[table “256” not found /]

Wall Street might have done enough for now, with market news services citing French election fears starting to spook stock players. And let’s face it, the more short-term trader has to be thinking “is it time to take profit?” Banks in the US have lost their momentum and the bears look like they’re winning their battle with the bulls in the oil pit, with 200 rigs starting to pump the black stuff’s supply over the past 12 months.

One CNBC headline explained the slowdown in stock price rises and it went like this: “Border adjustment tax is on ‘life support’ and tax reform may come later… and with less punch.”

Remember, this rally has been premised on presidential promises and any adjustment to these by Congress, for example, could easily de-vibe the current market excitement. You can also throw in the fact that US market indices have been at record levels, with the Dow, S&P 500 as well as the Nasdaq beating their best levels five times in a row, which generally poses the question for many: “is it time to take profit?”

You could add a recent fall in metal prices to all this. And even talk about rising interest rates could worry a few players on Wall Street.

And then there’s the French election fear, which has seen bond prices fall. That happened in Greece, with Grexit and increases concerns about Frexit!

The current worry is that the left-wing groups might join together to KO the pro-market candidate, which could help the anti-Eurozone, right-winger Marine Le Pen.

Bloomberg describes it succinctly: “The campaign twist was bad news for French bondholders: polls suggest that a unified left bid would dent the chance of pro-market candidate Emmanuel Macron, the current front-runner, to advance to the May 7 decisive round. That would leave voters a choice between Le Pen and either Hamon or Melenchon, neither of whom is seen as market-friendly. It might also broaden support for the anti-euro, anti-immigration Le Pen.”

Locally, the Trump-inspired rally continued this week but it was helped by a pretty good week for earnings, spearheaded by the CBA’s one cent increase in its dividend. Of course, it was monetarily a mere bagatelle but it was the symbolic gesture that suggested that the bank doesn’t expect a capital event. It was this need for another capital raising that has hung over our banks, which held back share prices until Donald’s “let my banks go” play, as he promised to reduce financial regulations in the USA.

And by the way, it’s not all Trump. As I pointed out recently, there’s good economic growth happening in the USA, and China, Europe and Japan are growing better than expected in what is called the reflation trade. The US President is just adding a turbo charge to it all.

The S&P/ASX 200 index was up 1.5% for the week and I have to say I’m surprised. The market’s defiance of gravity is a little baffling. However, as a market optimist, generally, I’m happy when my stocks go higher. That said, a pullback driven by profit-takers shouldn’t be a surprise.

However, I’m not alone in being baffled by this irrepressible Trump rally.

“It looked a bit under pressure a couple of weeks ago,” said Michael Gable, the MD of Fairmont Equities. “The markets move around a lot – you can’t get too bullish after a long run.” (The Age)

Donald’s “phenomenal tax” powered up stocks early in the week and then CBA’s result kept the momentum going. And what I’m seeing tells me my 6000 and even my 6300 calls for the index are not too outlandish, as the two crucial E’s – earnings and economics – are both playing to the advantage of market-believers, like yours truly.

Underpinning the pretty good results from the likes of Treasury Wines, CSL and others is the growing belief that the 2016 comeback of mining is not a flash in the pan. All this gives solidity to the overall market index. And what I especially liked was the recovery of interest in mining services companies such as Mondelphous, which Bell Direct’s Julia Lee backed strongly on Tuesday night on my TV show. The company put on 7.5%, which gives me a better feeling about the mining sector. When mining services and real mining companies start to kick goals, it’s a solid sign.

Of course, there were disappointments and Telstra took the cake. However, as its share price falls, its yield goes up and CMC’s Michael McCarthy thinks it’s a buy at $4.60. I think some care might be required with the telco and I’ll be having a long hard look at what its CEO, Andy Penn, is up to with the company.

I’m not sure about the likes of Domino’s but I suspect when it sorts out its payments problems and we see another six months of earnings, the company’s share price will be considerably higher and the analysts agree, including Macquarie’s number crunchers.

What I liked

- Trump tax talk with the belief this week that President Trump will announce tax cuts in the next 2-3 weeks! And allegedly they will be “phenomenal” and it’s no wonder a pullback can’t get a start.

- Earnings season so far.

- I liked AMP’s Shane Oliver’s take on earnings: “We are now a bit over 40% through the Australian December half profit reporting season. As is often the case, after an initial flurry of good results, we’ve seen a few more misses over the last week. But so far the overall results remain good. 53% of companies to report so far have exceeded earnings expectations, compared to a norm of 44%. 70% of companies have seen profits up from a year ago and 69% have increased their dividends from a year ago. But reflecting the strong rally in the market in anticipation of the results, only 44% have seen their share price outperform the market on the day they reported, as a lot of good news was already priced in. Resource profits are on track to more than double this financial year and this is driving a return to overall profit growth for the market.”

- These charts look good:

- And I love this dividend chart:

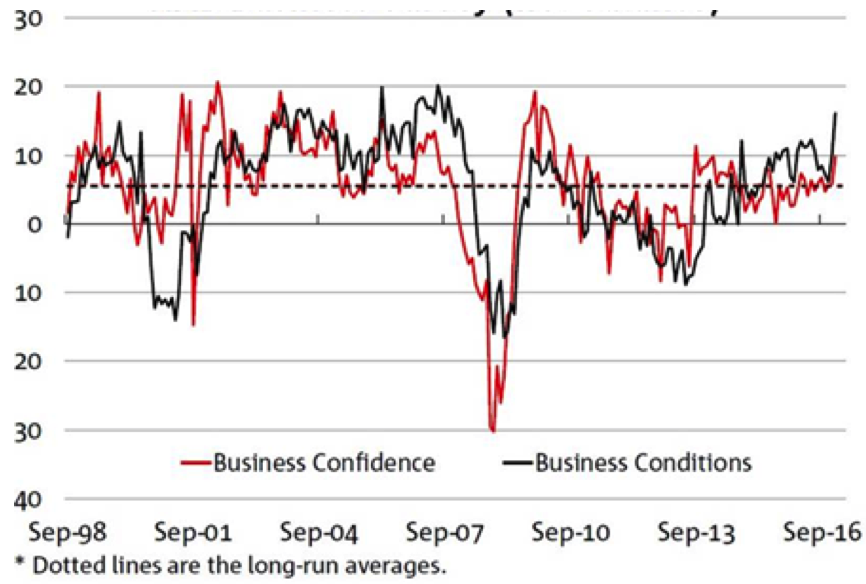

- The NAB business survey: “The latest business survey from NAB showed business conditions went from 9.9 to 16.2″ – a nine year high, which says doing business right now is a ripper! The long-term average is only 4.9!

- NAB’s business confidence reading went from 5.7 to 9.8, which is a three-year high. The long-term average is 5.8.

- The number of passengers on the Sydney-Melbourne route eased from record highs in December, down 0.2% on a year ago. The Sydney-Melbourne route is a key measure of business activity.

- US consumer prices rose by a larger-than-expected 0.6% in January to be up 2.5% on a year ago. Core consumer prices rose by 0.3% (forecast +0.2%) and higher inflation is a good thing nowadays!

- Retail sales rose by 0.4% in January (forecast +0.1%).

- The Westpac/Melbourne Institute survey of consumer sentiment rose by 2.3% in February to 99.6. The confidence index is down 1.5% on a year ago.

- Fed boss Janet Yellen implied a March rate rise and the market seems to like actions that say the US economy is looking good.

- Consumer prices in China rose 2.5% in the year to January (forecast +2.4%). Annual growth of producer prices rose to a 5½-year high of 6.9% (forecast 6.3%). Remember, inflation is good nowadays!

- The Euro STOXX 600 index rose to 13-month highs, up by 0.8%, which is a good omen considering I’ve been pointing out that Eurozone GDP numbers have been surprising on the high side.

What I didn’t like

- Total new lending commitments (housing, personal, commercial and lease finance) fell by 5.8% in December, after rising by 9% in November. Lending totalled $71.4 billion in December, down from the nine year high in November but up 1.8% over the year.

- The Oz dollar breaching 77 US cents three times this week – we grow faster on a lower dollar.

Top stocks – how they fared

The week in review

- I outlined the tests that lie ahead for the market, both here and abroad.

- Paul Rickard said Rio Tinto should be a core stock in your portfolio and revealed three ways to play resource stocks.

- The brokers placed Sims Metal Management in the good books, but AMP was out of favour.

- Charlie Aitken said Treasury Wine Estates’ strong results announcement makes it a stock to watch.

- Tony Featherstone said that despite headwinds, Genworth looks undervalued. Find out why.

- In our second broker report, Ainsworth Game Technology received an upgrade while JB Hi-Fi copped downgrades.

- In this week’s Professional’s Pick, Simon Brown said Nufarm has room to grow and could be seen as a target for acquisition.

- And in light of the changes to super rules later this year, Graeme Colley pondered the question: are transition to retirement income streams still worthwhile?

What moved the market?

- US Fed Chair Janet Yellen said delaying rate hikes would be “unwise” and hinted at the prospect of a rate rise in March.

- Encouraging signs out of reporting season (CBA was a highlight) minus a disappointing result from Telstra.

- All-time highs on Wall Street, with investors aboard the Trump tax train!

Calls of the week

- Wesfarmers boss Richard Goyder announced that he would be stepping down as CEO after more than twelve years in the top job. Watch his interview here.

- Charlie Aitken said he had ‘grape expectations’ for Treasury Wine Estates. In his view, it’s the number one alcoholic beverage exposure in the world! Find out why.

- And CBA increased its interim dividend by 1 cent to $1.99! Stay tuned for Paul Rickard’s commentary on the company’s report in Monday’s Switzer Super Report.

The week ahead

Australia

- Monday February 20 – CommBank Business Sales Index (January)

- Tuesday February 21 – Reserve Bank Board minutes

- Tuesday February 21 – Weekly consumer confidence

- Wednesday February 22 – Wage price index (December quarter)

- Wednesday February 22 – Construction work done (December quarter)

- Wednesday February 22 – Reserve Bank speech

- Thursday February 23 – Business investment (December quarter)

- Thursday February 23 – Detailed employment data (January)

- Thursday February 23 – Average weekly earnings (November)

- Friday February 24 – Testimony by Reserve Bank Governor

Overseas

- Tuesday February 21 – Markit “flash” Manufacturing (February)

- Wednesday February 22 – Existing home sales (January)

- Wednesday February 22 – US Federal Reserve meeting minutes

- Thursday February 23 – Chicago Fed National index (January)

- Thursday February 23 – FHFA Home price index (December)

- Friday February 24 – US New home sales (January)

- Friday February 24 – US Consumer confidence (February)

Food for thought

“In the business world, the rear-view mirror is always clearer than the windshield” – Warren Buffett.

Last week’s TV roundup

- Domino’s CEO Don Meij joins the show to discuss the company’s latest report, the growth of the business globally, as well as controversies the company has faced recently.

- CBA reported a profit of $4.89 billion and lifted its dividend, so to discuss the results, interest rates and more, CFO David Craig joins Super TV.

- Wesfarmers reported a 13.2% rise in half-year profit. To discuss the result, CEO Richard Goyder, who will retire this year and take on the role of AFL chairman, joins the show.

- Has reporting season given the stock market enough power to crack 6000? To discuss, Michael McCarthy of CMC Markets joins Super TV.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week the biggest mover was OFX Group with a 1.02 percentage point increase in the amount of its shares sold short to 8.38%.

Source: ASIC

Chart of the week

Business good vibes at 9-year highs

The NAB business conditions index rose from 9.9 points to 16.2 points – the highest level since October 2007! Let the good business times roll.

Top five most clicked stories

- Paul Rickard: RIO should be a core stock in your portfolio

- Rudi Filapek-Vandyck: Buy, Sell, Hold – what the brokers say

- Peter Switzer: Could this week make or break the Trump rally?

- Charlie Aitken: Treasury Wine Estates: Grape Expectations

- Staff Reporter: Buy, Sell, Hold – what the brokers say

Recent Switzer Super Reports

- Thursday 16 February 2017: Reporting season underway

- Monday 13 February 2017: Make or break

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.