Trump concerns eased overnight, with European markets well into the green, while Wall Street went strongly positive, considering the political consternation that still prevails, albeit at a lower level.

The FTSE was up 1.26% (or 268 points), the French CAC was 0.66% higher and the German DAX was up 0.39%. And with markets up around 0.6%, I can’t see why our market won’t get more positive on Monday.

Over the week, the S&P/ASX 200 index lost 1.9% and, given commodity prices were up a bit and the unemployment news was positive, you have to put most of this sell off down to the bank levy and Mr Trump. Who said politics isn’t important to stocks?

(In all of the Trump and bank stuff, you might have missed the fact that BHP rose 2.5% over the week, Rio Tinto spiked 5% and good old volatile Fortescue surged 10.6%! This is a great dip buying stock nowadays but it worries me too much to play.)

So this month has seen our market optimism and unwillingness to sell off to create the overdue pullback in stocks trumped and thumped. This week in particular has given validity to my “sell in May” prediction of April. We are down 3.8% for the month. Of course, I was never fully committed to the proposition but there had been a notable build up of negatives, on top of a “red hot” market in the USA, which looked ready for something negative, if the US President made one false move.

Well, he’s made more than one. And while the market could stand him playing tough guy in Syria and with that clown in North Korea, his sacking of the FBI boss and the possibility of him giving away state secrets to the Russians has really worried Wall Street.

To put it cutely, Trump has trumped our Trumpomania. Provided however that it doesn’t get even crazier and impeachment proceedings result, we could be looking at a buying opportunity!

Wednesday brought the worst day for the New York Stock Exchange for 2017, with the Dow dropping 372 points. Thursday saw some positivity but it was tentative.

This observation on CNBC by Randy Warren, the chief investment officer at Warren Financial, was spot on. “What happened yesterday [Wednesday, US time] was interesting. You had a complete removal of any Trump premium,” he said “What’s happening now is the fundamentals are taking over.”

And thankfully, the fundamentals will save us, if Trump gets booted (which I don’t expect), with the combination of improving economic readings worldwide adding to better earnings numbers.

A Trump dumping would hurt markets but, eventually, Vice President Pence, running with the same tax reform, deregulation and infrastructure policies, might even be seen as a safer pair of hands for the Congress to play ball with.

That said, the unconventional, un-presidential Trump actions have added to volatility and we can only play with what’s in front of us.

Supporting my point was CLSA strategist Christopher Wood, who observed “One point is stunningly self-evident – the latest developments have not encouraged hopes of a speedy implementation of tax reform”.

That’s the worrying bit for markets but the bright side was put by a GaveKal analyst, who looked at Pence as Trump’s possible replacement, arguing that “markets may quickly focus on ‘Trump without the bad stuff'”.

What I liked

- Employment rose by 37,400 in April, after rising by 60,000 in March (previously reported as a rise of 60,900 jobs). Full-time jobs fell by 11,600, while part-time jobs rose by 49,000. Economists had tipped a 5,000 increase in jobs.

- Unemployment fell from 5.9% to 5.7%, with the participation rate steady at 64.8%.

- Total new lending commitments (housing, personal, commercial and lease finance) rose by 7.7% to a 4-month high of $72.9 billion in March. Loans to buy used cars hit record (30-year) highs in March!

- The NAHB housing market index in the USA rose by 2 points to 70 in May. The reading was the second highest in 12 years and confirmed that single family home builders remain very optimistic.

- US industrial production rose by 1% in April – the biggest increase in three years.

- Fairfax was up 16.4% for the week, which has to be great news for long-suffering supporters of the stock. The arrival of a second bidder for the company was manna from heaven.

- Oil was at $US52.90 a barrel on Friday afternoon, which means two weeks of gains for ‘Texas tea’.

What I didn’t like

- The bank levy’s impact on banks, with the NAB closing down 6% for the week, while Westpac was down 5.3%, ANZ off 2.5% and CBA down 1.7%.

- The call of Damien Boey from CLSA, who thinks we’ll see a couple of rate cuts this year! Gotta hope this doomsday merchant has a faulty computer model or some crazy assumptions!

- The wage price index rose by 0.5% in the March quarter, to be up 1.9% over the year. Annual underlying inflation remains below wages at 1.7%.

- The Westpac/Melbourne Institute survey of consumer sentiment fell by 1.1% in May to 98. The confidence index is down 5% on a year ago. The index of whether it was a good time to buy a home fell to 7-year lows.

- This out of Europe: “European stock markets recorded their worst daily declines since September on political concerns in the US. Reuters noted “reports that US President Donald Trump had asked then-FBI Director James Comey to end a probe into his former national security adviser have raised questions over whether obstruction of justice charges could be laid against the President.”” (CommSec)

- A slump in the Brazilian stock market on corruption concerns involving the country’s President.

- Chinese economic data – retail, industrial production and urban investment – was OK but a little softer than expected.

- US housing starts fell by 2.6% in April to a seasonally adjusted annual rate of 1.17 million units – the lowest level in five months.

The trumping of Trump

I know Trump is unusual but markets don’t need the instability of an impeachment and a long drawn out period of political speculation, which creates divisions in the Republican Party. A strong, supported US President getting his economic agenda across the line is the best outcome for stocks. With US economic and earnings data all looking supportive of higher stock prices, you have to hope Trump can trump his natural, reactive self and his enemies.

Anyone heavily invested in stocks can’t be hoping for the impeaching of a US President or the political fallout of the whole drama that goes before it.

The week in review:

- Are ETFs a risky investment option? What about compared with managed funds? I explained what you need to know.

- Bank shares sold off following the Treasurer’s announcement of a bank levy at last week’s Budget. In this week’s Switzer Super Report, Paul Rickard ranked the Big Four in order.

- What’s ahead in the float pipeline? James Dunn revealed five non-resources opportunities to watch.

- The brokers upgraded Aveo Group, while BT Investment Management and Healthscope were downgraded.

- Charlie Aitken is concerned about the outlook for Australia’s economy and for the bricks and mortar retailers, which is one of Australia’s biggest employers. Find out more.

- With more tourists visiting Australia, Tony Featherstone shared three inbound tourism-related stocks with a mix of yield and capital growth.

- Telstra’s share price has dropped and the market has priced in a cut to its dividend, so is it time for another look at Telstra? Sean Fenton explained why he sees value in the company.

- In our second broker report, Fairfax was upgraded this week while AGL and Origin Energy were in the not-so-good books.

- And with the end of the financial year just around the corner, there are a number of things to consider before the super changes come into effect on July 1. Graeme Colley revealed the super reforms checklist.

Top stocks – how they fared

What moved the market?

- ‘The Donald’ trumped the market this week with political uncertainty around his Presidency weighing on global markets.

- The Aussie dollar bounced on a better-than-expected employment report for April, and US dollar weakness.

- Safe-haven trading helped buoy gold prices.

Calls of the week

- Not one, but two US private equity firms launched a takeover bid for Fairfax Media this week.

- S&P affirmed Australia’s AAA credit rating, but they’ve still got us on “negative watch”.

- Wesfarmers decided not to spin off its Officeworks business through an IPO.

- And shareholder activist Elliott Funds sent a new letter to the BHP board, calling for a divestment of BHP’s onshore US petroleum assets. For more, read Paul Rickard’s article, Fixing BHP.

The week ahead

Australia

- Monday May 22 – Business sales index (April)

- Tuesday May 23 – Speech by Reserve Bank official

- Wednesday May 24 – Construction work done (March quarter)

- Thursday May 25 – Detailed job market data (April)

- Thursday May 25 – Speech by Reserve Bank officials

- Friday May 26 – Australian Industry 2015/16

Overseas

- Tuesday May 23 – US New home sales (April)

- Wednesday May 24 – US Federal Reserve minutes

- Wednesday May 24 – US FHFA housing prices (March)

- Wednesday May 24 – US Existing home sales (April)

- Friday May 26 – US Durable goods orders (April)

- Friday May 26 – US Economic growth (March quarter)

- Friday May 26 – US Consumer sentiment (May)

Food for thought

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

Warren Buffett

Last week’s TV roundup

- For the first time, US global fund manager WCM will be available to retail investors looking for overseas exposure, via a new listed investment company called Contango Global Growth. To discuss, the co-CEO of WCM Investment Management, Paul Black, joins Super TV. Click here for more information.

- To discuss the details and reaction to the Budget, Switzer Super Report’s Paul Rickard and Sky News’ Paul Murray join the show.

- There’s a debate going on about the value of active fund managers versus passive exchange traded funds (ETFs). To discuss this issue and more, Gary Stone of Share Wealth Systems joins Super TV.

- Super Retail Group’s Peter Birtles discusses the changing retail environment and the outlook for the industry.

- And is Donald Trump the only reason our market is drifting lower? For a look at the market and the companies he’s watching right now, FNArena’s Rudi Filapek-Vandyck joins Super TV.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week one of the biggest movers was Vocus Group, with its short position increasing by 2.95 percentage points to 15.90%. Quintis went the other way, with its short position decreasing from 11.45% last week, to 8.73%.

Source: ASIC

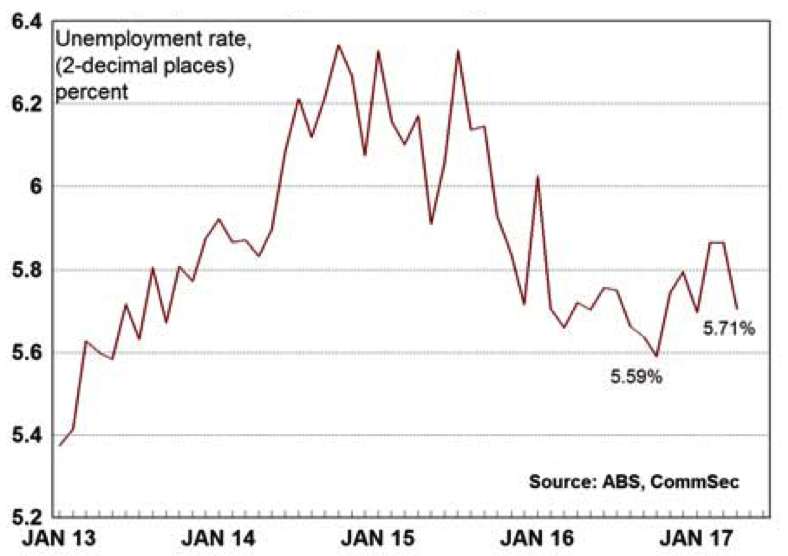

Chart of the week

Unemployment drops to near-4 year lows!

Source: CommSec, ABS

37,400 jobs turned up in April according to a survey by the ABS. That follows a lift of 60,000 in March. Encouragingly, the unemployment rate fell to 5.7% from 5.9% in March – the lowest level in nearly four years.

Top five most clicked stories

- Paul Rickard: Which bank?

- Charlie Aitken: Has the ASX 200 peaked?

- Peter Switzer: Are ETFs really a Big Short problem?

- Tony Featherstone: Tourism boom: 3 stocks to watch

- James Dunn: 5 floats to watch

Recent Switzer Super Reports

- Thursday, 18 May: Economic outlook

- Monday, 15 May: The Big Four banks

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.