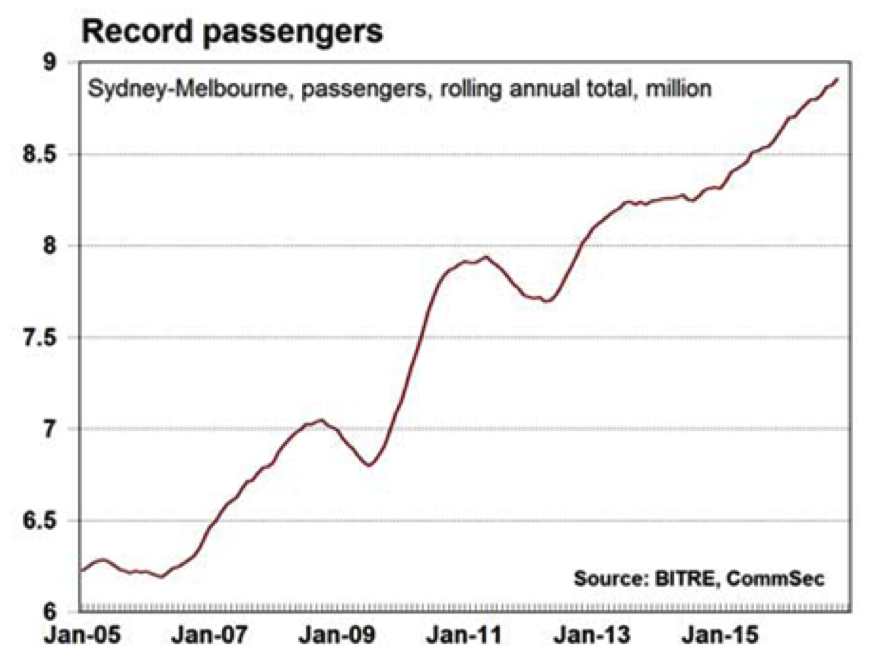

- In November, the number of passengers on the Sydney-Melbourne route was up by 4.2% on a year ago to a record 797,669 for the month. The Sydney-Melbourne route is also a key measure of business activity, CommSec says. On all domestic flights, passenger traffic rose 2.2% in November compared with a year ago but the number of flights fell so the smoothed load factor held at 4-year highs.

- Chinese exports and imports beat expectations, rising 5.9% and 25.2% respectively in the 12 months through January, which looks like a good pro-growth reading.

- The big number of stocks reporting this week but I’m a market nerd!

- Iron ore futures beat $US 100 late this week.

- Copper hit the highest price since May 2015, surging 4.6% to close at $US6090 a tonne and copper is a great omen indicator for world growth.

- The market support for the Switzer Dividend Growth Fund or SWTZ.

What I didn’t like

- Retail sales eased by 0.1% in December and was up 3% over the year.

- The ANZ/Roy Morgan consumer confidence rating fell by 0.5% to 117.5 in the week to February 5. (Confidence is up 5.7% over the year and well above the average of 113.2 since 2014.)

- European investors continue to watch carefully the developments in the lead up to the French presidential election, causing weakness in the financials sector.

- The Oz dollar at 76.72 US cents but a lot of analysts say we’ll go up before we fall in the second half of 2017. And that’s when the Fed will have to raise rates probably quicker than in the first half.

One big like

On Thursday this week, the Switzer family met a new Switzer – Theodore “Ted” William Switzer – who weighed in a tick under 4 kilos. As most of you know, I seldom gloss up the facts but he looks nothing short of perfect and I’m going long Big Ted!

Top stocks – how they fared

The week in review

- This week I explained why I’m expecting a great year for stocks!

- Paul Rickard outlined the performance of the Switzer Super Report income and growth portfolios in January.

- Tony Featherstone revealed two high-quality Australian retailers trading below their intrinsic value.

- Charlie Aitken explained why stocks like Microsoft, Amazon, IBM and Facebook are so attractive.

- The brokers upgraded Brambles and Suncorp this week, while the Commonwealth Bank was in the not-so-good books.

- In our second broker report, Oil Search was in the good books.

- The Super Stock Selectors liked NAB and Healthscope but Ardent Leisure was out of favour.

What moved the market?

- The RBA’s bullish commentary on the economy – are they riding the Trump train?

- Solid company earnings reports. Transurban Group and Rio Tinto were standouts.

- Donald Trump’s promise to reveal a “phenomenal” tax plan in the next few weeks.

Calls of the week

- Mad Malcolm’s tear down of Bill Shorten, calling him a “sycophant” and “parasite” during a heated Question Time this week. Is the new Malcolm here to stay?

- RBA Governor, Dr Philip Lowe, implied his support for the Government’s corporate tax cuts to keep Australia competitive.

- And in case you missed it, Tony Featherstone named two standout retailers in this week’s Switzer Super Report. Find out more.

The week ahead

Australia

- Monday February 13 – Tourist arrivals (December)

- Monday February 13 – Credit and debit card lending (December)

- Tuesday February 14 – Weekly consumer confidence

- Tuesday February 14 – Lending finance (December)

- Tuesday February 14 – NAB business survey (January)

- Wednesday February 15 – New vehicle sales (January)

- Wednesday February 15 – Consumer confidence (February)

- Thursday February 16 – Employment data (January)

Overseas

- Tuesday February 14 – US Producer prices (January)

- Tuesday February 14 – Federal Reserve Chair testimony

- Tuesday February 14 – China inflation data (January)

- Wednesday February 15 – US Consumer prices (January)

- Wednesday February 15 – US Retail sales (January)

- Wednesday February 15 – US Industrial production (January)

- Thursday February 16 – US Housing starts (January)

- Thursday February 16 – US Philadelphia Fed index (February)

- Friday February 17 – US Leading index (January)

Food for thought

“It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.” – Charles Darwin, natural scientist.

Last week’s TV roundup

- What can we expect from companies this reporting season? Peter Switzer and Charlie Aitken discuss on Super TV.

- Paul Rickard reveals some of the highlights from reporting season so far, and what he expects for the next few weeks.

- With the market’s optimism starting to give way to caution, how are ETFs trading in the Trump age? David Bassanese from BetaShares shares his views.

- And for a look at the big issues that could affect the local and global market, AMP’s Shane Oliver joins Super TV.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week the biggest mover was Western Areas with its short position increasing 1.42 percentage points to 13.11%. Monadelphous Group went the other way, decreasing by 1.78 percentage points to 8.00%.

Source: ASIC

Chart of the week

The amount of passengers flying the Sydney to Melbourne route in November was up by 4.2% on a year ago to a record 797,669. In the year to November, a record 8.91 million passengers were carried. As the route is a key measure of business activity, that’s a good sign for the economy!

Top five most clicked stories

- Peter Switzer: I’m seriously expecting a great year for stocks

- Tony Featherstone: 3 undervalued resource stocks

- Rudi Filapek-Vandyck: Buy, Sell, Hold – what the brokers say

- Bernadette Morabito: Hot stock tips: the banks and Healthscope

- Staff Reporter: Buy, Sell, Hold – what the brokers say

Recent Switzer Super Reports

- Thursday 9 February 2017: MAFIA stocks and Facebook’s report

- Monday 6 February 2017: Market outlook

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.