Link Administration Holdings (LNK) is a stock I’ve supported since its IPO and after reviewing the 1st half FY17 result, I am of the view LNK is undervalued by around 10% on what we know today.

My view remains LNK is a very high quality larger mid-cap business ($2.7b market cap) that operates in a structurally growing sector with high barriers to entry.

The stock has been somewhat in the doldrums for six months but my fund has used that as an opportunity to increase our investment in LNK, feeling the structural earnings and dividend growth the company offers is now under-priced by the market.

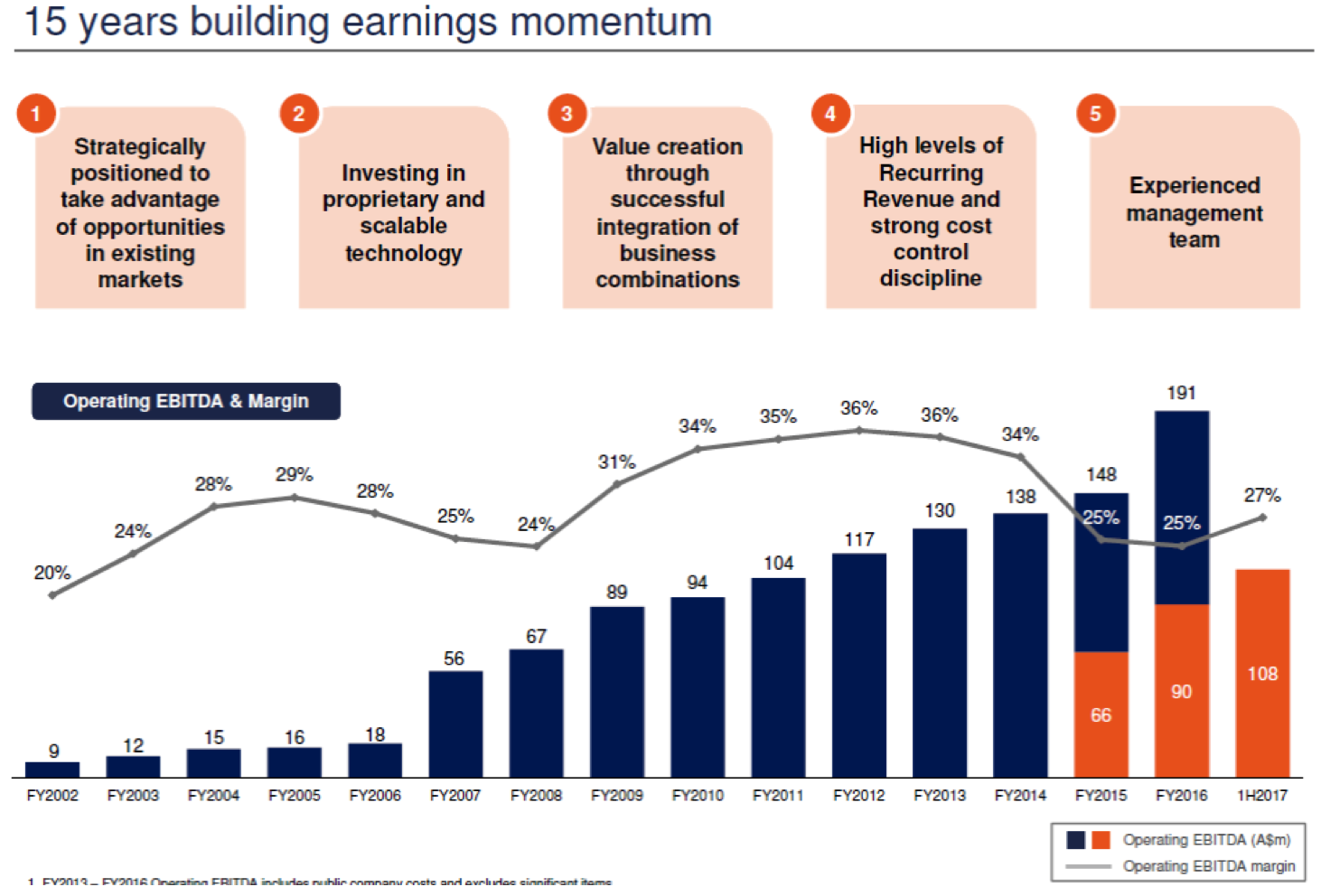

Just to remind you Link Administration Holdings Limited operates as a holding company. The company, through its subsidiaries provides fund administration, corporate markets, information and digital and data services. LNK serves customers worldwide and has spent “15 years building earnings momentum”.

There’s always a degree of scepticism towards stocks that were once owned by private equity, and rightly so in many Australian examples, but in LNK’s case my view is that private equity made this a better business and this isn’t a company that is suddenly going to experience deterioration two years after the private equity exit. My view is this company is going to continue to structurally grow and the indigestion caused by the final private equity sell down earlier this year has provided investors with an opportunity. The other point worth noting is private equity left LNK with a strong balance sheet ($282m net debt) which is a clear positive and differentiates it from many other private equity exits.

LNK is also a diverse and enduring company by customer base and geography.

The 1H result was clean and good. There was clear evidence of structural growth and strong management value add.

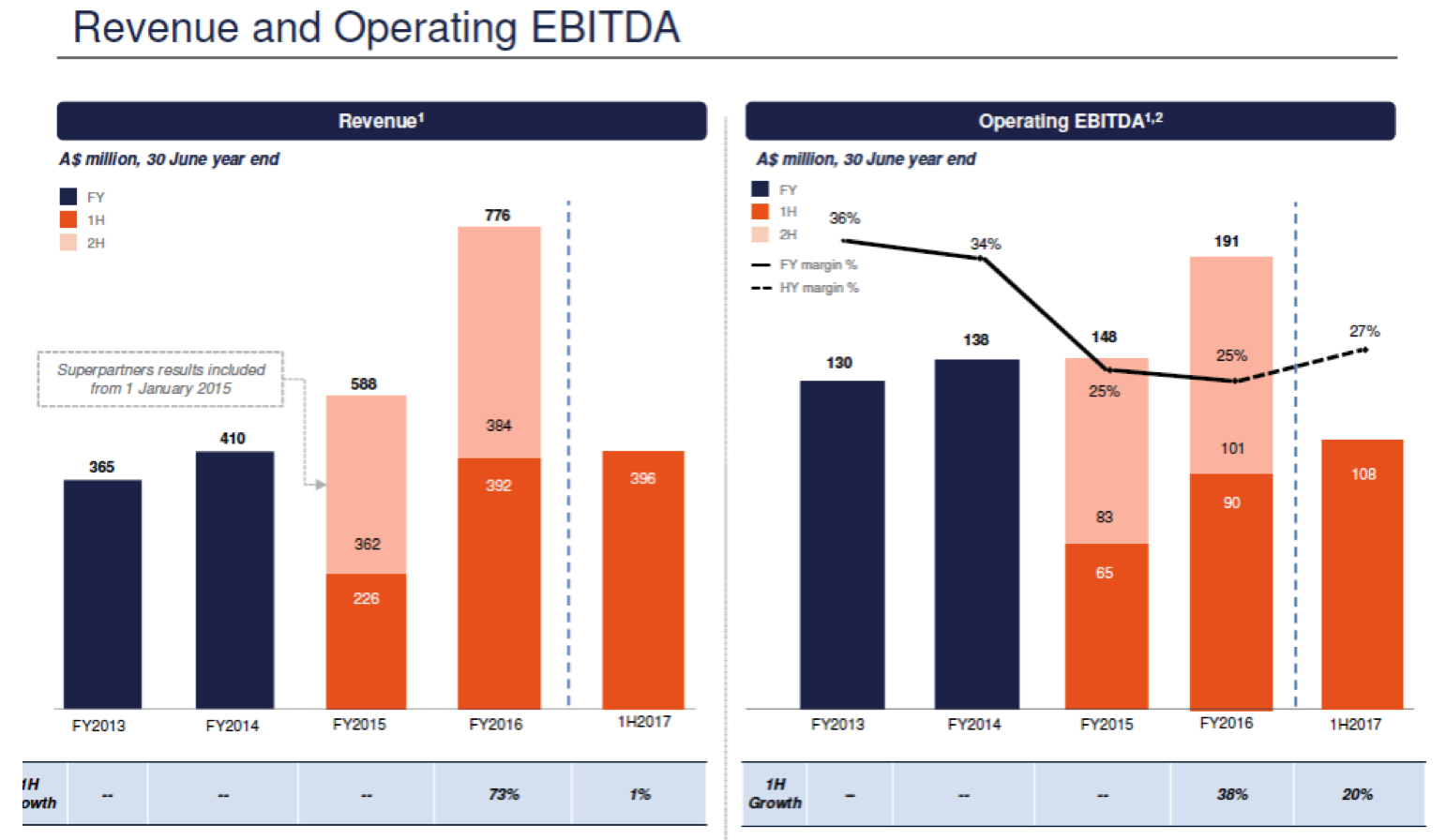

The result was better than analyst expectations and will lead to +2% to 3% upgrades to FY17 consensus EPS estimates and beyond. That is an important point and I feel investors will come back to LNK in the next few weeks and realise it’s one of a small number of mid-cap stocks that beat consensus estimates and experienced consensus earnings upgrades.

I said on Peter Switzer’s TV show the other night that once the dust settles on the reporting season genuine institutional investors meet with companies and analysts and then think about where they want to be invested for the next six to 12 months. Sometimes a good result goes under the radar because of the very compressed reporting season, only to be rediscovered a few weeks later. I think LNK is a real candidate for re-rating in the next few weeks as investors do more work on what was an excellent set of interim numbers.

One of the reasons I think LNK has been somewhat overlooked this reporting season is only four analysts cover the stock with research. That’s unusually low for a $2.7b market cap stock and my suggestion to the LNK board and management would be that they should be actively encouraging more broking houses to write research on their stock because it’s a really good, undervalued story!

Interestingly though, of the four analysts who bother covering LNK, the median 12 month forward price target is $8.29, +11% above the current share price and in line with the undervaluation I see in LNK shares.

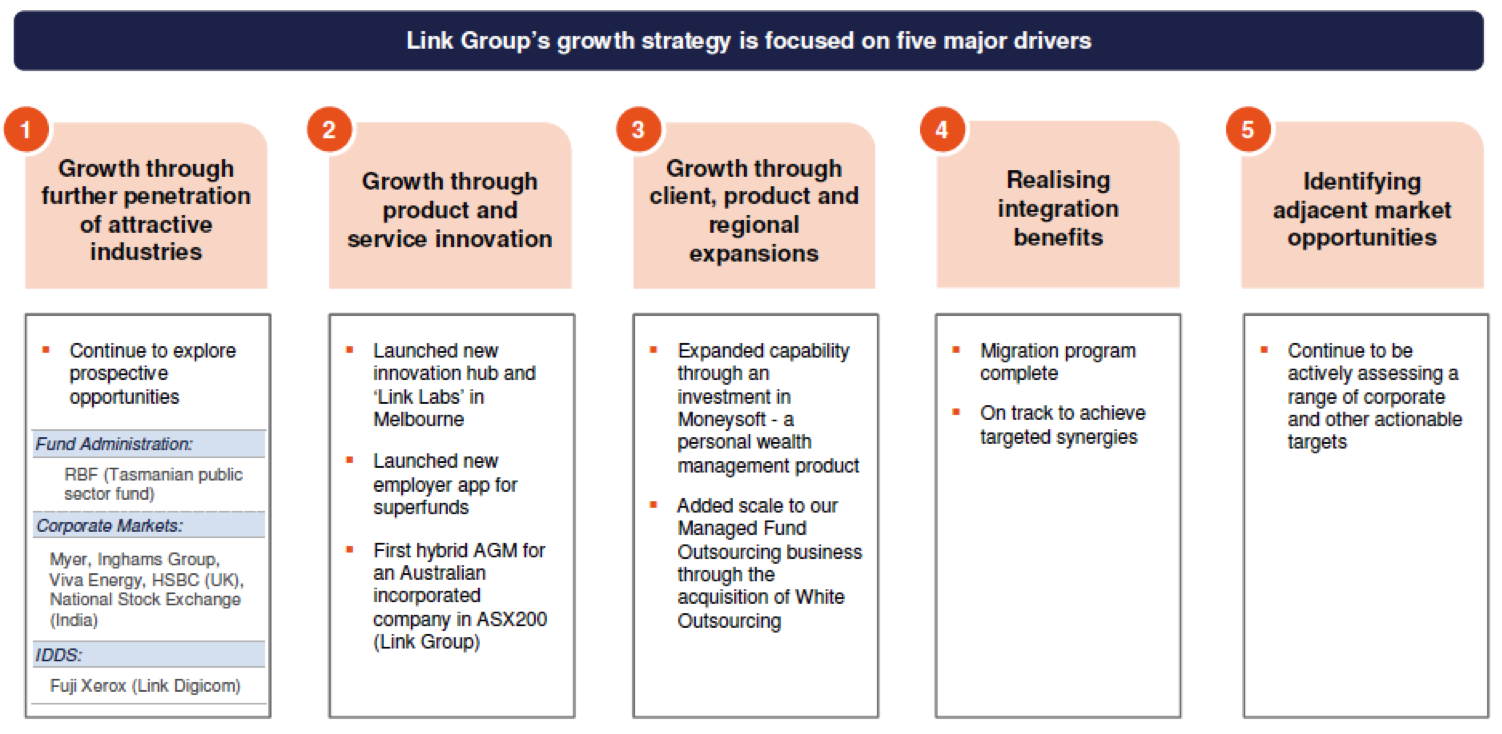

I tend to believe there’s more GROWTH to be had from this company in the next few years than is currently forecast. The company itself is trying to guide you with the table below of its “five major drivers of GROWTH”.

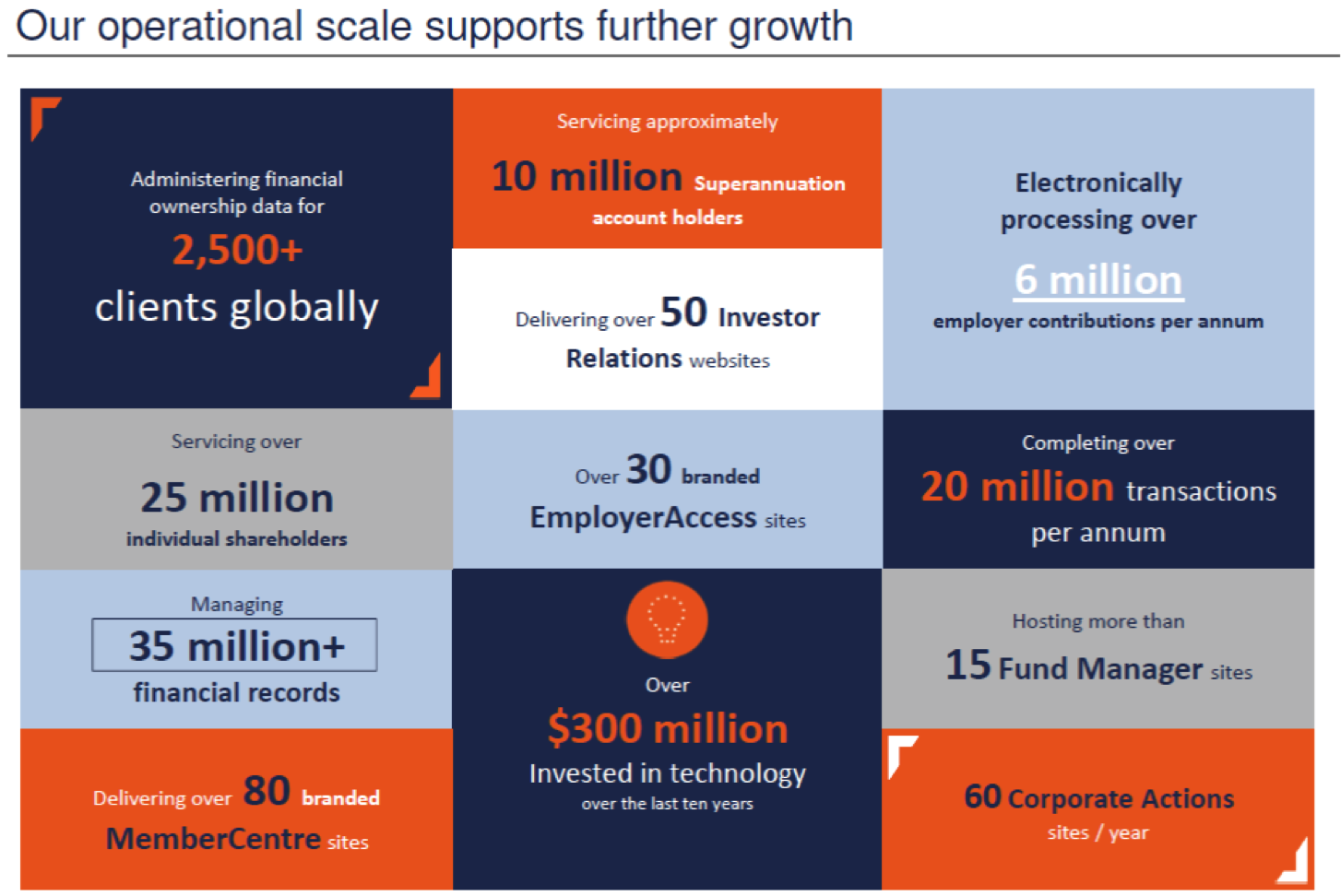

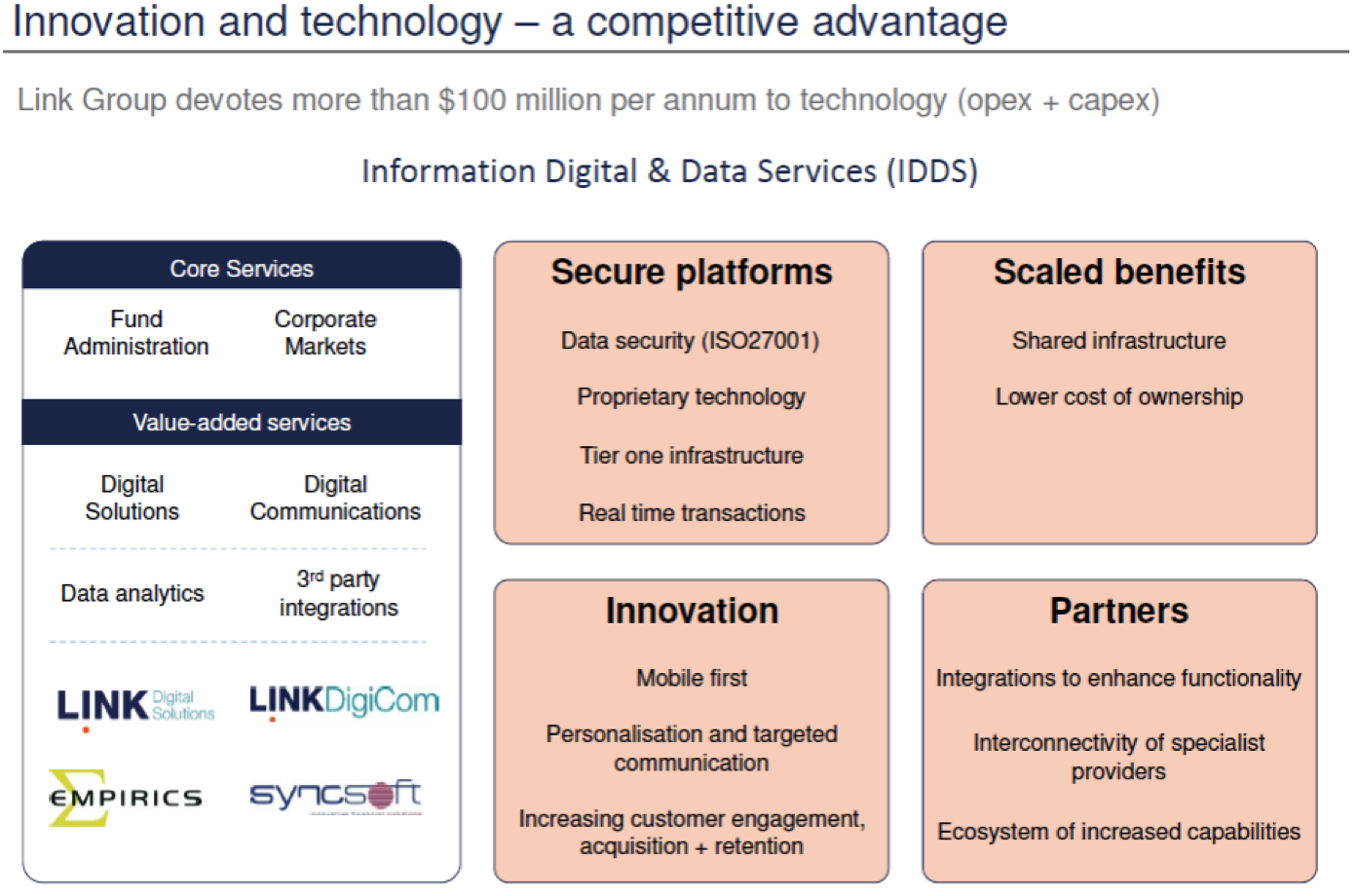

I also like the fact LNK is investing heavily in technology. In my opinion, this is a perquisite of any growth business.

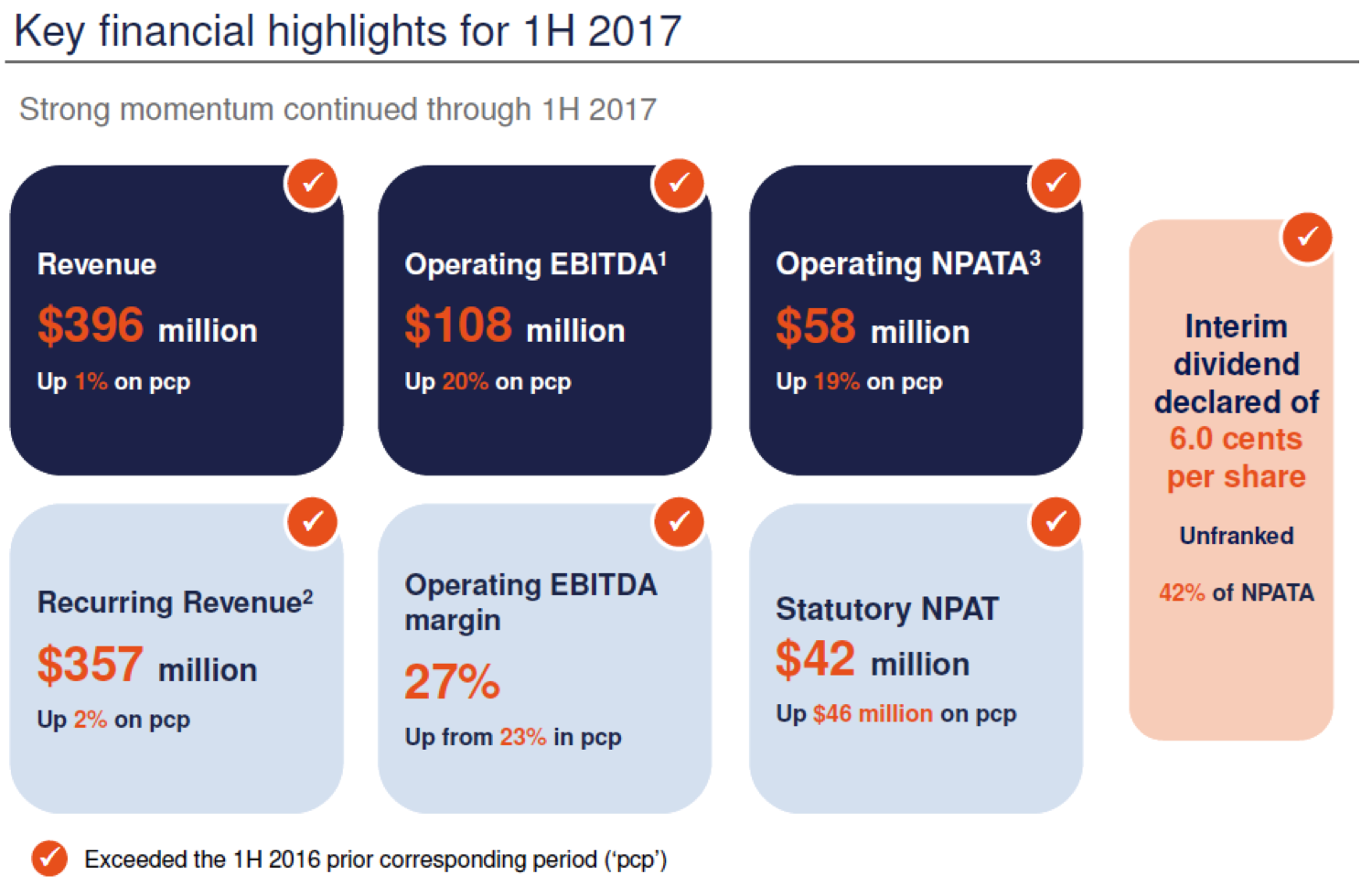

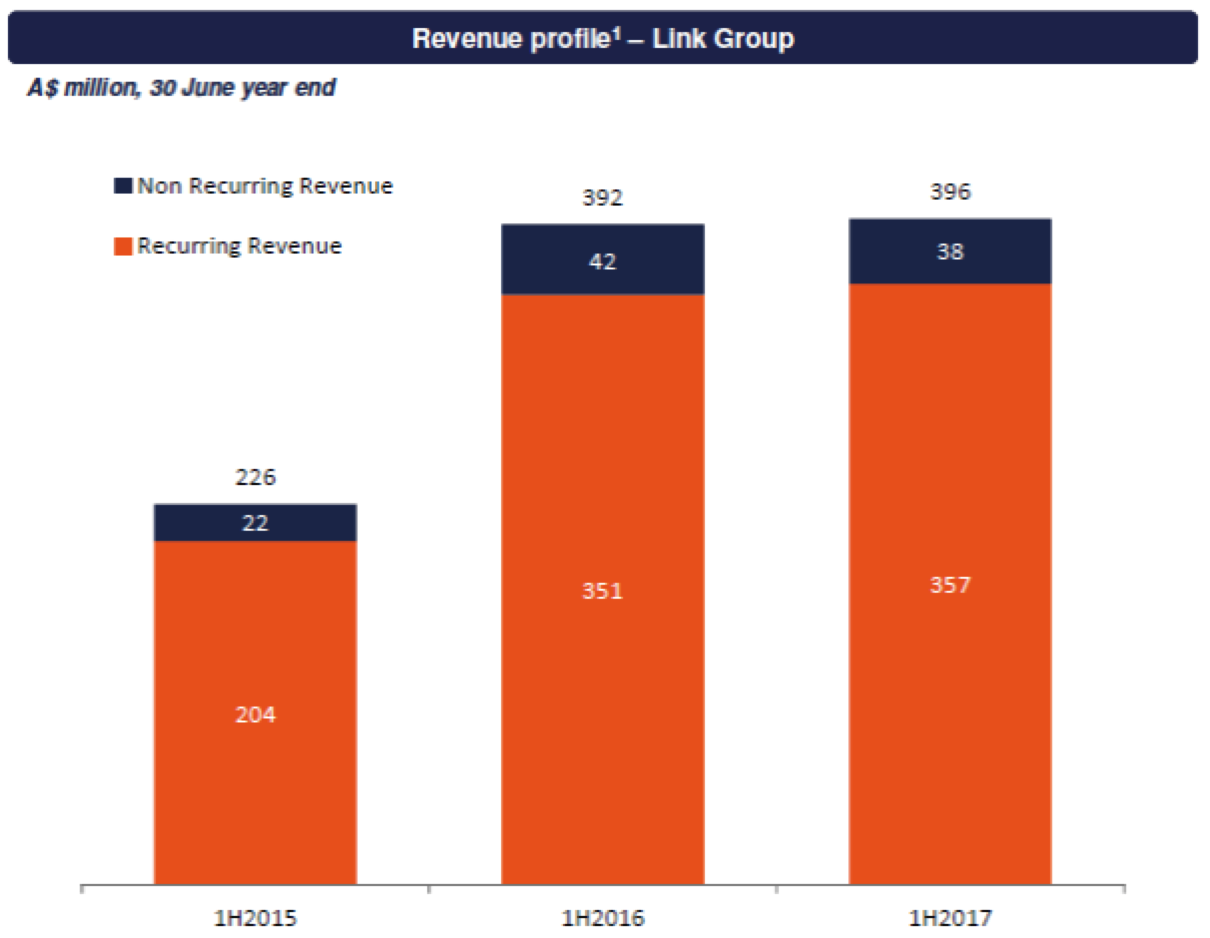

Arguably, the greatest attraction on LNK is its recurring revenue streams. 90% of group revenues are “recurring”. This is NOT a cyclical business as such and why in my opinion it should command a P/E premium to the ASX200 and its peers. The percentage of recurring revenue rose 2% in the half.

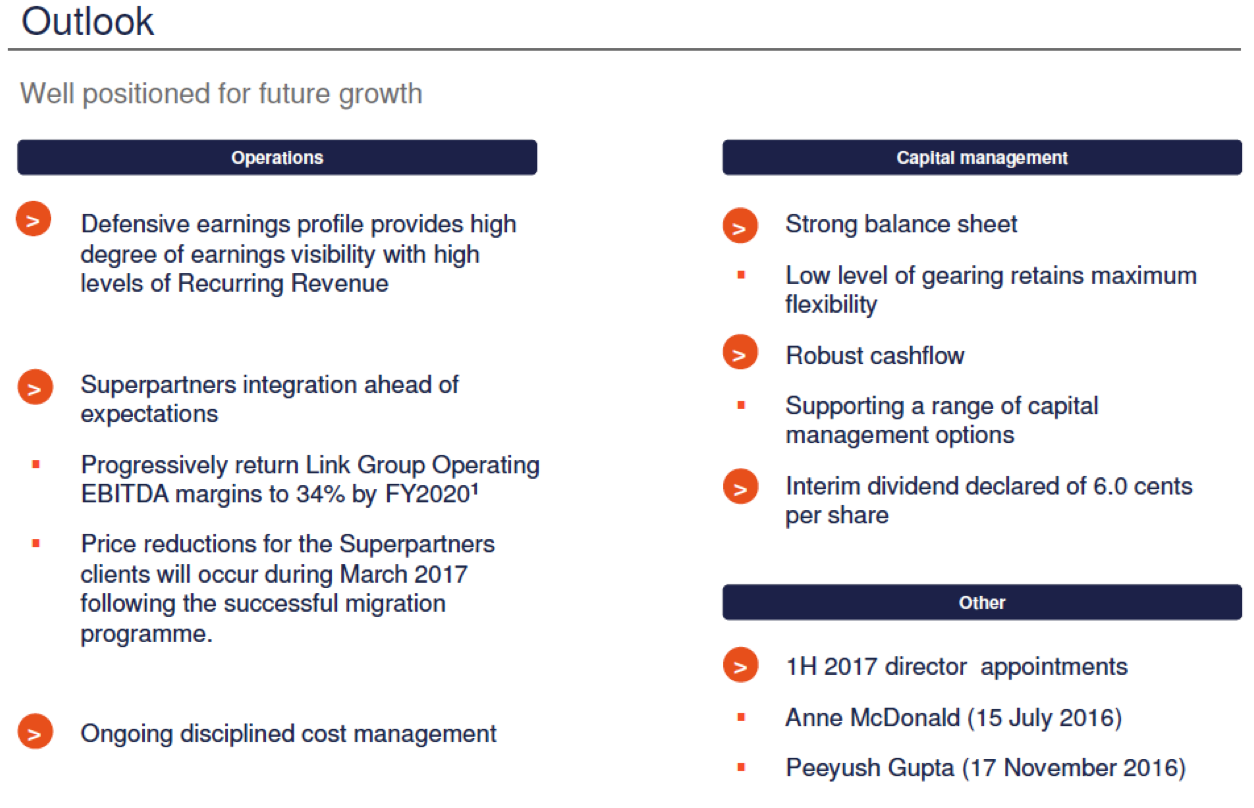

The outlook side was positive and I agree the company is “well positioned for future growth”.

On all the information above I am of the view LNK should be trading above $8.00.

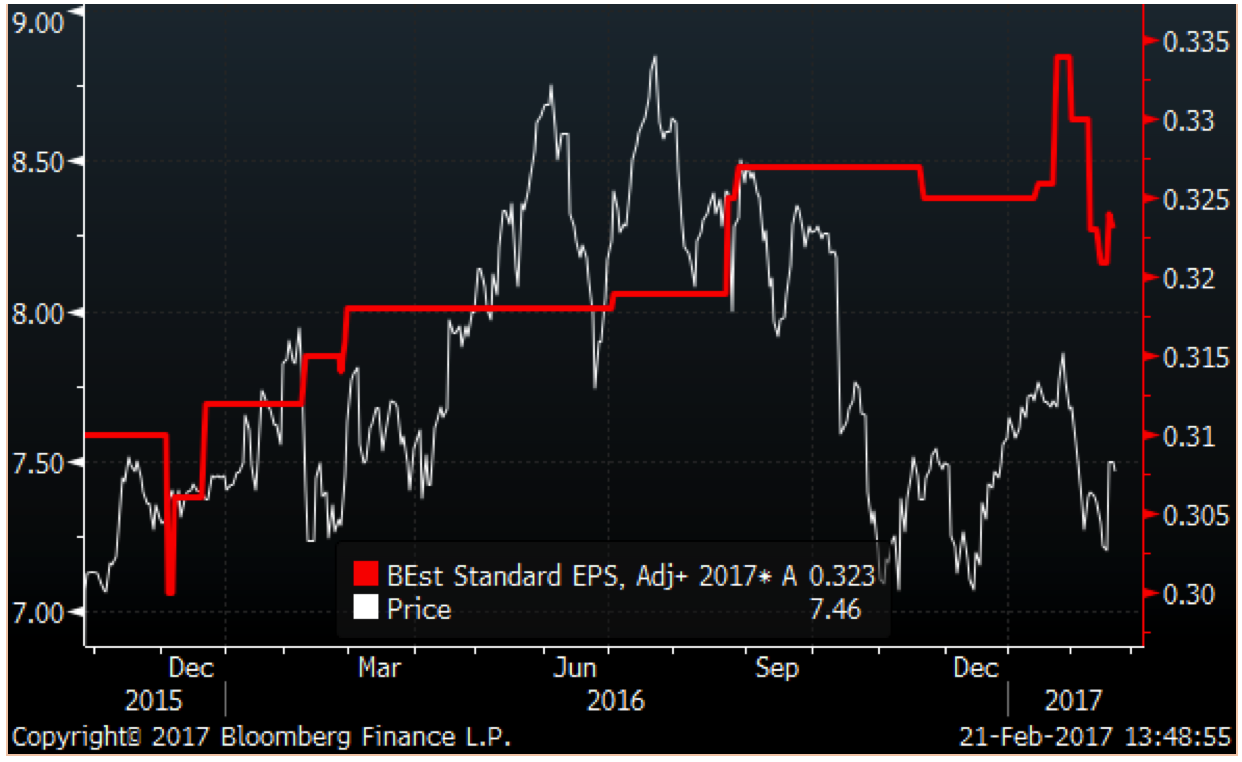

The table below charts consensus LNK FY17 EPS estimates and the LNK share price. You can see that around 32.5c of EPS LNK shares were happily trading between $8.00 and $8.50 in the middle of last year. I can see no reason why the market won’t pay $8.00 to $8.50 again for exactly the same EPS stream.

I forecast LNK to generate 33c of EPS in FY17 and 40c in FY18. Applying a P/E of 22x for the FY18 year generates 18 month price target of $8.80.

So my view is LNK should trade up to between $8.00 and $8.80 in the months and year ahead and I encourage you to consider the stock for your growth portfolio while it is undervalued vs fundamentals.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.