There is little doubt that Ramsay Health Care (RHC) is one of Australia’s best companies. By share price performance, probably in the top 3, along with CSL and perhaps Commonwealth Bank or Macquarie. Have a look at this share price graph that covers the last decade.

Ramsay Health Care – Jan 07 to Feb 2017

So, when the stock suddenly falls 8.3% in price, after the company delivers on forecast with core profit up 12.8% for the first half, upgrades guidance for the rest of the year, and announces that its CEO intends to retire later in the year, this is what we call in the trade as a “buying opportunity”. And that is what happened on Thursday.

The retirement of Chris Rex, who has been CEO since 2008 and prior to that, Chief Operating Officer for 13 years, took the analysts by surprise and perhaps the Company could have done better in briefing the market. But as soon as the CEO tells you that he intends to go, this becomes a disclosable item and the Board had no choice but to advise the market.

What the market seems to have forgotten is that with a track record of performance going back to the nineties, however great Chris Rex was as a CEO, this is not just down to one man. A strong board and senior leadership team, and most importantly, the 60,000 employees, have produced this performance.

So, has the “buying opportunity” passed, or is there still value in Ramsay?

I am of the latter view, and here is why.

Ramsay’s Half Year

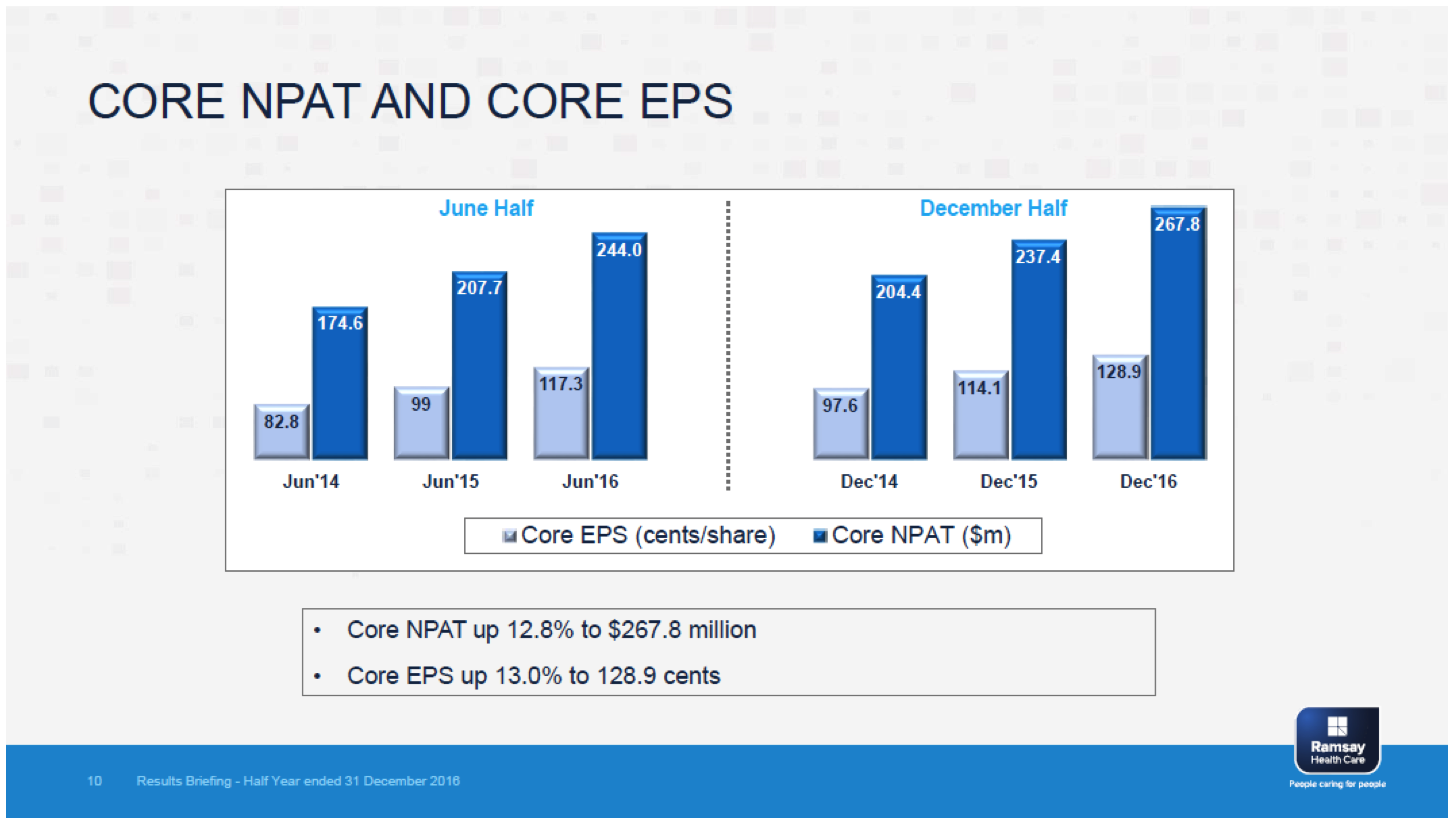

Ramsay reported core NPAT of $267.8m for the December half year, up 12.8% on the corresponding period in 2016. Core EPS (earnings per share) grew by 13% to 128.9 cents.

Reflecting weakness in the pound and euro, revenue grew by 3.5% but 7.6% on a constant currency basis. The Australian hospitals business was again the star, with strong growth in admissions despite some market volatility leading to revenue growth of 8.8%.

Segment revenue and EBITDA contributions (in local currency) are set out in the table below.

Comparing Ramsay to competitor Healthscope’s Australian hospital business, in the December half year, Ramsay achieved revenue growth of 8.8% compared to Healthscope’s 3.0% and EBITDA growth of 14% cw 2.2% for Healthscope. Ramsay improved its operating margin to 20.0% – a full 150bp higher than Healthscope.

On the negative side for Ramsay was the performance of the French and UK hospital business, where EBITDA (in local currency) rose by 2.9% and 1.9% respectively.

Importantly, Ramsay upgraded its guidance for the full year. It lifted guidance for core NPAT growth and Core EPS growth from 10% to 12% to a higher range of 12% to 14%.

Upsides

Ramsay sees growth coming from three drivers. Firstly, organic growth from the demographic and technological changes that make this sector so attractive:

- Population growth and ageing;

- Increase in chronic and lifestyle diseases; and

- Advancements in medical technology and treatments.

Secondly, a public hospital system that is under pressure in all three markets (Australia, France and the UK). This provides an opportunity for brownfield capacity expansion, and public private collaborations.

In the last half, Ramsay completed $142m of developments which increased capacity by 166 beds and led to the opening of six operating theatres and two private emergency centres. Its pipeline of developments includes a new mental health facility on the Gold Coast, St Andrews Private Hospital in Ipswich, a new Northside Clinic in Sydney, Albert Road Clinic in Melbourne, three new theatres and day surgery expansion at The Avenue, Melbourne and a new three-theatre day surgery in Croydon, UK.

The third plank of the growth strategy is strategic developments and acquisitions. In this category is Ramsay’s pharmacy strategy, where it plans to establish an extensive network of franchised retail pharmacies throughout Australia for the provision of pharmacy and associated services. It currently has 22 pharmacies and expects to rapidly expand the network in 2017 and beyond.

On the cost side, Ramsay sees an opportunity to deliver substantial savings in supply costs through the implementation of a global procurement strategy.

Risks

Leaving aside the price risk (ie. is Ramsay too expensive?), there are two major short term categories of risk. Firstly, in Australia, with regard to private health insurance and the relationship between the hospitals and the insurers. Rising premiums impacts the affordability of private health insurance and participation rates, while the insurers are getting increasingly more active in contractual negotiations with the hospitals and demanding “service quality” guarantees. In relation to the latter, Ramsay says that it has been able to negotiate satisfactory outcomes with the major insurers.

The other major risk relates to Ramsay’s offshore assets, in particular, its portfolio of hospitals in France. Already under pressure from two years of mandated tariff reductions by the French Government, the French Presidential election will be held in April/May. Although unlikely, a win by National Front leader Marine Le Pen would be seen as a negative for the private hospital industry in France.

There is also a foreign exchange risk. With France and the UK now accounting for one third of Ramsay’s earnings, further weakness in the Euro/Pound will impact Ramsay’s bottom line.

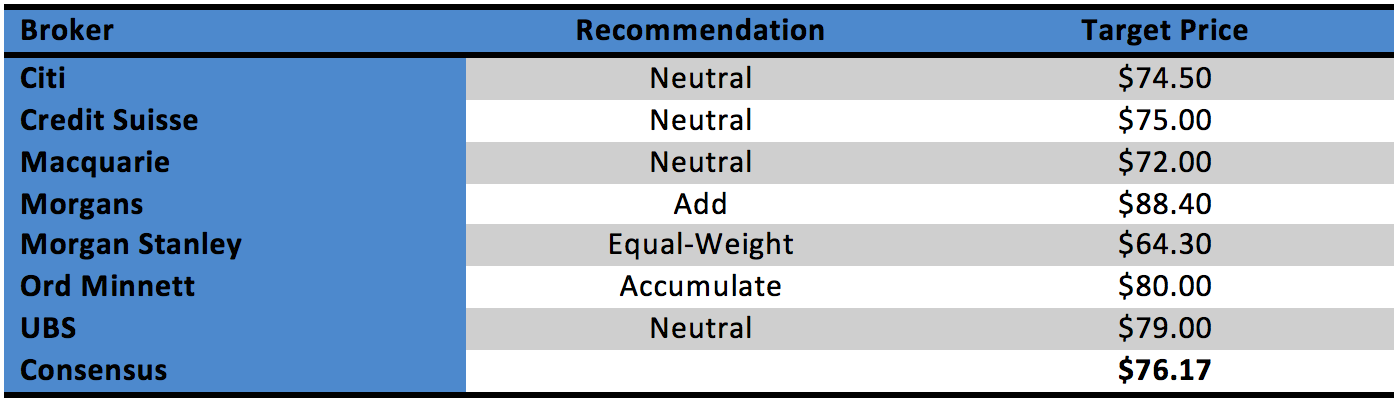

The Brokers

The Brokers are largely neutral on Ramsay. With Ramsay currently trading about 8.6% below the consensus valuation, they see some value and understand the growth agenda, but note potential headwinds with the UK and French businesses. Individual ratings and target prices (source FN Arena) are as follows:

On a multiple basis, Ramsay attracts a premium price. The Brokers have Ramsay trading on a multiple of 26.7 times forecast 2017 earnings, and 23.9 times forecast 2018 earnings.

My view

Yes, Ramsay is expensive, but there are very few companies that have been able to deliver year after year EPS growth of circa 14% per annum. And the CEO going is a negative, but the company’s record suggests that it will be able to navigate this hick-up. Further, the tailwinds of an ageing population and increased demand for health services remain firmly in place.

On track record, Ramsay deserves to be core holding in SMSF and other portfolios oriented to long-term growth, or for those who want exposure to the healthcare sector. At around $70, Ramsay is in buy territory.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.