From 1 July 2017, a cap of $1.6m will be introduced on the amount you can transfer into the tax-free retirement phase. Anyone with a total retirement phase balance in excess of $1.6m will generally be required to either commute the excess amount back to accumulation phase or withdraw the excess from superannuation altogether. Further, transition to retirement (TTR) pensions will not be treated as retirement phase income streams from 1 July 2017.

To compensate for the taxation implications of transferring assets out of retirement phase in order to comply with the new rules, SMSFs will have access to Capital Gains Tax (CGT) relief on impacted assets. This CGT relief will allow trustees to elect to reset an asset’s cost base in 2016-17. This effectively locks in the capital gains tax treatment of the asset up to 30 June 2017. How this relief applies is different depending on whether the SMSF was using the segregated or proportionate method at 9 November 2016.

While beneficial for many funds, the decision to apply the CGT relief is not entirely straight-forward. We highlight two key strategies to consider before making any decisions on applying CGT relief.

1. Are you fully retired? If not, it might be better NOT applying the CGT relief

For SMSFs using the proportionate method as at 9 November 2016, the CGT relief provisions allow the trustee to elect for assets to lock in the 2016-17 financial years’ tax exempt percentage on unrealised capital gains or losses. While for many this will be advantageous there are certain situations where it may actually be better to retain the existing cost base. The main argument for not applying the CGT relief is where the fund’s tax exempt percentage (TEP) is expected to increase in the future. For example, this may occur when an accumulation member is expected to convert their balance to retirement phase prior to the sale of the asset.

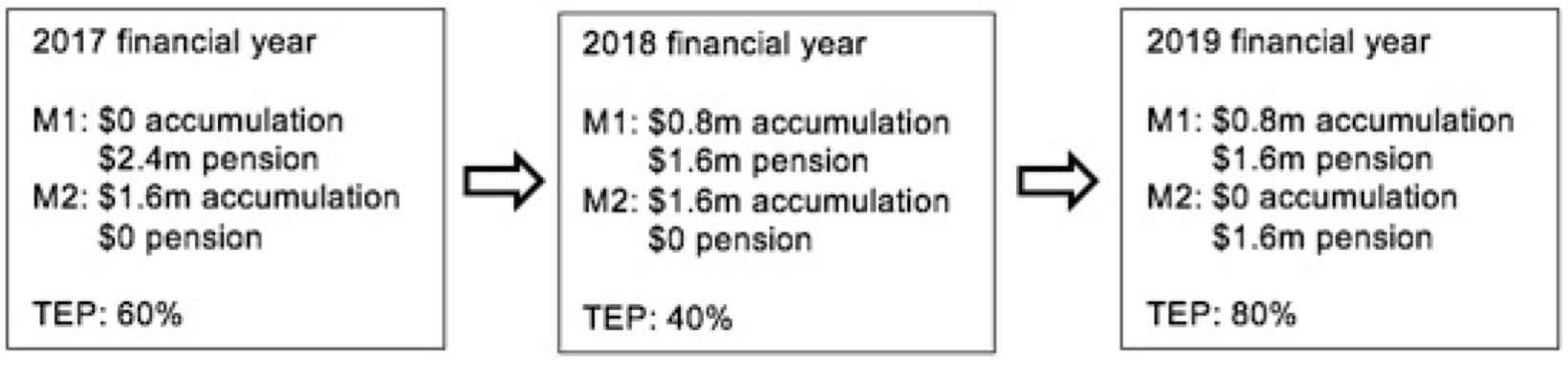

Let us consider a simplified example:

An SMSF has two members, M1 and M2, with four million dollars in assets in the 2017 financial year. M1 has an account based pension and M2 is still in accumulation. In 2017, the SMSF will only pay tax on (1 – 60%) = 40% of the net capital gain.

In 2018 the TEP reduces due to M1 commuting $800,000 to accumulation at 30 June 2017 to comply with the new transfer balance cap. It does look like resetting the cost base in 2017 would be a good idea as the trustee could lock in the 60% tax exemption on gains accrued so far compared to only 40% in 2018. However in the 2019 financial year the accumulation member expects to move into retirement phase leading to a higher TEP in 2019 compared to 2017. Assets sold in 2019 may be better off not applying the CGT relief so all gains will be realised using the higher TEP in 2019.

The decision on whether to apply the CGT relief depends on the timing of future capital gains tax events. Trustees should consider this decision on a per asset basis. Depending on when each asset is expected to be sold some may experience a better tax outcome choosing to reset their asset cost base at 30 June 2017 while for other assets it may be better to NOT apply the CGT relief.

2. Moving to the proportionate method may provide the best outcome for segregated assets

Assets which were segregated current pension assets at 9 November 2016 must use the segregated method to claim the CGT relief. An asset can apply the CGT relief if it ceases to be a segregated pension asset in order to comply with the new superannuation reforms. There are two options for how the relief is applied.

Option 1: Specific segregated pension assets are selected to be commuted to accumulation in order to reduce a retirement phase balance below $1.6m. The remaining pension assets continue to be segregated pension assets. In this case only those particular assets which are commuted and are no longer segregated pension assets are eligible to apply CGT relief. All remaining fund assets are not affected and will not be eligible.

Option 2: If the trustee does not wish to (or cannot) select specific assets to commute to accumulation they may choose to cease all segregated current pension assets and use the proportionate method in order to comply with the transfer balance cap. For example, if the trustee elected to treat all fund assets as unsegregated at 30 June and commute the required balance to accumulation on this date, then the fund could apply the CGT relief to all segregated current pension assets on 30 June when assets cease to be segregated. Gains or losses on segregated pension assets to which the CGT relief is applied would be disregarded.

Conclusion

The CGT relief provides a great opportunity for SMSFs to reset the cost base of fund assets and lock in capital gains which would currently be tax free or based on the current year TEP before making changes to comply with the transfer balance cap. However, while beneficial at first glance there are some scenarios which require further consideration.

Funds employing a segregation strategy may wish to move to the proportionate method to ensure all current pension assets can obtain the CGT relief and lock in current unrealised gains as tax free. For unsegregated SMSF assets, depending on the current TEP and expectation for future years it may be beneficial to not employ CGT relief.

Trustees should, prior to 1 July 2017, carefully consider the impact of applying the CGT relief on a per asset basis before decisions are made.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.