The big news stock market stories have come out of the States, with the US economy growing at a huge 4.1% for the second quarter. However it didn’t help the share indexes, with tech stocks losing friends, adding to the Nasdaq’s woes, following Facebook’s 19% slump in its share price on Thursday.

The good growth number was expected but it does confirm that the world’s most important economy, in making sure the IMF’s global growth guess of 3.9% works out, has delivered. On the other hand, it must be making those who worry about upcoming Fed rate rises more concerned, so some of the sell off in stocks overnight would be a reflection of those fears.

Some reports suggested that a bigger number was possible. Maybe that’s out there waiting to happen, with President Trump saying “we’re going a lot higher.” This guy is on a roll, with the EU trade concessions he won, averting a Europe/USA trade war, so it’s not easy to doubt him.

All three indexes headed south but the real drivers of negativity were tech stocks. Intel and Twitter came up with news that didn’t impress the market so they were slugged. And here’s a really important point to remember for our reporting season – if a company is priced to perfection, even slightly bad news brings a big markdown.

Twitter actually delivered a profit result as expected but reported a drop in users and that news was not well-received.

Meanwhile, FactSet says, at the 50% mark for US reporting, where half the companies in the S&P 500 index have done show-and-tell, 79.8% have come in with better-than-expected earnings.

On the home front, it’s been a week where we hit a 10-year high for stocks, finishing out the week at 6300.2, after a 0.2% gain for the S&P/ASX 200 index. However, the story was helped by Friday’s nice 55.7 point (or 0.89%) gain.

It was hard to pinpoint a local reason for the rise and AMP Capital’s Shane Oliver saw it this way: “Share markets mostly pushed higher over the last week helped by good US earnings news and a US/European trade agreement.”

That said, there seems to be an undercurrent of positive sentiment towards stocks, helped by the re-loving of banks and the fact that commodity prices are holding up. The Bloomberg Commodity Index was up 2% for the week and Fairfax says it was “its best weekly performance since October 2017.”

BHP Billiton rose 4.5% to $34.40 this week, with the company telling the market that it has sold its US shale assets for $US10.5 billion. Rio put on 1.6% to $81.38 over the week, South32 rose 2.5% to $3.63 but Fortescue had a tough week at the office. It started around $4.43, topped out at $4.62 on Wednesday but lost friends (after reporting only OK) to end the week at $4.35.

The AFR picked out the negative to explain the share price drop: “The company confirmed it had received 64% of the benchmark iron ore price in the year to June 30. The company had initially expected to receive between 75% and 80% of the benchmark price, but China’s growing preference for high grade iron ore has seen bigger discounts applied to the lower grade ores that Fortescue sells.”

Anyone wanting a leg up for a rare earths company shouldn’t ignore this from UBS that said Lynas “had the best global Rare Earth deposit” in their view. The stock popped 15.4% on the revelation.

And I can’t ignore Nine Entertainment’s feisty bid for Fairfax, which will result in a new company called Nine but it still has to be given the green light by the regulator. Interestingly, Fairfax shares only closed flat for the week at 80.5 cents but Domain shareholders loved the news, rising 8.1% to $3.35. Nine’s shareholders had to cop a 13.1% hiding because of the company’s vision, taking its share price to $2.19!

And while some might have thought the stock market was sexist, clobbering Macquarie’s share price when it was announced that its CEO Nicholas Moore would soon retire and be replaced by Shemara Wikramanayake, history tells us that when a good boss leaves a company, its share price fall, unless the incumbent is a bum and the replacement is a god! Shemara has a huge reputation and her appointment isn’t a surprise to expert Macquarie watchers. Macquarie’s share price rose 1.19% on Friday to $124. Compared to other analysts, Morgan Stanley remains a big fan of the bank: “Morgan Stanley has retained their $130 price target for the company, forecasting that the bank will continue to pay strong dividends per share, rising to $6.54 a share in 2021 from $5.25 a share in 2018.” (Fairfax)

By the way, anyone wondering why gold and other precious metal prices fell from mid-week, can blame the EU deal with President Trump, which dodged a trade war bullet. Gold is still loved when scary economic and geo-political stuff is going on.

That’s the wrap of the past but I’m excited about the next few weeks, where I hope the improving economic news for the Oz economy translates into better-than-expected company earnings. Shane Oliver is sharing my excitement and this is how he summed up what lies ahead: “Australian June half earnings reports will start to trickle through with Rio, Janus Henderson, and Genworth reporting on Wednesday and Resmed on Friday,” he wrote in his weekly note. “We are expecting 2017-18 earnings growth to come in around 7%, with resources earnings rising around 20% (albeit down from 130% in 2016-17), thanks to solid commodity prices and rising volumes and the rest of the market seeing profit growth of around 4.5%.”

I found Shane’s final summary of what’s expected interesting: “Strong results are expected for insurers, health care, gaming, building materials and utilities, offsetting softness for telcos, banks and consumer stocks,” he forecasted.

And as someone who has a dividend and growth fund in SWTZ, I liked this from Shane: “Dividend growth is likely to remain solid.”

What I liked

- Prices of intermediate goods rose by 0.9% in the June quarter to stand 4.1% higher over the year – the strongest annual increase in 6½ years. Preliminary stage materials rose by 1.1% in the quarter to be up 4.4% over the year – the strongest annual gain in four years.

- The Aussie dollar fell from highs near US74.45 cents to lows near US73.70 cents and was near the lows in late US trade on Thursday.

- The Internet Vacancy Index fell by 1% in June after decreasing by a downwardly-revised 1.2% in May. The index is 4.2% higher than a year ago and is still at levels last seen six years ago.

- Official figures show that the US economy grew at its fastest pace in nearly four years in the second quarter, expanding at an annualised rate of 4.1%. Importantly, the growth was driven by a big spike in consumption and exports.

- The US Markit ‘flash’ manufacturing purchasing managers index rose by 0.1pt to 55.5 in July. Any number over 50 means expansion.

- The US Markit ‘flash’ services gauge fell by 0.3pts to 56.2pts in July but, like the above, the sector is still expanding.

- The European Commissioner and the US President agreed not to impose new tariffs on autos while discussing other trade issues.

- European Central Bank President Mario Draghi vowed to keep interest rates at low levels “through the summer of 2019”.

- The Chicago Fed National Activity index rose by 0.88pts to 0.43pts (survey: +0.25pts) in June.

What I didn’t like

- The Consumer Price Index (or inflation) rose by 0.4% in the June quarter, below expectations for a lift of 0.5%. In seasonally adjusted terms, the CPI rose by 0.5%. The annual rate of headline inflation lifted to 2.1% in the June quarter from 1.9% in the March quarter. But the seasonally adjusted annual growth rate lifted to 2.2% (also from 1.9%).

- The weekly ANZ-Roy Morgan consumer confidence rating fell by 2.1% to 118.9 but was still above the average of 114.0 since 2014 and the average of 113.0 since 1990.

- US durable goods orders rose by 1% in June but the tip was a 3% rise.

- Shares in Facebook fell by 19%, wiping around $110 billion off its market capitalisation, in response to a disappointing earnings result.

Kiwi centurions behind Centuria

Many of you might have been introduced to the property company Centuria Capital Group through our Switzer Report and its investments have been impressive. Over a five-year period, its share price has doubled and its unlisted property plays have been very rewarding for its followers.

The centurions behind this company are a couple of consistently performing Kiwis: John McBain is chairman and Jason Huljich is Head of Real Estate and Funds Management. After catching up with them last Thursday, I couldn’t help but invite them to an upcoming lunch where the ex-PM of New Zealand, Sir John Key, will speak to my team at Switzer. Naturally I’ll share any gems that come out of this day with you in this Report.

The only shortcomings that these three Kiwis have are that they are tragic All Blacks fans, though I guess that’s where they learnt how to win!

The Week in Review:

- You might not like to hear this, but now’s the time to do an objective test on your ability to manage your own money. I offered the money-making test all DIY fund managers have to sit!

- Paul Rickard followed on with that theme to ask: Has your super fund done better than 9%? And what to do if it hasn’t.

- How do you know if a company is going to outperform? It’s difficult but here are a few tricks. James Dunn offered 6 secret tips for valuing an IPO.

- Our Hot Stock this week was DMP by chartist Gary Stone of Share Wealth Systems, find out why!

- In our first Buy, Hold, Sell – what the brokers say, resources related companies were a focus, with upgrades for Alumina and Evolution Mining. And in the second edition, a review of AREITs by Citi resulted in a slew of downgrades.

- Where do you look for yield when the banks and Telstra stop delivering? Mark Christensen shared three great income stocks outside the top 50.

- Tony Featherstone recommended two education stocks you should keep an eye on.

- Graeme Colley explained what to do in the case of excess non-concessional contributions.

- Our Professional’s Pick this week was Royal Dutch Shell by Peter Wilmshurst.

- In Questions of the Week, we answered readers’ queries about how to plan ahead for franking credit changes and what to do about the Iron Mountain delisting from the ASX.

Top Stocks – how they fared:

What moved the market?

- Nine and Fairfax Media announced plans to merge in a deal that will see Nine shareholders own 51.1% of the combined entity, with Fairfax owning the remaining 48.9%. The new company will be called Nine, to be led by Nine CEO, Hugh Marks.

- BHP sold its US onshore oil and shale gas business to energy giant BP for $US10.8 billion ($14.6 billion).

- Facebook lost $US119 billion in value overnight Thursday, in the biggest single-day fall in US stock market history. Shareprices dropped 19%.

- Donald Trump and European Union leaders appear to have stepped back from the brink of a trade war, striking a deal to work towards “zero” tariffs, barriers and subsidies.

Calls of the week:

- Tony Featherstone made a call two on education stocks you should be keeping an eye on.

- Mark Christensen named three 3 great income stocks outside the top 50.

- Macquarie Group CEO Nick Moore made a call to step down, paving the way for the company’s first female CEO Shemara Wikramanayake.

The Week Ahead:

Australia

Monday July 30 – State of the States

Tuesday July 31 – Building approvals (June)

Tuesday July 31 – Private sector credit (June)

Wednesday August 1 – CoreLogic home value index (July)

Wednesday August 1 – Manufacturing purchasing manager surveys (July)

Thursday August 2 – International trade (June)

Friday August 3 – Services purchasing manager surveys (July)

Friday August 3 – New vehicle sales (July)

Friday August 3 – Retail trade (June)

Overseas

Monday July 30 – US Pending home sales (June)

Tuesday July 31 – China Purchasing managers indexes (July)

Tuesday July 31 – US Home price index (May)

Tuesday July 31 – US Personal spending/income (June)

Tuesday July 31 – US Consumer confidence (July)

Wednesday August 1 – China Caixin manufacturing (July)

Wednesday August 1 – US Federal Reserve interest rate decision

Wednesday August 1 – US ISM manufacturing index (July)

Wednesday August 1 – US ADP employment (July)

Thursday August 2 – US Factory orders (June)

Friday August 3 – China Caixin services (July)

Friday August 3 – US Non-farm payrolls (July)

Friday August 3 – US Trade balance (June)

Food for thought:

“The most difficult thing is the decision to act, the rest is merely tenacity. The fears are paper tigers. You can do anything you decide to do. You can act to change and control your life; and the procedure, the process is its own reward. – Amelia Earhart

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

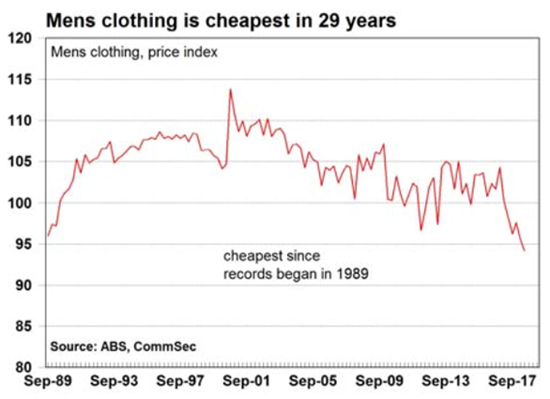

Charts of the week:

Source: Commsec

Source: Commsec

Top 5 most clicked:

- 3 great income stocks outside the top 50 – Mark Christensen

- This is the money-making test all DIY fund managers have to sit! – Peter Switzer

- Buy, Hold, Sell – what the brokers say – Rudi Filapek-Vandyck

- Has your super fund done better than 9%? – Paul Rickard

- Hot stocks – chartist’s view – Penny Pryor

Recent Switzer Super Reports:

- Monday 23rd July: Great minds

- Thursday 27th July: Outside the [top 50] box

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.