Let me tell you a few facts. For some unknown reason bears always sound much smarter than bulls. Secondly, there’s a genuine business in scaring the pants off uninformed investors. I call it “scare broking”.

This week an Australian fund manager decided to liquidate his entire Australian equities portfolio and return capital to his investors. Fair enough, he’s worried about the future and thinks it’s the right thing to do. I am not criticising his decision.

However, the media coverage this generated was completely nonsensical relative to the size or influence of the fund. Quite frankly, had anyone heard of the fund in question before this week? I hadn’t.

The media coverage was akin to Warren Buffett liquidating his portfolio! It was ridiculous, but these are the headline grabbing days we operate in. “Bad news” gets clicks.

Clearly there are a variety of reasons to be concerned about the outlook for the Australian economy and the Australian equity market. However, I absolutely DO NOT believe we are at the “sell everything” point, I strongly believe that the ASX200 is morphing into a great LONG/SHORT market where the best returns from here will be generated by funds like my own who can buy the best companies in Australia and short the weakest.

The ASX200 performance in May, and particularly the ASX Twenty Leaders index performance this month (which broadly replicates what the average SMSF holds) again reminds you of the DANGERS of index investing. I am absolutely resolute in my view that buying a passive index product now is the most certain way to generate poor performance. May was a classic example of that in leading Australian equities.

The opportunities for high conviction stock pickers, both long and short, are increasing and I know this for a fact as that is what my investment team and I do all day.

While the ASX200 fell -3.4% in May and ASX Twenty leaders fell -5.8% (4.8% after dividends), the AIM Global High Conviction Fund gained over +3.00%. Since we started the fund in July 2015 we have beaten the ASX200 by +15%. It is flat and we are up +15%.

Our strong return in May, versus a significantly weak Australian index, really came down to high conviction longs such as Aristocrat (ALL), Treasury Wine Estates (TWE) and HUB 24 (HUB) rallying strongly, and high conviction shorts such as Ramsay Healthcare (RHC), Wesfarmers (WES) and Scentre Group (SCG) falling. We made money on our longs and shorts which confirms to me that the long/short strategy is the right one for approaching Australia. The rising index tide is no longer lifting all ships. In fact the index tide went out last month and thankfully our longs rose despite the falling index tide.

It is a market of stocks, not a stock market. Never forget that when someone tries to convince you to invest in a low cost index product or tries to convince you to “sell everything”. To me, active stock-picking has never been more alive and the opportunities for active stock-pickers never greater. Passive bubble = active opportunities, it’s as simple as that.

In Australia there are stocks and sectors we are attracted to and invested in. There are also stocks and sectors we aren’t attracted to and are short. This makes perfect sense as the Australian economy undergoes another new phase post the mining boom.

The new Australian economic phase is a derivative of TOO MUCH DEBT. The Federal Government has too much debt and the household sector has too much debt. This makes me bearish on anything consumer facing in Australia. We are entering a medium-term consumer downturn as households pay their record mortgage debt pile and do nothing much else. Households are in a nasty cash flow squeeze that won’t end anytime soon as I have written in these notes repeatedly.

The second aspect of the new Australian economy is “regulatory risk”. Overly-indebted governments, led by economic amateurs, go on revenue grabs. The bank tax is a classic example and you can expect further negative regulatory risk in Australian sectors in the months ahead. I am particularly worries about the private health sector, both private hospitals and private insurers. We are short Ramsay on this view as you know and would steer clear of the domestic healthcare sector.

The problem the Australian private healthcare stocks have is, just like the banks, there are too profitable! Can you believe I am writing that! I almost can’t but when I see a Liberal government target banks of all things, in a populist move, I say be very careful in any company that relies on government subsidies yet generates huge profits from a high ROE.

The two sectors I am really concerned about in Australia are the retail and healthcare sectors. Together they employ more Australian’s than all other sectors combined.

However, just like in the GFC I believe Australian’s will service their mortgages under all circumstances (unless they lose their job). On that basis I am NOT SHORT the big 4 Australian banks and think there probably will be a contrarian buying opportunity present itself in the next few months. I also think the BIG 4 will pass on the majority of the bank tax to borrowers, further squeezing household cash flows, yet pretty much ensuring bank dividends remain stable.

With resources, another big part of the ASX200, I just put that in the “too hard” category. I can’t predict commodity prices so my fund rarely does anything in Australian resource stocks. If I owned any Australian resource stock it would be BHP.

So what do we like in Australia?? What is going well??

My fund makes large investments in our highest quality structural growth stocks. Our two largest investments in Australia remain Aristocrat (ALL) and Treasury Wine Estates (TWE). Hopefully readers of these notes have followed my positive views on both these great global companies that just happen to be listed in Australia.

As times get broadly tougher in Australia, with the majority of the ASX200 facing headwinds not tailwinds, I believe the price paid (in PE terms) for those few stocks that can demonstrate structural growth will rise absolutely and relatively. I think ALL and TWE will be further re-rated.

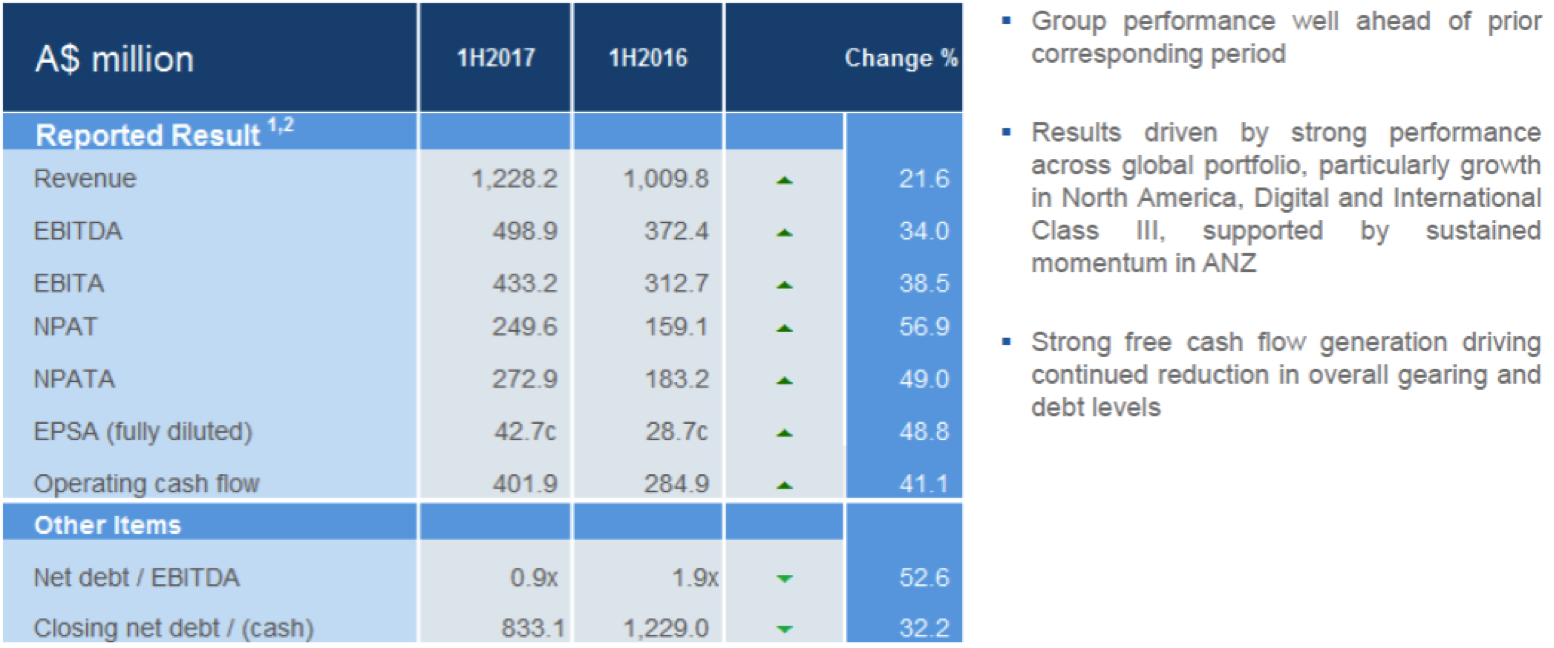

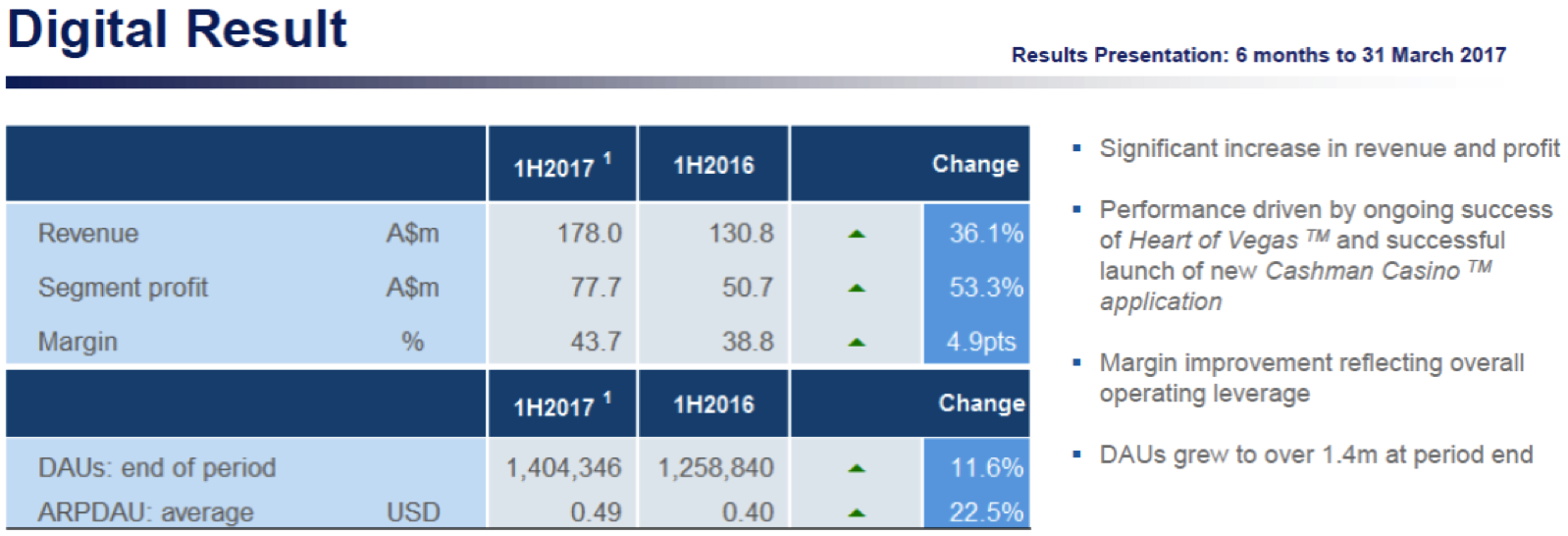

Today I thought we should run through the excellent Aristocrat (ALL) 1H FY17 numbers and why we remain very high conviction in this stock. I’ll start with some key slides from the ALL results presentation.

Everything in the 1H result was strong. Particularly pleasing was the cash flow conversion.

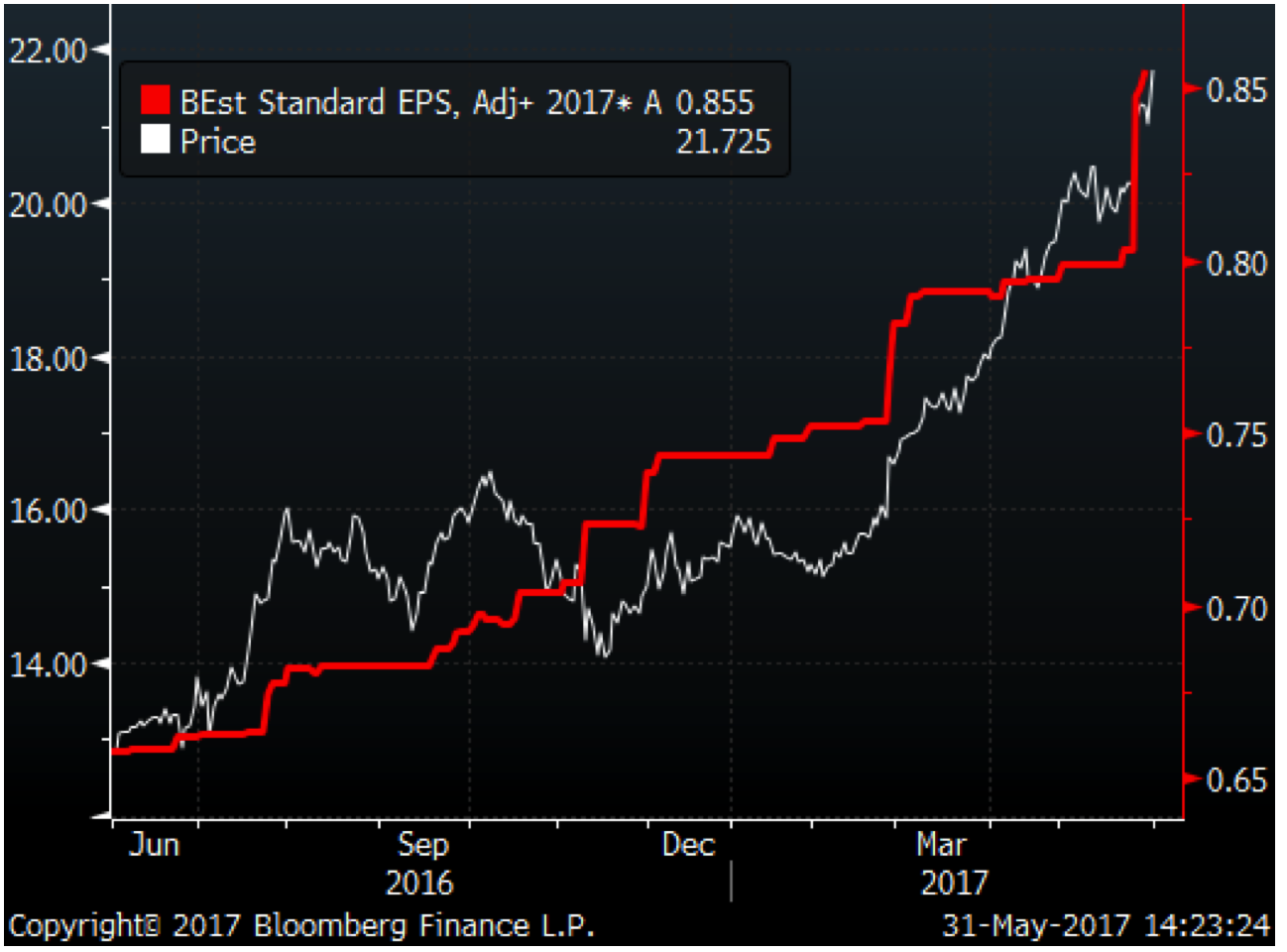

The result was stronger than analyst expectations and led to around +7% upgrades to FY17 estimates as evidenced in the chart below.

While ALL is up over +100% in the last 12 months, the most interesting aspect to me is the P/E has hardly moved.

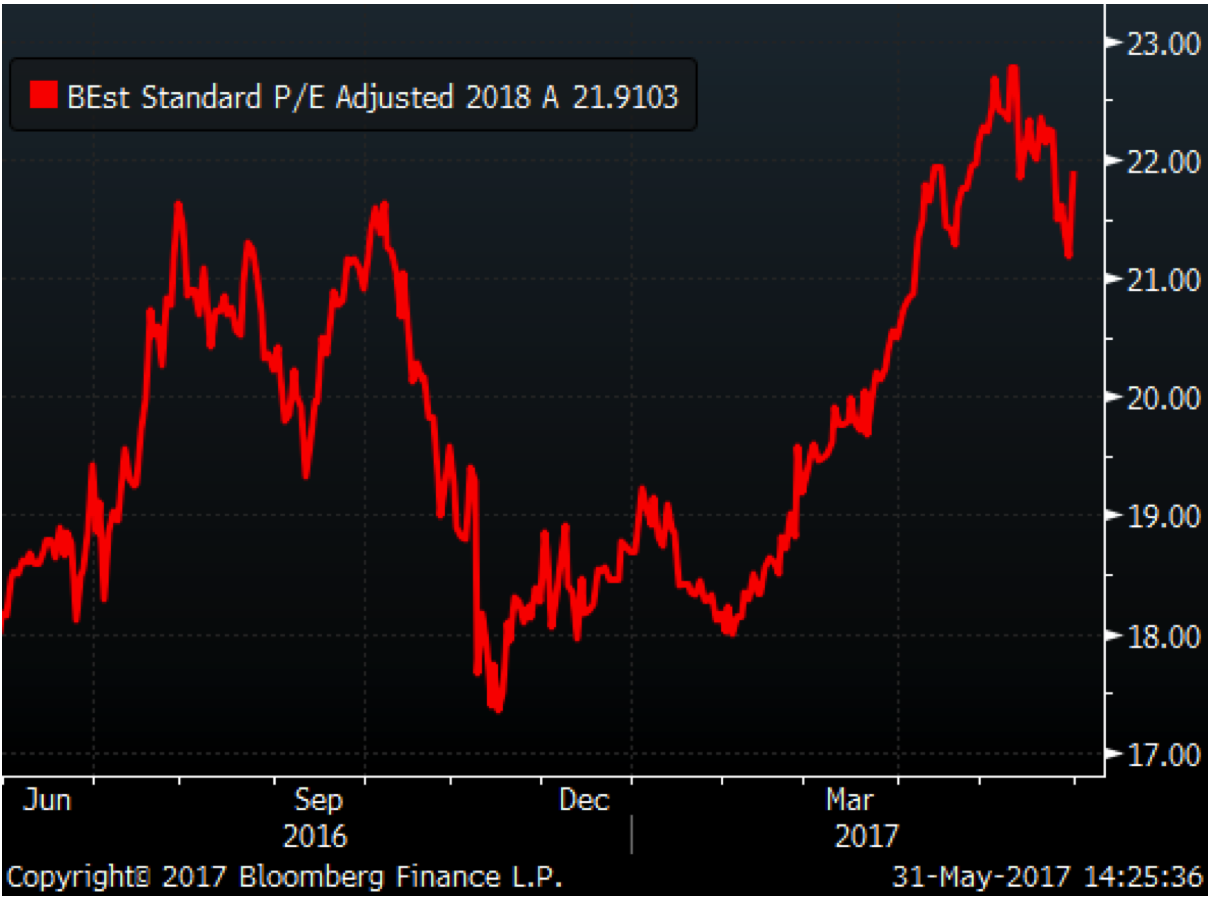

The 2018 P/E really hasn’t moved.

This is what changes next for ALL, the P/E expands.

The current 2018 consensus forecast is $1.00. I think that will prove light on by the time we get to the end of 2018, but for the sake of the exercise let’s use the current consensus forecast for ALL.

ALL is effectively a global technology stock. There’s no reason ALL couldn’t trade on 25x forward earnings which would equate to a $25.00 price target in 18 months’ time.

I think ALL will continue to $25.00 and beyond and it remains our largest Australian investment. It is a classic example of why ‘sell everything’ is not the right strategy.

While there is much to be concerned about in Australia and Australian equities, I remain of the view that active high conviction stock-picking will continue to generate superior absolute and relative returns.

I’ll be doing a webinar with Paul on Friday at 12.30pm to 1.30pm this Friday and I look forward to explaining more how I am positioned in Australia for what comes next.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.