Short sellers aim to profit from share price declines. Short selling is a very different proposition to going long. Not only is your upside capped, and downside unlimited – but you also have to pay a fee to borrow the stock. The easy answer can be to exclude shorting from your portfolio completely. However, we believe there are significant benefits to be gained from shorting, and that investors should consider allocating a part of their portfolio to shorting.

How can you access shorts in Australia?

When looking at managed funds, there are broadly two categories of funds that offer shorting. In our view, the most important decision that investors in these funds must make is the overall level of equity market exposure desired. The two categories are:

- Market exposed funds, otherwise known as long short funds. These funds have a positive exposure to the equity market. The direction of the equity market is the best indicator of returns – if the equity market falls in absolute terms, then it is likely that these funds will also fall. Common long short funds in Australia have 130% long equities, and 30% short equities – giving 100% equity market exposure.

- Market neutral funds are funds where exposure to the equity market has been minimised or eliminated. These funds, such as Firetrail Absolute Return, have short positions equal to their long positions, meaning the equity market exposure has been minimised. Returns are not dependent on whether the market is up 20%, or down 20%, but instead by whether the manager has chosen the right stocks to buy long, and the right stocks to sell short.

Whilst I have narrowed down the funds to these broad two categories – within the categories there are managers with different styles (value, growth, pairs trading etc).

The two golden rules

Shorting requires a different psychology when investing. Our experience in shorting has provided two key lessons that are applied when finding shorting opportunities.

1. Ignore valuation

Valuation can be a strong indicator signal to buy a stock as a long position. But it’s not so good on the short side! Stocks can remain expensive on valuation for long periods of time … and get even more expensive. Holding a short position in a stock that has a high valuation can be a dangerous investment proposition.

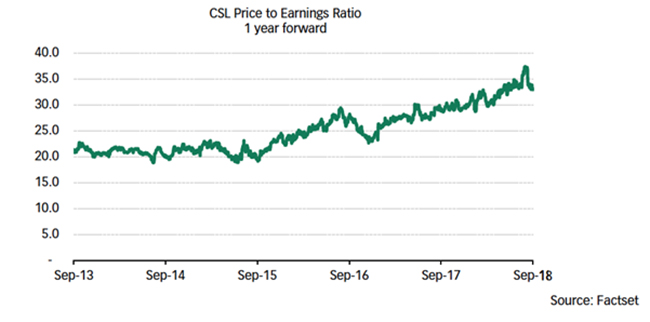

Take a look at the case of CSL over the past five years. It’s been a great performer – driven by not only earnings improvement, but also a significant increase in its valuation. This can be seen in the increase in the Price to Earnings Ratio from 20 times to approximately 35 times in the chart below:

Under these circumstances it could be argued that CSL is expensive, and we do not necessarily disagree with this. But in our view, it will likely remain at its current level until we see a catalyst occur. In the short term, share prices tend to follow earnings, and a catalyst to short the stock would be if our research suggested that they would not meet market expectations. Currently this isn’t the case for us – and CSL isn’t a short position.

2. Don’t hold on to shorts forever

“Time in the market, rather than timing the market” is not true for shorting!

Controlling your timeframe for shorting is critical – the longer you hold on to a short, the higher the risk that the share price will rise (and hurt your returns). We advocate holding shorts for a shorter period of time than you would hold most of your long positions. Be opportunistic in looking for the catalysts.

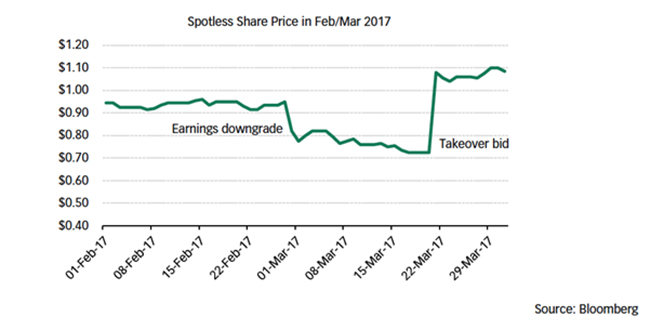

A great example of the importance of managing a timeframe is Spotless, which was the subject of a takeover offer from Downer in March 2017. Just three weeks earlier, Spotless had reported its first half 2017 financial results, which had resulted in brokers downgrading earnings forecasts by 20%. The share price fell 18% over two days, and over the next three weeks the short interest increased to 6% of the company. It was then that the takeover bid from Downer arrived – at a 60% premium to the price at the time. A painful day for the shorts!

Holding on to a short position after a catalyst has occurred, like the Spotless earnings downgrade, is the riskiest time to be short. Not only are company boards and management under immense pressure to improve earnings and the share price, but it is also a time where possible suitors could make a play for the company. Managing the timeframe for holding a short position is one way of minimising this risk.

Follow the rules

There is a different mindset required to short successfully. Not only can shorting be used to reduce levels of equity market exposure, but shorting can be a great contributor to returns in a portfolio when rules are followed.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.

Any opinions or forecasts reflect the judgment and assumptions of Firetrail and its representatives on the basis of information at the date of publication and may later change without notice. Any projections contained in this article are estimates only and may not be realised in the future. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. This communication is for general information only. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice relevant to their particular circumstances, needs and investment objectives. Past performance is not a reliable indicator of future performance.Interests in the Firetrail Absolute Return Fund (ARSN 624 135 879) and Firetrail Australian High Conviction Fund (ARSN 624 136 045) (‘Funds’) are issued by Pinnacle Fund Services Limited ABN 29 082 494 362 AFSL 238371. Pinnacle Fund Services Limited is not licensed to provide financial product advice. A copy of the most recent Product Disclosure Statement (‘PDS’) of the Funds can be located at www.firetrailinvest.com You should consider the current PDS in its entirety and consult your financial adviser before making an investment decision.

Pinnacle Fund Services Limited and Firetrail believe the information contained in this communication is reliable, however its accuracy, reliability or completeness is not guaranteed and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Firetrail and Pinnacle Fund Services Limited disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

Firetrail Investments Pty Limited ABN 98 622 377 913 (‘Firetrail’), Corporate Authorised Representative (No. 1261372) of Pinnacle Investment Management Limited ABN 66 109 659 109 AFSL 322140.