The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are APN News and Media with 33.47% and Domino’s Pizza Enterprises with 26.8%.

[table “264” not found /]

In the good books

AUTOMOTIVE HOLDINGS GROUP LIMITED (AHG) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 5/1/1

First half operating cash flow was well below estimates. Those hoping for a quick divestment of the troubled refrigerated logistics business may be disappointed but Credit Suisse believes management’s strategy to try and improve the asset is correct, whether or not it is ultimately sold.

The broker believes regulatory risk is manageable and the FY17 growth outlook achievable. Upgrade to Outperform from Neutral. Target is lowered to $4.35 from $5.20.

MG UNIT TRUST (MGC) Upgrade to Add from Hold by Morgans B/H/S: 1/1/0

First half result was weaker than expected. Morgans expects FY17 will be a tough year but this should be as bad as it gets as the eventual return of a more normal season and management’s initiatives should turn things around.

While acknowledging the risk, the broker upgrades to Add from Hold, believing that patient investors will be rewarded by a better year in FY18. Target is reduced to $1.20 from $1.25.

MEDUSA MINING LIMITED (MML) Upgrade to Neutral from Sell by Citi B/H/S: 0/2/0

It was a weak result, as expected, comment analysts at Citi. They have reduced estimates and the price target to 38c from 45c in response.

However, the savage share price response has now triggered an upgrade to Neutral from Sell. Also, the analysts flag that the company might need some near-term funding, estimated at circa US$5m, for working capital.

SOUTH32 LIMITED (S32) Upgrade to Buy from Neutral by UBS B/H/S: 6/1/0

UBS upgrades to Buy from Neutral, believing metallurgical coal and manganese prices are stabilising and valuation metrics now look compelling.

The broker believes the stock offers a free cash flow yield of over 15% with out-of-cycle returns possible in the June quarter. The company has stated at its results briefing that was very close to being able to justify returns to shareholders and UBS believes this will increasingly be the case.

Target is raised to $2.80 from $2.75.

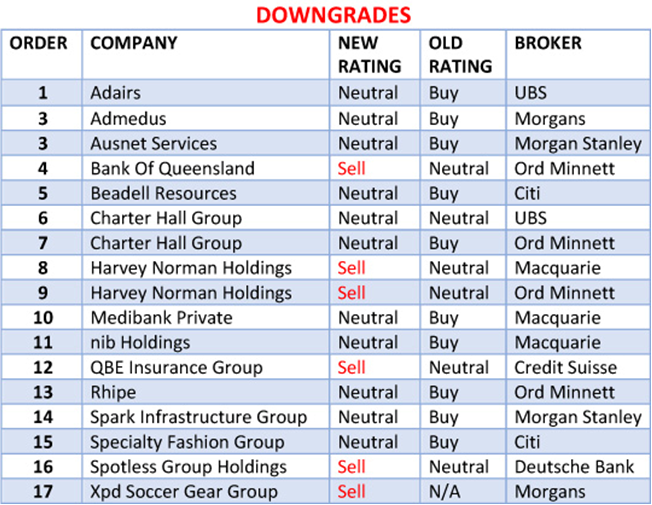

In the not-so-good books

BANK OF QUEENSLAND LIMITED (BOQ) Downgrade to Lighten from Hold by Ord Minnett B/H/S: 1/5/1

Ord Minnett forecasts first half cash earnings of $171m, which incorporates a -5% downgrade. This reflects a lack of volume growth, margin weakness from deposit competition and re-basing of trading gains.

Importantly, the lack of growth in the first half means the bank can maintain the interim dividend at $0.38, despite it translating into an 85% payout ratio. Order Minnett downgrades to Lighten from Hold. Target is reduced to $11.00 from $11.25.

MEDIBANK PRIVATE LIMITED (MPL) Downgrade to Neutral from Outperform by Macquarie B/H/S: 0/6/2

With the recent share price performance narrowing the discount to Macquarie’s price target, the rating is downgraded to Neutral from Outperform.

The broker does not believe the investment case is supported at current levels, given the combination of moderating industry premium growth and operations at, or near, peak margins.

Claims growth remains materially below long-term trends, which is a risk to the broker’s view. The other risk is a structural change to address the policy-holder mix and lack of growth amongst younger members. Target is $2.95.

NIB HOLDINGS LIMITED (NHF) Downgrade to Neutral from Outperform by Macquarie B/H/S: 1/6/0

With the recent share price performance narrowing the discount to Macquarie’s price target, the rating is downgraded to Neutral from Outperform.

The broker does not believe the investment case is supported at current levels, given the combination of moderating industry premium growth and operations at, or near, peak margins.

Claims growth remains materially below long-term trends, which is a risk to the broker’s view. The other risk is a structural change to address the policy-holder mix and lack of growth amongst younger members. Target is $5.50.

RHIPE LIMITED (RHP) Downgrade to Hold from Buy by Ord Minnett B/H/S: 1/1/0

First half results were worse than expected. FY17 revenue guidance has again been lowered, although the EBITDA target of $4m is unchanged.

Ord Minnett points to a seemingly quick slowdown in the profitable private segment, where the broker envisaged key competitive advantages. Medium-term forecasts are reduced significantly and the rating is downgraded to Hold from Buy. Target falls to $0.46 from $1.00.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.