[table “279” not found /]

This was an odd week when I actually admitted on TV and in my Thursday Switzer Daily piece that I was a tad negative! Rudi Filapek Vandyke, the founder of FN Arena, wanted to note the day, time and place when I said this on The Final Count. I did quickly add, however, that it wouldn’t last for all that long – maybe until August earnings or until Donald Trump gets his tax plans passed.

However, ironically and you might have missed this, our market actually went up this week.

The S&P/ASX 200 gave up 0.65% on Friday but ending at 5751.7 meant we put on 0.4%, which surprised someone like me, who watches the market like my black lab used to watch a sausage on a BBQ.

Oil prices had been good for the week until OPEC’s meeting, where the commitment to production cuts was not as strong as experts were hoping.

Helping to explain my short-term and not very dramatic negativity is AMP Capital’s Shane Oliver’s explanation for his negativity.

“Poor shares reflected relatively tighter monetary policy in Australia, the commodity slump, the lagged impact of the rise in the $A above parity and a mean reversion of the 2000 to 2009 outperformance – has been reversed,” he wrote on Friday. “However, the Australian share market looks likely to continue underperforming going forward, reflecting weaker growth prospects in Australia – with the economy looking like it may have stalled again in the March quarter, the housing cycle peaking and turning down, constraints on consumer spending (high debt, higher bank lending rates, slowing wealth effects, rising energy costs, record low wages growth and high underemployment, risks around the banks and uncertainty around the outlook for bulk commodity prices.”

Now that’s pretty annoying, negative stuff but wait, it’s not all bad news. He finally concludes: “We still see the ASX 200 higher by year end, but global shares are likely to do better on both a hedged and particularly un-hedged basis.”

So the news is not great and the Amazon threat is not helping, with our retailers trashed for most of the week, with Myer and Super Retail Group down by more than 10% for the week. Last week I had the latter’s CEO, Peter Birtles, on my show and he was very happy with the way his stores were going. I really hope he sticks it to analysts in reporting season. And he might, given what happened to retail reports in the US on Thursday.

Shares in Best Buy soared 21.5%, while shares in Sears were up 13.5% on Thursday alone. How come, with Amazon out there ‘killing’ retailers?

As CNBC put it: “Best Buy showed signs in the latest quarter that it has the right formula to go up against Amazon, as more shoppers ring up their purchases online.”

Could JB Hi-Fi do the same? That’s a good question for my Monday column!

Best Buy shares ended up nearly 19% on Thursday afternoon, reaching an all-time intraday high of $60.14.

Analysts were expecting a 1.5% decline and the company was worried too but maybe Amazon was over-hyped, as I’ve been predicting.

Not surprisingly, the recent sell off madness was questioned by the market, with JB up 3.26% on Friday to $23.12, but on February 10 it was $29.38

More on this on Monday.

What I liked

- The Nasdaq and S&P 500 again closed at record highs, suggesting that belief in Donald remains.

- Morgan’s Michael Knox’s positive outlook for commodity prices for 2017.

- The news that House Speaker Paul Ryan is convinced President Trump’s tax reform measures will be passed this year.

- The ANZ/Roy Morgan consumer confidence rating rose by 1% to 110.5 in the latest week – the third rise in the past four weeks!

- The US “flash” Markit PMI eased by 0.3 to 52.5 in May but it’s still a positive number.

- The so-called “fear gauge” (the CBOE volatility index or VIX) fell by 9% to 10.96 during the week and Wall Street was up five days in a row! Donald’s foibles are quickly forgiven by the market, thankfully.

- Eurozone business conditions PMIs remained very strong in April and business confidence rose in Germany and France, which is all consistent with strengthening growth in Europe.

- Contango’s Bill Laister liking Ausdrill because of a miner’s presentation he went to, where the CEO talked about returning to exploration because the higher commodity prices encouraged it!

What I didn’t like

- The terror attack in Manchester, England.

- Local construction work done in the March quarter fell by 0.7%, to be down 7.2% on a year ago but Victorian construction rose by 3.4% to a record $11.2 billion in the March quarter.

- The Richmond Federal Reserve composite index in the US eased from +20 to +1 in May, with manufacturing shipments down from +25 to minus 2.

- OPEC’s oil cut decision sent oil prices lower and this can be negative for US stocks.

- Me not as positive as I usually am but the latest run of economic data could mean the next GDP number could be zero or even negative! (That comes out in two weeks time on Wednesday June 7.)

One more like and it’s important…

Fairfax reported on Friday that WorleyParsons soared 12.2%, “after it told investors it was seeking more than $410 billion in contracts from China’s Belt and Road spending plan.”

When someone is looking for good news going forward, the age of infrastructure abroad and here (recall the Budget’s $75 billion spending plan) could be the stimulus we have to have.

The week in review:

- I discussed how you might play this new phase of the market. Don’t forget this lesson!

- Amazon worries have contributed to the share price fall of both JB Hi-Fi and Harvey Norman, so are they a buy? Paul Rickard revealed all in this week’s article.

- In this day and age of hacking, there are potential gains for companies that exist to protect against these threats. James Dunn shared four stocks, an ETF and upcoming listings to watch.

- Rising interest rates may be among the concerns for REITs. Roger Montgomery revealed three REITs to watch out for.

- Buying LICs based on discount and premiums alone is dangerous. Tony Featherstone revealed a diversified portfolio of five unloved LICs to consider.

- Charlie Aitken said it’s tougher times ahead for Australia and that companies like Wesfarmers may be hit by a household cash flow squeeze.

- MNF is a software-based telecommunications business with clients including Skype and Aldi Mobile. Sebastian Evans explained why he likes the stock.

- The brokers placed Huon Aquaculture in the good books this week, while G.U.D. Holdings was downgraded.

- In our second broker report, Harvey Norman and Stockland were upgraded, while Suncorp and Sydney Airport were downgraded.

- Our stock selectors placed Fortescue Metals and Rio Tinto on the likes list this week, while Sydney Airport was on the dislikes list. Find out why.

Top stocks – how they fared

What moved the market?

- The OPEC meeting, which was expected to bring in deeper production cuts and a longer agreement from oil producers, weighed on energy and mining stocks.

- Retailers have been clobbered under the dark cloud of Amazon. The problem for this sector was underlined when the local division of Top Shop went into voluntary administration. JP Morgan also downgraded JB Hi-Fi and Myer.

- The US Fed expressed caution over raising interest rates too quickly.

Calls of the week

- Andrew “Twiggy” Forrest donated $400 million dollars to a number of causes including cancer research, early learning and eradicating slavery. It’s the biggest donation from any living Australian.

- Ansell pulled out of its condom business for $800 million dollars to a Chinese consortium. It will also buy back up to 10% of the shares on issue.

- And my mate Paul Rickard told the banks – who are still reeling from the Government’s surprise levy – to stop whinging and move on! Read his article here.

The week ahead

Australia

- Tuesday May 30 – Building approvals (April)

- Wednesday May 31 – Private sector credit (April)

- Thursday June 1 – Business investment (March quarter)

- Thursday June 1 – Retail trade (April)

- Thursday June 1 – CoreLogic home prices (May)

- Thursday June 1 – Performance of Manufacturing (May)

- Friday June 2 – New home sales (April)

Overseas

- Tuesday May 30 – US Personal income/spending (April)

- Tuesday May 30 – US CaseShiller home prices (March)

- Tuesday May 30 – US Consumer confidence (May)

- Wednesday May 31 – US Pending home sales (April)

- Wednesday May 31 – US Beige Book

- Thursday June 1 – US ADP National Employment (May)

- Thursday June 1 – US New vehicle sales

- Friday June 2 – US International trade (April)

- Friday June 2 – US Non-farm payrolls (May)

Food for thought

Our greatest weakness lies in giving up. The most certain way to succeed is always to try just one more time – Thomas A. Edison

Last week’s TV roundup

- What’s wrong with the Aussie market, and what could turn it around? CMC Markets’ Michael McCarthy discusses this and more.

- ST Wong from Prime Value shares his views on the stock market and the companies he’s watching right now.

- To talk about the impacts from the bank levy, and if the retailers are being over-shorted from the Amazon effect, Paul Rickard joins Super TV.

- With the big-cap stocks seemingly becalmed, some analysts think small-cap companies could start carrying the market. To discuss the stocks he’s watching, Bill Laister from Contango Asset Management joins Super TV.

- And ahead of the super changes set to come in on July 1, Assistant Commissioner – Superannuation at the ATO, Graham Whyte, shares the information the Office has to help with tax-related questions.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week one of the biggest movers was Independence Group, with its short position increasing by 0.91 percentage points to 13.16%. Orocobre went the other way, with its short position decreasing from 22.95% last week to 21.52% this week.

Source: ASIC

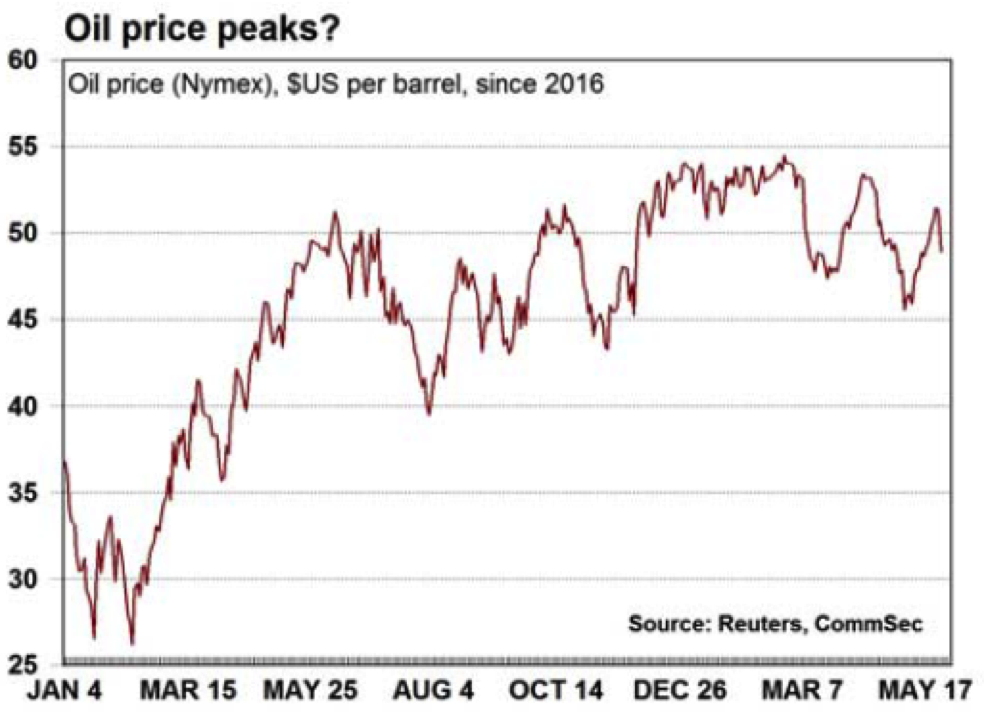

Chart of the week

Has the oil price peaked? The chart above shows the price of Nymex since 2016. Since the OPEC meeting, it’s fallen to around US$49 a barrel.

Top five most clicked stories

- Paul Rickard: Product Road Test – Contango Global Growth

- Tony Featherstone: Tourism boom: 3 stocks to watch

- Peter Switzer: Playing the Trump Trumping – don’t forget this lesson!

- Tony Featherstone: 5 undervalued LICs

- Paul Rickard: Do you want to take the short sellers on in JB Hi-Fi or Harvey Norman?

Recent Switzer Super Reports

- Thursday 25 May, 2017: Watch consumer spending

- Monday 22 May, 2017: How to play the stock market

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.