In a week when stocks should have gone up, with positive Trump trade talk with China, the pesky political Peter Dutton play for the Prime Ministership also took our eye off how reporting season has progressed, in what has been the biggest week for the corporate show-and-tell we all look forward to. And it looks like the results will come in better than expected, which mirrors our economy that continues to just come in better than the consensus views, which have tended to be a little too negative.

This is AMP Capital’s Shane Oliver’s summary of what has shown up so far, with 85% of companies reporting: “47% of results have surprised on the upside, compared to a norm of 44%, the breadth of profit increases is high, with 79% reporting higher profits than a year ago compared to a norm of 66, 86% have increased their dividends or held them constant and 65% of companies have seen their share price outperform the market on the day results were released. 2017-18 earnings growth are on track to come in around 9%, with resources earnings up 25%, thanks to solid commodity prices and rising volumes and the rest of the market seeing profit growth of around 5%.”

Here’s a chart that shows the above story:

For dividend lovers, like yours truly, here’s a nice picture of improving dividends. Just follow the blue line.

Overall, the Dutton drama and what it means for the credibility of the Coalition Government and its potential to beat Bill Shorten’s Labor, in large part explains why our S&P/ASX 200 index ended down 91.9 points, 1.45% (for the week) to finish at 6247.3 .

You don’t have to be David Speers or Laurie Oakes to work out that a Labor Government will play a lot harder ball with banks and future regulation, so it was the banks that made heavy weather of it all last week. Westpac actually was off 8.5% to $27.75 over the week, after it reported on Friday, not helped by an 11 basis point fall in its net interest margin.

And after reporting a 14.5% rise in net profit, Flight Centre was fried by the ABC, with allegations of bad behaviour towards its customers. The share price copped a 15.3% slugging by the stock market, down to $57.90!

The huge story that really was swamped and trumped by the Dutton drama was TPG’s talks with Vodafone that gave the telco sector a huge shot in the arm. Over the week, TPG shares rose 29.4% to $7.74, Telstra shares rose 4.2% for the week to $3.21, while Vocus put on a huge 18.7% to close the week at $2.82. The prospect of less players and potentially less crazy competition in the mobile business has got the market, probably, excessively excited. But that’s what markets do in both directions!

Another important story for the week was the good reporting by what many thought is the over-hyped tech-sector. This is how the AFR’s William McInness summed it up neatly: “The information technology sector had a week to remember, with prices rising and falling wildly this week, after Wisetech Global, Altium, Afterpay, Iress and Carsales.com all reported. Despite some lofty guidance, most of the tech stocks were able to hit expectations, causing a short squeeze on some of the most shorted stocks. Wisetech Global closed the week up 26 per cent at $20.00, Altium closed the week 27.5 per cent higher at $27.47, while Appen that’s yet to report, rose 22.9 per cent to $13.73.”

Don’t you love it when the ‘shorts’ cop it?

And I have to point out the performance of Afterpay, with its shares up 17.5% for the week to $19.64, after revenue growth of 390%! It also raised $108 million this week to buy the UK business, ClearPay, which will give it a significant footprint in the Old Dart.

To US markets overnight and, unlike our leaders, the US leader wasn’t upsetting stock markets, with the S&P 500 and the Nasdaq hitting all-time highs! And helping the story was an upgrade for Netflix, after SunTrust noted that the pay-TV business is growing like topsy overseas. And if my viewing habits can be useful, I think these analysts are on the money.

Its share price was up over 5% overnight.

Helping positivity was the Fed boss, Jerome Powell, who addressed the fun group of economic types at the famous conference in Jackson Hole, Wyoming, telling them that the US economy was “strong” and that there’d be “further, gradual” rises in interest rates.

The market wasn’t spooked by his observations and liked his take on inflation ahead, which looks like it won’t force the Fed’s hand to hike rates too quickly, which could kill off this remarkable bull market in the States. The US dollar fell after his speech and that’s good for the US economy as well.

And the boss of Target, Brian Cornell, gave Donald Trump’s economy a big pat on the back, saying this after reporting pretty well: “There’s no doubt that, like others, we’re currently benefiting from a very strong consumer environment – perhaps the strongest I’ve seen in my career.”

Interestingly, China and the US concluded trade talks with no big achievements but at least this ongoing battle didn’t rattle the stock market for a change!

What I liked

- The decision to make the new PM Scott Morrison. The whole Dutton drama hasn’t been good for stocks this week but if Malcolm had to go, I think ScoMo is the right man to give Bill Shorten a run for his money.

- The “flash” purchasing managers index in the USA eased from 55.7 to 55 in August (forecast 56.3) but any number over 50 means expansion.

- Some experts reckon the S&P500 index marked its longest ever bull market run of 3,453 days but this defies other assessments that say the US stock market has gone for 15 years plus over the 1950s and beyond!

- Early in the week, US-China trade talk optimism, linked to a meeting later this month, helped US stocks for most of the week.

- Concerns about Turkey eased over the week.

- Eurozone business conditions PMIs were basically stable in August.

What I didn’t like

- The US slammed tariffs on $US16 billion worth of Chinese goods and the Chinese returned fire.

- There wasn’t much data out this week.

- The political battle for the Lodge that hasn’t helped stocks!

On our new PM Scott Morrison

I promise this is the last time I’ll point out that I taught Scott Morrison Economics but it’s a big milestone when someone you saw as a kid, just out of school and at the UNSW, goes on to become the Prime Minister. And while he has his dissenters, the economy and the country’s finances have headed in the right direction on his watch.

None of us like his $1.6 million cap but all Treasurers ultimately make decisions that even hurt their constituents.

This is what the AFR said about ScoMo on Friday before the vote: “His May budget offered a path to returning insidious bracket creep tax increases, boosted incentive in the personal tax system, and put the budget on a course back to balance. Angering many in the Liberals’ base, he rightly capped unsustainable superannuation tax breaks for the better off.

Yet Mr Morrison’s conservative credentials leave him better placed to clean up the party’s bad blood. As immigration minister, it was he, not Mr Dutton, who stopped the boats. He is rooted in Sydney’s deeply suburban Sutherland Shire, is an unshowy evangelical Christian, and at home with small business aspiration. But he is worldly enough not to alienate moderates and centrists. He has openly displayed loyalty to Mr Turnbull.”

I wish him luck for his sake and for our aspirations as loyal Australians and as people committed to building our own wealth.

Go ScoMo.

The Week in Review:

- I shared a quick look at how last week’s reporters are faring against their target prices with ‘Stocks in and out of the buy zone!’

- It looks like Link Market Services has got over the hiccup of the Government’s budget announcement and, according to Paul Rickard, it may be well positioned for long-term growth.

- With another big reporting week for blue chips and market darlings done and dusted, James Dunn offered 10 company earning reports you should have been watching.

- The S&P/ASX 200 is the US dollar’s slave, which means you have to hunt for the right kind of growth in an overbought market. According to Charlie Aitken, Aristocrat Leisure could be just what you’re after.

- Tony Featherstone served up 3 small-cap company stars that delivered solid results this earning season.

- Our Stock of the Week was ResMed by Philippe Bui of Medallion Financial Group.

- In our first Buy, Hold, Sell – what the brokers say we saw what looked like a record number of movements by brokers! And in our second edition, CSR was one of the lucky few to get an upgrade.

- In Questions of the Week, we answered a reader’s query about a precious metal and funds management company.

- Among our Hot Stocks this week were Rio, QBE Insurance and Kogan. Find out why!

What moved the market?

- TPG Telecom and Vodafone Hutchison Australia confirmed Wednesday that they were in merger talks with a statement by TPG saying discussions were about a “merger of equals.”

- Australia was served yet another leadership crisis, with PM Malcolm Turnbull facing down calls by senior party members for his resignation. The government suspended parliament on Thursday to try to come to a resolution on the issue.

- Trade talks between the US and China kicked off in Washington this week, in an effort settle the escalating trade war.

Calls of the week:

- Paul Rickard named Link Market Services as a stock positioned for long-term growth.

- The Liberal Party picked Scott Morrison as its next leader in a close 45-40 spill vote against Peter Dutton, making ScoMo the country’s 30th Prime Minister.

- Charlie Aitken said it’s time to be cautious around the S&P/ASX200 – which he said has risen to 11-year highs for unjustified reasons.

The Week Ahead:

Australia

Wednesday August 29 — New Home Sales (July)

Thursday August 30 — Business investment (June quarter)

Thursday August 30 – Building approvals (July)

Friday August 31 — Private sector credit (July)

Overseas

Monday August 27 — China Industrial profits (July, year)

Monday August 27 — US Chicago Fed National Activity Index (July)

Monday August 27 — US Dallas Fed Manufacturing Index (August)

Tuesday August 28 — US Trade in goods (July)

Tuesday August 28 — US Home prices (June)

Tuesday August 28 — US Consumer confidence (August)

Tuesday August 28 — US Richmond Fed Manufacturing Index (August)

Wednesday August 29 — US Economic growth (prelim, June quarter)

Wednesday August 29 — US Pending home sales (July)

Thursday August 30 — US Personal spending/income (July)

Friday August 31 — US Chicago Purchasing Managers Index (August)

Friday August 31 — US Consumer confidence (August, final)

Food for thought:

“In war, you can only be killed once, but in politics, many times”

Winston Churchill

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

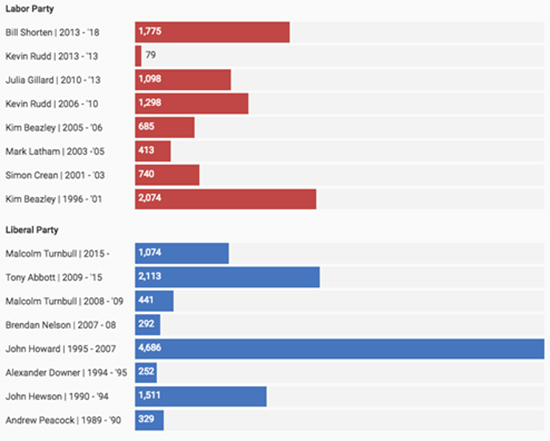

Chart of the week:

The number of days in power for recent Labor and Liberal party members published by the ABC:

Source: ABC

Source: ABC

Top 5 most clicked:

- Stocks in and out of the buy zone! – Peter Switzer

- Buy, Hold, Sell – what the brokers say – Rudi Filapek-Vandyck

- 10 company earning reports to watch – James Dunn

- Aristocrat Leisure – a $40 plus stock – Charlie Aitken

- Hot stocks – Rio, QBE Insurance and Kogan – Penny Pryor

Recent Switzer Reports:

- Monday 20 August: Hit or miss

- Thursday 23 August: Pockets of growth

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.