I continue to believe the correction in Australian small cap companies is providing some excellent stock specific opportunities in high-quality companies with solid fundamental potential. The AIM Global High Conviction Fund has added selected Australian small cap exposure at what we believe are now cheap entry prices.

Today I thought I’d introduce you to a stock that we have recently bought, IPH Limited (IPH.ASX), the $900m market cap Asia-Pacific leader in “intellectual property protection”.

Clearly listed legal firms haven’t had a stellar track record in Australia, however IPH has a completely different business model to its listed peers and is very conservatively run.

IPH, or “Intellectual Property Holdings”, is a holding company as such that wholly owns Spruson & Ferguson (established 1887), Pizzeys, Fisher Adams Kelly Callinans, Cullens & Practice Insight. IPH employs nearly 500 staff and provides specialist services spanning the protection, commercialisation, enforcement and management of most types of Intellectual Property (IP). Key practice areas include “Patents & Designs” (patent work being IPH’s major revenue contributor), “Trade Marks”, “Domain & Business Names”, and “Legal” (such as commercial legal advice/IP litigation).

For a larger version, click here.

{kind=link}

I was first introduced to IPH when I was a stockbroker at Bell Potter and working on the company’s IPO. I thought at the time it was an excellent business and I remain of that view. The company had a very successful IPO ($2.00) in November 2014, seeing heavy institutional support. The shares performed very strongly (high of $9.34) before coming back to earth ($4.44 today) in the last 12 months as institutional investors rotated to other sectors and shorters helped them along.

Interestingly, as the shares have come down so too have the FY17 P/E, to actually below the prospective FY17 P/E at the IPO. This is because since the IPO IPH has grown by acquisition and organically and FY17 consensus forecasts have risen through time. The stock is now commanding its lowest P/E since listing and in that I see opportunity.

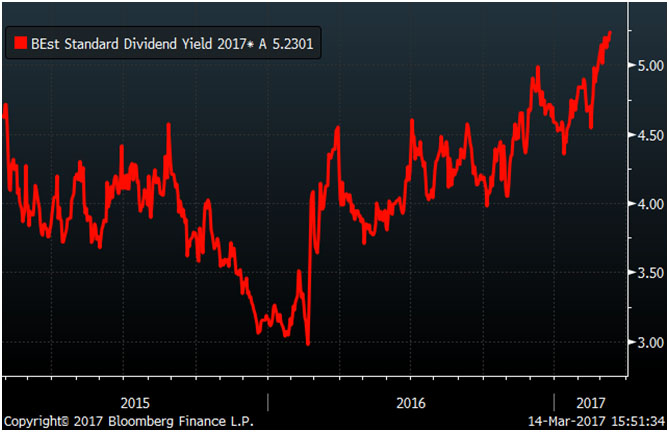

Conversely, the prospective FY17 dividend yield is now the highest since the IPO at 5.23%.

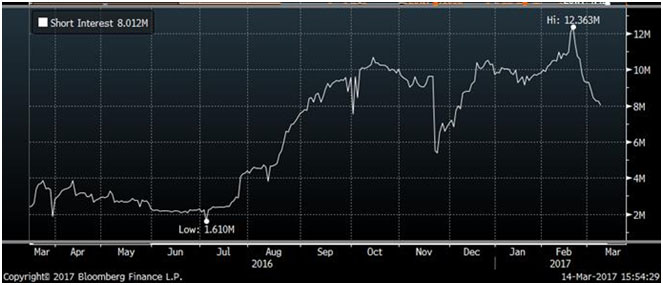

Interestingly short interest (SI) was rising in IPH over the last 12 months but peaked in February this year at 12.36m shares. Short interest has since fallen to 8m shares or 5.1% of the free float.

Other than short-covering hedge funds the other buyer of IPH shares has been Perpetual, the fund manager, who increased their holding by 2.6m shares to now own 13.04% of IPH.

Perpetual are a value based fund manager and I agree that IPH is now “value” on all investment metrics. It’s worth remembering also that IPH carries net cash of $32m on its balance sheet. Clear high debt levels killed other listed legal firms and this is the polar opposite of IPH who are un-geared despite the fact their forecastable business model could carry significantly higher debt levels.

One of the key attractions of IPH is it is a very predictable business with a wide spread of revenue streams by geography and client. The largest client is just 2% of group revenue.

For a larger version, click here.

{kind=link}

For a larger version, click here.

{kind=link}

In terms of recent results the FY17 IH result showed encouraging trends. Underlying EBITDA was $36.4m, roughly +5% ahead of consensus analyst forecasts. Against the previous corresponding period (PCP), EBITDA rose +13.3%. Obviously acquisitions and FX movements played the major role in PCP growth.

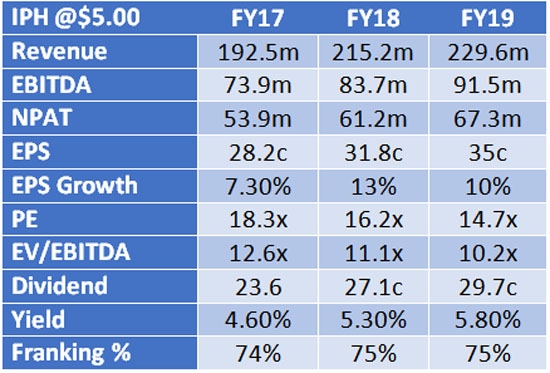

In terms of the investment arithmetic, the stock exceeds everything we look for now and into the forecast period.

One of the reasons for the pullback in IPH shares was a slow-down in growth in Asia during 2H FY16 and 1H FY17. Analysts believe this was primarily a function of cycling very strong comparatives that were boosted by the pull forward effect from the America Invests Act (AIA) on patent filings. Analysts now forecast Asia will return to solid organic growth of +9% in 2H FY17.

Other reasons cited for the P/E de-rating of IPH’s trading multiple include the release of escrowed shares and the delay in executing a strategic acquisition in Asia. However, with IPH’s free-float lifting from 59% to 82% post the November 2016 sell-down of escrow shares we believe the stock overhang issue has now been dealt with. In regards to the acquisition in Asia, while this is moving at a slow pace, we believe this reflects a thorough due diligence process that works for a better outcome for the group for the longer-term.

What has really happened is a combination of events have simply made this high-quality company cheap. We believe all the headwinds have eased and we expect to see the market start paying a higher multiple for the strong investment attributes IPH possesses.

The 10 reasons below are a succinct summary of the investment case for IPH.

For larger versions, click here and here.

{kind=link}

{kind=link}

In the last week there have been a series of positive sector notes and recommendation upgrades on IPH. We feel this is most likely a bottom in IP shares and the recovery has commenced.

We agree with analysts that a return to growth would see IPH shares trading around $7.00 in 12 to 18 months’ time, while paying a solid dividend yield along the way.

IPH is the debt free leader of the IP sector in Asia. We believe the shares are now cheap for the structural growth in the sector, IPH’s diverse long-lasting client base, high revenue visibility, minimal work-in progress (WIP), strong cash flow conversion, and high barriers to entry.

I encourage you to consider an investment in IPH at an appropriate size in portfolios to reflect this is a small cap company.

All in all, I am seeing more and more value in Australian small cap industrials and IPH is another example.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.