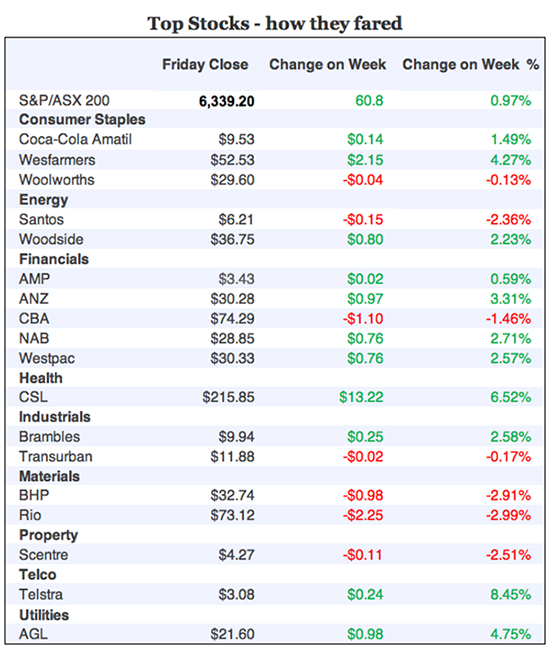

This week’s market action has been about the big T’s: Trump, Trade wars and Telstra. And despite the threatening clouds for stocks, I love it when our stock market marches against a global trend towards negativity. And that’s what happened this week. Our S&P/ASX 200 Index ended up 60.8 points (or 1%) for the week, finishing at 6339.2. This was a pretty heartening effort, with metal prices under pressure.

You can see that the US market was heading down until President Trump let it slip that his trade talk team would be talking to their Chinese counterparts later in August. This was Thursday in the States and the Dow liked it. And the uptrend was reinforced overnight when Donald let it out that he and President Xi were going to talk turkey – no, not the real Turkey – but the trade talk ‘turkey’ in November.

The Dow Jones Industrial Average

Source: finance.yahoo.com

“If you take the possibility of a trade war with China off the table for a few months, that allows the market to work its way higher,” said Ed Keon, chief investment strategist at QMA to CNBC. “This has been one of the market’s biggest worries. If you put it on the back burner, it’s a good thing.”

This has market players dreaming of the S&P 500 at 3000 for the end of the year.

Given we are outpacing the US market index, then if our S&P/ASX 200 index went up 5%, we’d end close to 6660! No, not the devil’s number! Why did I do that calculation?

Away from silly superstition, a big help to our market was the market’s acceptance of Telstra and its CEO, Andy Penn’s work-in-progress story, despite some ordinary profit news featuring an 8% slump in profit. The telco ended the week up 8.8% to close at $3.09 on Friday.

S&P/ASX 200’s rising week

Source: finance.yahoo.com

Those who noted and reacted to my surprise revelation a couple of weeks ago, when Roger Montgomery gave the company the loving thumbs up after years of hating the company, must be pleased. I have to say the size of the rise even surprises me but Roger reckons the lack of bad news this week from Penn gave the market confidence.

And what about the irrepressible CSL, which recorded a 29% increase in profit and expects growth to be strong in the year ahead, which led to a 6.5% rise in the company’s share price?

For anyone worried about Treasury Wine Estates, the SMH reported that Morgan Stanley has swallowed the company’s less than palatable report this week, to suggest $20 is a buyable target. The company announced its net profit after tax in 2018-19 was up 34% to $360.3 million but the market was a little concerned about fewer US wine shipments, following the company’s recent move to take control of distribution for a quarter of all sales in the US’s biggest states. Earnings in Asia also showed signs of slowing but even though the share price fell 2% to $19.02 on Friday, it did start the week at $18.20.

By the way, the dollar has fallen from 79 US cents in February to be now a tick under 73 US cents, which partly explains why our stock market is defying gravity, even with the Trump curve balls that keep on coming. Companies such as TWE, Macquarie and other overseas currency earners have got a free profit kick from the currency.

Overall for profit reporting, some 35% of companies have reported and this is how Shane Oliver of AMP Capital has scored it:

- 48% of results have surprised on the upside, compared to a norm of 44%.

- The breadth of profit increases is high, with 83% reporting higher profits than a year ago, compared to a norm of 66%.

- 89% have increased their dividends or held them constant.

- 64% of companies have seen their share price outperform the market on the day results were released.

But Shane reminds us that “the quality of results tails off in the last two weeks of the reporting season, so don’t get too excited just yet. 2017-18 earnings growth are on track to come in around 9%, with resources earnings up 25%, thanks to solid commodity prices and rising volumes and the rest of the market seeing profit growth of around 5%.”

In case you missed it, the RBA boss, Dr Phil Lowe, fronted up at Parliament to reveal his take on the economy. This is my summary:

- “It is more likely that the next move in interest rates will be an increase, not a decrease.”

- The transmission from strong employment growth to higher wages and inflation will happen, but slowly.

- Skills shortages are a worry, so if your kids need guidance, tell them to head towards information technology and engineering construction.

- On the housing market, the Governor welcomed the cooling of home prices in Sydney and Melbourne.

- Dr Lowe applauded the Turnbull government for the shrinking budget deficit.

- Dr Phil is a bit toey about Trump trade plays and the spiralling US budget deficit and debt situation.

One of the great efforts for our market was to avoid getting too spooked by Turkey, its collapsing lira and then associated fears for emerging market economies. Why Turkey should impact on Argentina, Indonesia and other unrelated economies confuses many normal people. As an economist, I think the link is a little screwy.

The only link I buy is this one: as the US dollar rises because of rising interest rates in the States, money that was drawn to emerging markets when official rates of interest were close to zero in the US, starts to go back there. And because this is believable and the word “contagion” is often tossed around in these speculative money markets, it all adds to fear, so these emerging economies cop it. And it applies even if some of these economies, like Turkey (whose President, Recep Tayyip Erdogan, has had it coming to him, after he’s allowed blatant politicking to compete with sound economics) don’t really deserve to be smashed,

Fears about Turkey and a possible contagion effect fell on Friday on Wall Street but the issue is still something that could turn ugly, if mismanaged by the key political players in this drama.

What I liked

- Average weekly ordinary time earnings (AWOTE) rose by 2.4% in the year to May, unchanged from the annual growth rate in November. But the AWOTE for full-time adults lifted by 0.3% to an annual growth rate of 2.7% – the strongest growth rate in over three years.

- Employment fell by 3,900 in July, after an upwardly-revised increase of 58,200 (previously reported as 50,900) in June. Full-time jobs rose by 19,300, but part-time jobs fell by 23,200. Economists had tipped an increase in total jobs of around 15,000. I never trust one month’s data so let’s call it an average 31,000 gain in jobs for two months in a row!

- The unemployment rate fell to 5.3% in July, down from 5.4% in June. But at 5.32%, it’s the lowest unemployment rate in 5½ years.

- The wage price index rose by 0.6% in the June quarter, after a 0.5% rise in the March quarter. Annual wage growth lifted from 2% to 2.1% – it’s small but it’s in the right direction.

- The Westpac/Melbourne Institute survey of consumer sentiment index fell from 4½-year highs in August. After rising by 3.9% to 106.1 in July, the index fell 2.3% to 103.6 in August. However, the index is above its long-term average of 101.4. A reading above 100 denotes optimism.

- The NAB business confidence index rose from 20-month lows of +5.6 points in June to +6.6 points in July. The long-term average is +6 points.

- The NAB business conditions index eased from a downwardly-revised +14.1 points (previously +15 points) in June to +12.4 points in July. The long-term average is +5.7 points.

- The 12-month moving average of the NAB employment index rose to a record high +9.58 points in July, up from +9.3 points in June. The long-term average is +1.7 points.

- The average credit card balance rose by $21.30 to a 5-year high of $3,272.70 in June. Balances were up by 4.6% over the year – the strongest annual growth rate in almost eight years. In smoothed terms (12 month average), the average balance was up by 1.3% – the strongest annual growth rate in 6½ years.

- Trump’s team is set to meet Chinese officials later in the month to try to sort out trade issues.

- US retail sales rose by 0.5% (survey forecast was +0.1%) in July.

- The New York Fed Manufacturing Index rose by 3pts to 25.6pts (survey: 20pts) in August.

- The NFIB business optimism index in the US rose from 107.2 to 107.9 in July (forecast 106.9).

- Chinese house prices rose by 1.2% in July to be up 5.8% on the year – the highest annual rate since September 2017.

What I didn’t like

- The participation rate fell from 65.7% to 65.5% but it’s only a one month slip.

- Overall, Chinese economic data was worse than expected and it looks like the trade issues are hurting China’s economic performance, at the moment.

- Turkey contagion fears after its lira was trashed by forex markets.

- Turkey announced retaliatory tariffs on US imports, imposing an additional 50% tax on rice, 140% tax on spirits and 120% tax on cars.

- Chinese technology giant Tencent’s shares fell by 6.7%, after reporting its first profit decline in almost 13 years. Shares of industrials’ Boeing and Caterpillar both declined by 2.2% on tariff concerns.

Another like worth noting

The US company earnings have been great (up over 20%) and I liked Walmart’s effort on Thursday that helped US stocks spike significantly. The company’s share price was up 9.3% on Thursday but, more importantly, it not only shows that bricks and mortar businesses can compete with Amazon, if they get their online offering right, it’s a nice pointer for the strength of the US economy. But the world is changing, with Walmart reporting that online sales over the quarter were up 40%!

That said, Walmart shares are up more than 20% over the year, while, Amazon’s stock has climbed more than 90% over the period. Amazon’s market cap is now near $920 billion, while the one-time biggest retailer in the world, Walmart, is valued at $291 billion! Gee, Robert E. Kahn and Vint Cerf, who invented the Internet, and Tim Berners-Lee, who brought the World Wide Web to life, really have a lot of explaining to do to anyone who doesn’t like the brave new world of online sales and a world whose eyes are glued to smartphones nearly 24/7!

The Week in Review:

- It’s a big international universe out there, and while we all know we should have global exposure, maybe it’s best to leave it to the pros. Here’s a huge investing lesson you should never ignore from yours truly.

- If you’re a long-term investor, and not a short-term speculator, Paul Rickard believes you should consider Transurban – a stock for patient investors.

- James Dunn delivered 8 reporting stocks to watch in his first earnings analysis, including Cochlear, CSL and Wesfarmers. And in part two, he focused specifically on Fortescue and Woolworths.

- Plus, on a role this week, James Dunn shared a piece about a global high-growth fund with strong international exposure for investors you should take a look at.

- Continuing with this week’s global theme, Tony Featherstone offered up 3 ETFs with access to global megatrends.

- Its share price may have dived but its global JV partner hasn’t lost faith. According to Charlie Aitken, Kidman Resources (KDR) still has the same story, but at half the price.

- Our Hot Stocks of the week included Perpetual, which has been caught up in the ‘anti-active funds management’ downdraft.

- Our first Buy, Hold, Sell – what the brokers say, delivered more downgrades than upgrades, with Tabcorp one of the lucky few to get an upgrade. And in our second edition, there was a double upgrade for REA Group and a triple downgrade for GPT Group.

- In our Question of the Week, we answer a weary reader’s query about weathering the GFC 10 years on.

- Finally, our Stock of the Week was a software company that ticks all the right boxes, by Australian Ethical Investment. Find out which one!

What moved the market?

- Turkish President Tayyip Erdogan doubled tariffs on some US imports, including alcohol, cars and tobacco, increasing trade tensions.

- China and the US have said they’ll renew negotiations in an attempt to diffuse the escalating trade war. They’re timed to meet just before America’s $US16 billion worth of tariffs on Chinese goods — and Beijing’s retaliatory tariffs— take effect.

- This week saw a positive tone to earnings season with big reports from CSL, Wesfarmers, Treasury Wine Estates and QBE amongst others.

- Australia’s June quarter wage price index (WPI) was in line with market expectations. Data from the Australian Bureau of Statistics (ABS) showed hourly wage growth excluding bonuses rose by 0.6% in Q2, as forecast.

Calls of the week:

- A Melbourne man in his 20s made the call to buy a Powerball ticket online just before the draw closed Thursday night, scoring himself a $50 million prize, together with one other equally lucky winner.

- Paul Rickard suggested Transurban as a good stock to buy for patient investors.

- Tony Featherstone named three ETFs that do well at tapping into global megatrends

The Week Ahead:

Australia

Monday August 20 — CommBank Business Sales Index (July)

Monday August 20 — Overseas arrivals & departures (June)

Tuesday August 21 — Reserve Bank Board minutes

Tuesday August 21 — Speech by Reserve Bank Governor

Wednesday August 22 — Construction work done (June quarter)

Wednesday August 22 — Skilled vacancies index (July)

Wednesday August 22 — Speech by Reserve Bank Deputy Governor

Overseas

Wednesday August 22 — US Existing home sales (July)

Wednesday August 22 — US Federal Reserve minutes

Thursday August 23 — US House price index (June)

Thursday August 23 — US New home sales (July)

Thursday August 23 — ‘Flash” purchasing manager surveys

Friday August 24 — US Durable goods orders (July)

Food for thought:

“Happiness lies in the joy of achievement and the thrill of creative effort..”

Franklin D. Roosevelt

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week: Top 5 most clicked:

Top 5 most clicked:

- A huge investing lesson you should never ignore – Peter Switzer

- Kidman Resources (KDR): same story, at half the price – Charlie Aitken

- 8 reporting season stocks to watch this week – James Dunn

- Transurban – a stock for patient investors – Paul Rickard

- Buy, Hold, Sell – what the brokers say – Rudi Filapek-Vandyck

Recent Switzer Reports:

- Monday 13 August: Leave it to the pros

- Thursday 16 August: Broader horizons

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.