The question “Is Telstra buy, yet?” is probably the number one question I receive from investors. It has been this way for some months now, and follows a period of very ordinary share market performance by the company.

Telstra Share Price – March 2012 – March 2017

When I reviewed Telstra on 21 November last year (click here), I concluded by saying:

“I think it is unlikely that the market will re-rate Telstra upwards until there is more clarity on its capital strategy and evidence that its productivity/capital investment agenda is working. A steadier bond market will also provide support. While Telstra will be supported by income investors, particularly in any market sell-off, growth investors will continue to look elsewhere.

Sure, the dividend yield is attractive, and given that Telstra has yet to conduct an earlier announced on-market buyback, there is going to be buying support. So, I can’t recommend a sell. Buy more? I am not convinced there is any real hurry, so in weakness, targeting $4.50 to $4.75 range.”

And this is exactly what has happened over the last few months. Telstra’s shares have wallowed. Including the 15.5c dividend, Telstra has returned -1.8%, whereas the overall market since 18 November has returned (including dividends) 9.3% – an underperformance of around 11%.

This period covers Telstra’s disappointing first half results, which were released on February 16.

Telstra’s woes

Telstra has three core problems to address.

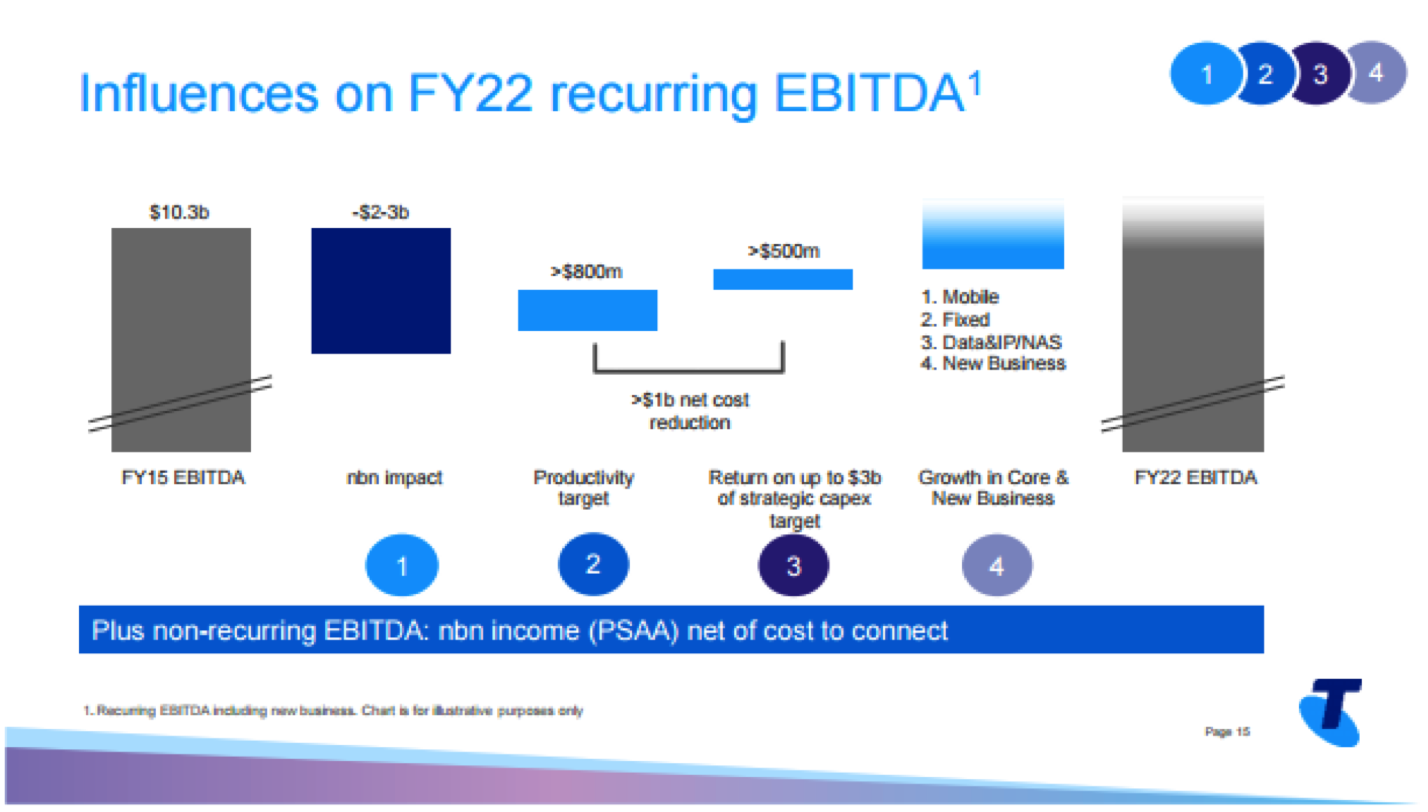

Firstly, it has an NBN (National Broadband Network) earnings hole to plug as customers switch from using the Telstra infrastructure to that provided by the NBN. In the long term, this is material and has been quantified by Telstra as having a negative impact on EBITDA of $2bn to $3bn annually.

For comparison, Telstra’s total EBITDA in FY17 is forecast to be around $10.8bn. Its dividend payment of 31c per share in FY17 will cost around $3.7bn, so if EBITDA is impacted by $2bn, you could see the dividend cut in half in FY22.

To address the NBN hole, Telstra has initiated a productivity program, is increasing capex to drive long run revenue and cost benefits, and says that it will grow revenue in its core and new businesses.

The productivity program is under the stewardship of CFO Warwick Bray and aims to find $800m of cost savings. This will focus on four key themes – improving the end-to-end customer experience; product and process simplification; reducing complexity in Telstra’s organisational structures; and supplier partnerships to reduce costs.

Independent of this program is a strategic investment of $3bn over the next three years into the core businesses. This will take the capex to sales ratio to 18%. The investment is targeting run rate benefits in excess of $500m annually, which they expect to fully realise by FY2021, with two thirds coming from revenue and one third from cost improvements. Of the $3bn, $1.5bn is earmarked for networks and re-inforcing network differentiation, $1.0bn for digitization to cover all forms of interaction between Telstra and its customers, and $0.5bn for projects improving the customer experience.

Assuming that these initiatives deliver a $1.3bn improvement in EBITDA, the balance of approximately $0.7bn to $1.7bn will be covered by revenue growth from Telstra’s four main products – mobile, fixed (including reselling NBN access), data and NAS (Networks, Applications & Services) and new business.

But that leads to the second problem – revenue is not growing. In fact, revenue fell in the first half of FY17 by 0.7% to $13.7bn. While there were some one offs due to regulatory pricing decisions, recurring core revenue fell by 0.4% compared to the same half in FY16.

Critically, revenue in the mobile division, which accounts for 39% of its sales revenue, fell on a recurring basis by 2.4%. This came despite Telstra adding 200,000 retail customers in the first half, taking their subscriber base to 17.4 million.

The revenue decline in mobiles largely reflected a decline in mobile broadband revenue, which fell by 14.7% to $545m, as customers shifted from the old dongle plans to newer tablet plans at lower ARPU (average revenue per unit). Reflecting on-going competitive pressures, post-paid handheld retail mobile ARPU declined to $67.26 in the December half, down from $67.82 in the June half.

Telstra says that it has seen some encouraging signs of stabilisation of revenue, ARPU and margin in the mobiles business. This will need to be the case, because the fixed division, which includes both the old fixed voice business and new NBN retail business, saw a revenue fall of 5.2%. Data and IP was down by 3.4%, while the Network Applications and Services business, which makes up 11% of Telstra’s sales, increased revenue by $225m or 18% to $1,475m.

The third problem for Telstra is the sustainability of the dividend. Free cash flow in the last half fell to $1.4bn, down from $1.9bn in 1H16. While this is expected to improve in the second half, with Telstra guiding for a full year free cash flow in the range of $3.5bn to $4.0bn (implies second half of $2.1bn to $2.6bn), the total dividend payment that Telstra will make for the full year is $3.7bn. Add in interest costs of $0.5bn, and Telstra requires free cash flow of circa $4.2bn.

Of course, Telstra could reduce its capex but it has said that it plans to increase this as part of the efforts to plug the NBN hole. Another option is to increase borrowings, however, this appears unlikely as the overriding and consistent feedback from shareholders in the Company’s ongoing capital review has been the importance of retaining a strong balance sheet. Telstra says that it is committed to retaining balance sheet settings consistent with an A band credit rating.

The most likely outcome is that the dividend will remain unchanged over the next couple of years. However, a cut down the track can’t be ruled out unless Telstra can find a way to boost earnings, either by increasing revenue, or slashing costs.

The Brokers

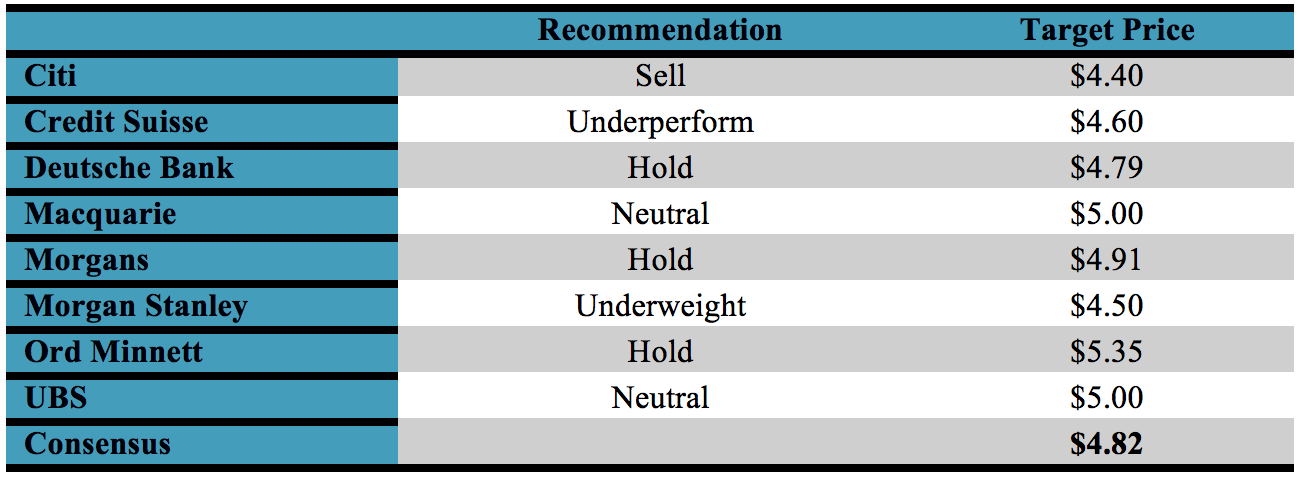

Broker sentiment remains negative, with 3 sells and 5 neutrals. Most brokers were disappointed with the first half results, and although supportive of Telstra’s actions to plug the NBN hole, are not yet convinced that they are going to be sufficient According to FN Arena, the consensus target price (for the 8 major brokers) is $4.82, a 2.8% premium to the current share price of $4.69. Individual recommendations and target prices are set out below.

Broker Recommendations and Target Prices

The Brokers have Telstra trading on a multiple of 14.9 times forecast FY17 earnings and 13.8 times FY18 earnings. They forecast a dividend of 31.0c fully franked in FY17, and 31.1c in FY18. At a price of $4.69, this puts Telstra on a forecast dividend yield of 6.6% pa (9.4% pa grossed up).

Guidance reaffirmed

Accompanying the half-year results, Telstra re-affirmed its guidance for the full year. A small but important change was made to the income target, with the outcome for the full year now likely to be at the bottom end of the ‘mid to high single digit’ range.

Guidance measures in place for FY17 are as follows:

Bottom line

As I mentioned at the start of this article, I think it is unlikely that the market will re-rate Telstra upwards in the short term. The market is not yet convinced that Telstra is on track to close the NBN hole and remains worried about ongoing competitive pressures. It will, however, be supported by investors who are attracted by the dividend yield.

For me, this means that Telstra will underperform. In a bull market, it will lag the rest of the market as it moves higher, while in a bear market or correction, it is likely to be supported by dip buyers.

So, is Telstra a buy, yet?

Well, I think it depends on who you are. If your priority is income, then around $4.50 to $4.75 isn’t too bad a level to get set at. But I also think you can be patient. I don’t get a sense that the Telstra is going to run away from you. So, you can perhaps target multiple entry points.

And if Telstra gets good at delivering “brilliant customer experiences” (the first pillar of Telstra’s strategy), then maybe the market might re-rate the company earlier. Unlikely.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.