The Australian Bank sector has lost $50b in value since the Federal Budget and I think that’s trying to tell you things get tougher from here in Australia.

As you know, I am concerned about the Australian economy in the second half of 2017 (and beyond) and particularly concerned about consumer spending as household cash flows are squeezed.

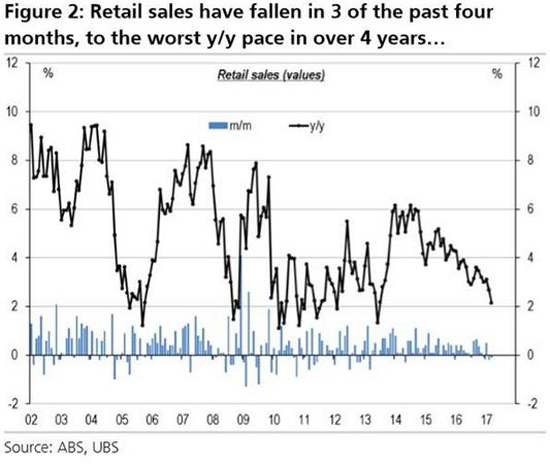

Australian retail sales have slumped and this is despite consumer confidence readings remaining upbeat. The fact the three of the last four months have recorded month-on-month retail sales falls is genuinely concerning.

Similarly, the number of shoppers at shopping centres, strip shops and discount centres has fallen -4.4% this year vs. 2016. This is an issue for retail landlords, who charge high rents on the premise that foot traffic will be strong.

Falling retail sales and falling shopper numbers are often the precursor to a broader economic slowdown.

It’s worth remembering that “consumption” is 57% of Australian GDP of which 30% is “retail”. Retail is also the largest sectorial employer.

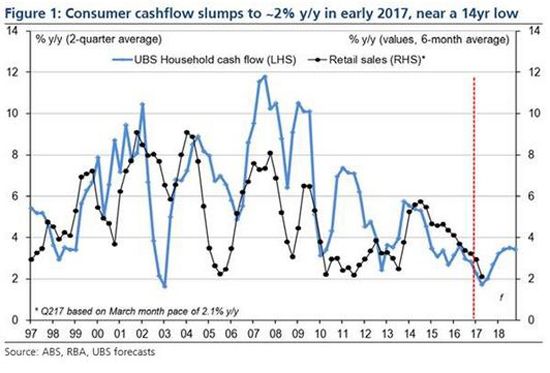

Investment Bank UBS recently attempted to reconcile what was driving this sharp drop in retail sales. UBS’s view is below.

“We’ve updated our household cash flow model, which looks at consumers “free cash” after taxes and debt interest payments, and after their utilities and petrol costs. The results are revealing. In short, cash flow has slumped into early 2017. While low interest rates and fallen petrol prices have softened the blow from slowing wage growth in recent years, with still low wages growth, and renewed rises across utilities, debt interest and petrol costs, household cash flow is under significant renewed downward pressure”.

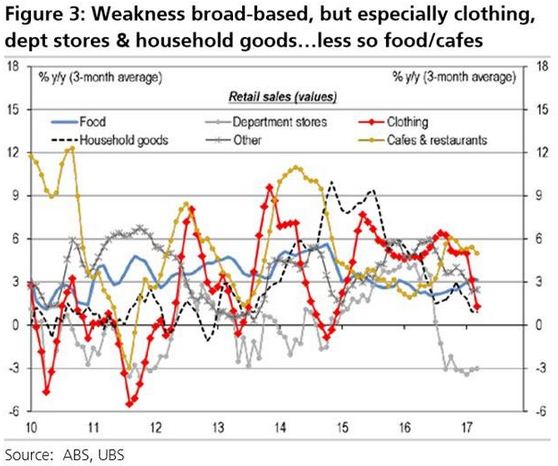

I absolutely agree with this view and can feel it in my own daily life. I’m sure most of you can too. What this means is people will continue to pay their mortgages, pay their utility bills, pay their toll road bills, and buy consumer staples. However, for consumer discretionary sectors, this is a BIG problem.

A lack of free household cash flow basically drives consumers to focus very hard on price when buying staple items and rules out most forms of discretionary consumption.

This is all occurring BEFORE AMAZON arrives in Australia and crushes margins in a variety of discretionary retail sectors.

My fund owns AMZN shares and we believe AMZN would be prepared to lose money in Australia for a decade to gain a footprint. The big driver of AMZN in the US has been Amazon Prime, a $79 annual fee that allows unlimited free delivery. When combined with voice assistant Alexa, this has driven major structural headwinds for high cost bricks & mortar retailers.

The combination of falling household free cash flow and Amazon arriving in Australia is potentially a very nasty combination for Australian discretionary retailers. You can see Harvey Norman (HVN), JB Hi-fi (JBH), Super Retail Group (SUL), The Reject Shop (TRS), Oroton (ORL), RCG Corp (RGC), Myer (MYR), Premier Investments (PMV) and all the listed retail landlords have been under significant share price pressure in recent months to reflect both these developments. About the only “winner” has been Goodman Group (GMG), which is expected to provide large-scale warehousing/logistics services to Amazon in Australia.

I absolutely DO NOT think this is a dip to buy in Australian discretionary retailers or retail landlords. This has every chance of being a structural industry change event combined with a medium-term downturn in household free cash flow.

In fact, I don’t think any retailer is going to be immune and that brings me to the largest diversified retailer, Wesfarmers (WES).

Through time, Wesfarmers has been one of Australia’s greatest companies. But what tends to happen is investors start to believe the company has some kind of “special sauce”.

If WES has a ‘special sauce,’ it is capital allocation discipline through the cycle, but that doesn’t make them immune to structural industry change.

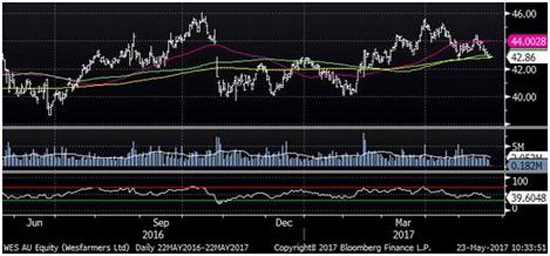

To put this in perspective, Wesfarmers (WES) shares have basically gone sideways for 4.5 years. Yes, they have paid a nice 5.00% fully franked dividend per annum, but capital growth hasn’t occurred.

WES: SIDEWAYS

To put this in context, Amazon (AMZN), which paid zero dividend yield over the last 4.5 years, delivered capital growth of +250%.

Ok, not fair I know, but it does remind you that if you buy high dividend yields, you usually get low capital growth, and vice versa.

So why am I cautious on Wesfarmers (WES)?

Firstly I have always seen WES as a listed “private equity” group. However nowadays, they are a small “private equity” group ($48b mkt cap) by global standards and competition for deals/assets is much more aggressive than in previous decades, due to the unprecedented inflow into private equity funds. I think WES will struggle to compete with the global private equity giants.

Secondly, long standing CEO Richard Goyder is leaving. This comes at during what I see as a period of structural change for most of the industries WES operates in. I don’t think it’s an ideal time to change CEOs. In my memory, and generally with the benefit of hindsight, long-standing CEOs tend to time their departures well. Good luck to Richard, he has done a solid job. However, the change of leadership does increase overall execution risk.

Thirdly, I think all WES’s industrial consumers businesses are going to face prolonged, increasing competitive pressure, while at the same time facing consumer spending weakness. The combination of slowing revenue growth/backwards revenue growth and margin pressure is never a good one.

Coles, Bunnings, Officeworks, Target and Kmart all will come under further competitive pressure in the months and years ahead.

Coles Supermarkets (38% of 1H WES EBIT) are seeing renewed competitive pressure from a reinvigorated and refocused Woolworths. Aldi continues to gain market share and increase its store rollout. Food price inflation remains weak and margins are in structural decline. I actually believe Australian supermarkets have never been more competitive on price, but that will lower long-term margins as they all invest in “price”. Small swings in supermarket EBIT margins have a large effect on profitability.

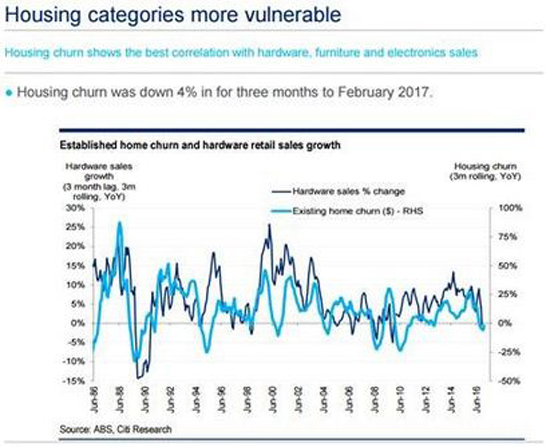

The other major swing factor in all this is Bunnings Australia & New Zealand (32% of 1H WES EBIT), which I think is seeing peak cycle earnings right now. This is “Jack Nicholson” for Bunnings (aka As Good as It Gets). Bunnings is WES’s 2nd largest EBIT contributor behind Coles.

The Australian new home construction cycle has peaked, the new apartment construction cycle has peaked, the house price cycle is peaking, the DIY home renovation cycle is peaking. Price competition in hardware will increase.

The chart below from Citi Research confirms that overall “hardware” sales track house churn. In other words, the number of houses changing hands affects hardware sales. That makes perfect sense to me.

Just like Coles had a great run of it while Woolworths was in disarray, Bunnings has clearly benefitted from the Masters debacle.

I also struggle to believe Bunning’s roll-out/rebranding of the 500 odd Homebase stores will go that smoothly. The price Bunnings paid for Homebase (UK’s 3rd player in hardware) looks full, particularly now the British Pound has collapsed vs the Australian dollar after Brexit. If the Pound stays down, the repatriated profits from Bunnings UK will be less than forecast, but the good news is repatriated losses will be less in the first few years on conversion.

You can see Harvey Norman shares (orange line) are pricing in a cyclical downturn in housing related revenues (renovations etc.) and this is coming to Wesfarmers (white line) and investors realise Bunnings is not immune to the same top down pressures.

HVN vs WES

The way I see this playing out is WES’s FY17 annual result in August will be underwhelming. This will lead to analyst downgrades to FY18 consensus forecasts and WES will start looking relatively expensive for its complete lack of growth. The dividend yield will remain somewhat supportive but you may well get the odd analyst start to question the sustainability of the high dividend pay out ratio.

At the same time, overall Australian retail sales will continue to disappoint and the noise about Amazon’s entry into Australia will increase.

WES currently trades on a small P/E premium to the ASX200. However, paying 16x FY18 earnings for no earnings growth, and potentially negative earnings growth, is not an attractive proposition to me. In fact, I do wonder whether WES is still trading on 16x because it’s simply a large weighting in the ASX200 in what is a passive investing bubble? I also suspect WES is a member of many “high yield” ETFs and funds.

Yes, the dividend yield of 5.00% fully franked is relatively attractive, but you are being paid 80% of EPS as DPS and that leaves little upward flexibility in that pay out ratio. If I am right and the EPS comes under pressure, then the dividend will be under a little pressure to be sustained. The group ROE of 10.2% is also a little disappointing, considering Bunnings generates an ROE of 30%.

I tend to wonder whether it is this dividend yield alone that “seduces” WES investors. If WES didn’t yield 5.00% fully franked, would you want to own a piece of Coles, Bunnings, Officeworks, Kmart and Target into a structural change in the Australian retail landscape and household cash flow squeeze?? I wouldn’t and that is why the AIM Global High Conviction Fund is short Wesfarmers shares. We are prepared to pay away the dividend and franking credits, believing our capital gains from WES share price falls in the months ahead will more than offset the dividend and franking credits. I am of the view WES will fall below $40.00.

And finally, the technical perspective for WES looks precarious, with a move down through the 50,100 and 200-day moving averages now confirmed.

Australian households are in a cash flow squeeze. Wesfarmers (WES) will not be immune to the negative effects of this extended household cash flow squeeze. In fact, there is no stock more exposed by dollar value of retail revenue generated in Australia than WES.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.