At around $2.50 per share, many value investors will have been tempted to have a nibble (or a mouthful) of AMP. It wasn’t that long ago that this supposed blue-chip company was trading at $5.47 (it peaked in March just six days before the first round of public hearings at the Royal Commission).

The question is this: is AMP a buying opportunity now, or will you just “catch a falling knife”? Here is what I think.

The latest dip

AMP Share Price- Oct17 to Oct18

Source: nabtrade

AMP’s latest share dip came after it announced the sale of its Australasian life insurance businesses to Resolution Life for $3.3 billion, and a re-insurance deal for its NZ retail wealth protection worth $150 million. The complex sale, which involves both cash and non-cash proceeds, will see AMP net about $2.17 billion after separation costs, and the replacement of hybrid capital and debt. Of this amount, $1.06 billion will be in cash and $1.12 billion in income generating investment assets.

AMP will also seek divestment of its New Zealand wealth management and advice businesses via an IPO in 2019.

The deal to sell the insurance business (AMP calls this “wealth protection and mature businesses”) was priced at a multiple of 0.82 times embedded value (an actuarial estimate of the present value of future profits plus net assets). While noting that the sale would simplify the AMP business, some analysts were disappointed with the price. Commonwealth Bank, for example, achieved a multiple of 1.1 times when it sold CommInsure and Sovereign NZ to AIA in September 2017.

The sale will also have an impact on the earnings of the largest of AMP’s continuing businesses, Australian wealth management. Because of the unwinding of internal distribution agreements, the sale will lead to a reduction in operating earnings for that division in the order of $80 million to $90 million per annum (the division earned $204 million in the first half). There are also “stranded” group office costs of $40 million per annum that won’t be recovered.

AMP said that it would exclude the second half earnings of the discontinued businesses (Australasian life insurance and NZ wealth management) when determining the final dividend for FY18 (AMP operates on a calendar year basis). This means that second half dividend is likely to be cut from 14.5c in FY17 to around 8c to 10c in FY18, taking the full year dividend from 29c in FY17 to perhaps as low as 18c for FY18.

Investors were also disappointed about a net outflow of funds in wealth management assets of $1.5 billion in the September quarter, reflecting a continued weakness in inflows and elevated outflows. On the back of this news, the AMP share price got clobbered, finishing on Friday at $2.38, a fall of 26.5% over the week.

What do the brokers say?

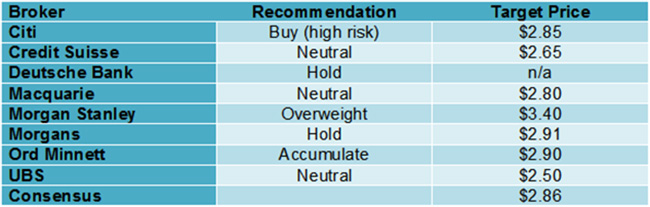

Each of the major brokers cut their target price for AMP following the announcements last Thursday. According to FN Arena, the consensus target price is now $2.86, a 20.1% premium to Friday’s closing price.

Two brokers upgraded (Citi to Buy/High risk from Neutral and UBS to Neutral from Sell), while Credit Suisse downgraded to Neutral from Outperform. Overall, there are three buy and four neutral recommendations. Individual recommendations and target prices are set out in the table below.

Major Broker Recommendations

On a forecast basis, the brokers have AMP trading on a multiple of 10.6 times FY18 earnings and 10.5 times FY19 earnings. They currently expect a full year dividend of 19c for FY18 and 19c for FY19 – which puts AMP on a prospective yield of 8.1%.

Morgans warns that “while the stock appears cheap, it will be hard to become positive until the outcome of the Royal Commission recommendations is clearer and the strategy of the incoming CEO is known.” This sentiment is shared by Macquarie, which says that “with RC fallout still to come, near term risks to funds flow and new CEO sure to re-base expectations, no opportunity for outperformance from here”.

On the other hand, Morgan Stanley and Citi cite the prospect of capital management initiatives, possibly through a buyback, and further cost reductions. Ord Minnett suggests that the remaining businesses have growth prospects.

Will you catch a falling knife?

The arguments for the “falling knife” are:

- There is no sign that AMP’s share price has yet bottomed. While share prices can bounce quickly off a bottom, they usually do a fair bit of work and trade sideways before reversing trend;

- AMP suffered incredible reputation and brand damage with the Royal Commission. The impact to funds flow, on planner numbers, with clients and ultimately earnings could be material and prolonged;

- As the brokers note, new CEO Francesco de Ferrari starts work in December. It is not unusual for incoming CEOs to “re-base expectations”.

Against this are:

- Compared to valuation, on a multiple of earnings, and dividend yield, AMP is attractively priced;

- AMP’s exit of its Australasian life insurance businesses and NZ wealth management business was as a result of the completion of its portfolio review. It has resulted in a significant simplification of the portfolio, which reduces complexity and should reduce earnings volatility;

- AMP’s balance sheet has been strengthened, which provides options for investment in growth businesses and/or capital management initiatives.

My view?

Buy, but high risk.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.