Stocks locally have been given a US-driven tailwind to reach new post-GFC heights this week but another week of Trump trade war anxiety could change all that. And if Friday’s US-Canadian negotiations are any guide, there could be fireworks next week!

More on that in a moment but local reporting season is done and dusted and the overall results were good, without being great, but that’s consistent with what our economy looks like – good but not great.

The company show-and-tell summary gets down to the following:

- 44% of results have surprised on the upside, which is in line with the long term norm.

- 77% were reporting higher profits than a year ago, which is the strongest since before the GFC and compares to a norm of 66%.

- 86% have increased their dividends or held them constant; and

- 62% of companies have seen their share price outperform the market on the day results were released.

This is how AMP Capital’s Shane Oliver viewed it: “2017-18 earnings growth have come in around expectations at about 8%, with resources earnings up 25%, thanks to solid commodity prices and rising volumes and the rest of the market seeing profit growth of around 5%. It’s not the 28% earnings growth being seen in the US but it’s still solid.”

And on the higher profits, he observed that “the breadth of profit increases was impressive” meaning the number of companies with rising earnings was historically significant. For a bigger picture of overall profits, this is Shane Oliver’s pictorial take on reporting season:

However, we have a long way to go to match the Yanks, with their 28% rise in collective company profits. And where the Dow and S&P 500 indexes had the best Augusts since 2014, they are further into their economic comeback than we are. In case you like milestones, the Nasdaq rose above 8,000 points for the first time, while the Dow Jones was back above 26,000 points, until Donald made some Canadian comments.

While on the US, stocks were buoyed by the Mexico trade deal announced early in the week and hopes were high that a Canadian inking on a deal would happen overnight. But a Bloomberg report of off-the record comments by President Trump didn’t help matters, where he allegedly said he was giving no ground to Canada on trade and that “it’s going to be so insulting, they’re not going to be able to make a deal!”

Later in the day, the Canadian negotiator said to reporters that “they were not there yet” and the market didn’t like it. The Canadians planned to do a press conference after the stock market closed at 4.30pm. It doesn’t sound market-positive but we’ll see.

This week has proven how important trade war talk has been for stocks. Next week will be driven by another “will he or won’t he” slam $US200 billion worth of tariffs on China on Thursday?

To the local stocks story and banks helped our market have a good week. The S&P/ASX 200 index rose 72.2 points (or 1.16%) this week, hitting the best level since December 2007 on Thursday of 6371.5 before closing on Friday at 6319.5.

Despite the bad publicity of Westpac raising home loan interest rates by 14 basis points to 5.38%, its share price sneaked up 3.2% over the week to $28.54, which shows us why CEO Brian Hartzer was prepared to draw fire on the subject. And while no other big four bank played follow the leader, they all went along for the stock price ride, with ANZ up 3.4% higher, NAB put on 3% and CBA rose 0.9%.

Bouquets have to go to Boral, who has turned its overseas foray into a winner, with underlying profit up 38% to $473 million. The company share price went up 8.2% for the week to end at $7.02.

Other big news stories were:

- “TPG Telecom announced a $15 billion merger, with Vodafone Hutchison Australia (VHA) on Thursday, lifting the company’s shares 10.7% to $8.56 this week. Hutchison Telecommunications, which owns 50% of VHA, also rose this week, up 28.6% to 13.5c.” (AFR)

- Bellamy’s actually delivered on its promise, with profit up, at $42.2 million after a near million loss last year! It looks like its Chinese problems are behind them but who knows with these guys? Anyway, good luck to them and the shareholders who have stuck solid.

- The big disappointment was Speedcast, with its lower profit and negative outlook putting them at odds with nearly every expert! Its share price slumped 36.6% for the week to $4.24!

What I liked

- The weekly ANZ-Roy Morgan consumer confidence rating rose by 2.1% to 116.5 above the average of 114.1 since 2014 and above the longer term average of 113 since 1990. The 2.1% increase in the index was the biggest lift in 11 weeks.

- In 2017/18, business investment rose by 3.1% to $117.99 billion. Non-mining investment rose by 8.8% to a record $82.8 billion – the fastest annual growth rate in 6½ years.

- Services sector investment hit a record high of $73.3 billion for the year to June.

- The third estimate of investment in 2018/19 is $101.997 billion and is 1.1% lower than the third estimate for 2017/18. The 16.1% lift in expectations for 2018/19 is the second biggest increase for a June quarter in seven years – above the decade average of 12.4%.

- The National Bureau of Statistics’ Manufacturing Purchasing Managers’ index in the US rose from 51.2 to 51.3 in August, above market forecasts for 51 points. The services gauge rose from 54 to 54.2, above consensus expectations for 53.8 points. Results above 50 points imply expanding activity.

- Annualised economic (GDP) growth for the US was revised up by 0.1% to 4.2% (survey: 4%) for the June quarter (second estimate).

- US personal income rose by 0.3% in July, with spending up 0.4% – both as expected. The core personal consumption deflator (the Federal Reserve’s preferred inflation measure) rose by 0.2% in July, to be up 2% on a year ago – both results as expected.

- Canadian PM Justin Trudeau said it was possible that a trade deal with the US and Mexico could be reached by Friday.

- US Treasury Secretary Steven Mnuchin said on Tuesday that he believed that the US could reach a trade deal with Canada this week, after an agreement with Mexico.

- The Conference Board Consumer Confidence Index rose by 5.5pts to 133.4pts (survey: 126.7pts) in August.

- The German IFO business conditions index rose strongly and growth in bank lending is continuing to trend higher.

- Just when it seemed Chinese growth is slowing, its PMIs surprisingly rose in August!

What I didn’t like

- Argentina’s central bank rate at 60% to stem the plunge in the peso and what all this means to emerging economies investments. Not good and its a worry when you throw in Turkey and its potential threat to European banks.

- Council approvals to build new homes fell by 5.2% in July, to be down 5.6% on the year.

- Private sector credit (effectively outstanding loans) rose by 0.4% in July after a 0.3% rise in June. Credit was up 4.4% over the year – the equal slowest growth rate in 4½ years. Investor housing finance fell 0.1% in July, with annual growth easing to a record low of 1.6%. Annual deposit growth at banks in July was the slowest in 26 years.

- New business investment (spending on buildings and equipment) fell by 2.5% in the June quarter to be up 0.4% over the year.

- Investors in the US took profits after four days of gains on reports that President Trump was preparing to apply tariffs on US$200 billion of Chinese goods.

Time to shop for an Amazon?

On August 6, I interviewed the CEO of MGM wireless (MWR) on my Money Talks program on Sky. He talked about his Spacetalk smartwatch, which means parents know where their young kids are 24/7. The share price has gone up over 100% since that interview! I thought about this company when I saw what Amazon has returned since going public. “If you had invested $1,000 during Amazon’s IPO in May 1997, your investment would be worth $1,341,000 as of August 31, according to CNBC calculations.”

The Week in Review:

- While it can be nerve-wracking when talk of a market dive escalates, I wrote that it’s important to look a little deeper.

- Paul Rickard said that Scott Morrison has a lot of work to do if he wants to win the next election, and it’s time to consider what you need to do if he doesn’t.

- It’s the final countdown for reporting season, and James Dunn highlighted 8 company announcements to pay attention to.

- Charlie Aitken suggested it’s time to forget FAANG and consider the Asian BATS – Baidu, Alibaba, Tencent and Samsung.

- 5 mid- and small-cap companies impressed Tony Featherstone this earnings season.

- In the first Buy, Hold, Sell – what the brokers say for the week, we saw downgrades outnumbering upgrades, with Afterpay Touch and Coca-Cola among the upgrades. In the second edition, downgrades continued to dominate.

- In Questions of the Week, we looked at Wesfarmers ahead of the Coles demerger, as well as G8 Education.

- Flight Centre, Wesfarmers and Nanosonics are our Hot Stocks for the week

Top Stocks – how they fared:

What moved the market?

- TPG Telecom and Vodafone Hutchison Australia announced plans for a $15 billion “merger of equals” to take on Telstra and Optus.

- The United States and Mexico agreed to enter into a new trade deal that President Donald Trump said would be beneficial to manufacturers and farmers from both countries.

- Reporting season has drawn to a close with better than expected results.

Calls of the week:

- Charlie Aitken said that emerging markets have bottomed and now is the time to invest in the Asian BATS: Baidu, Alibaba, Tencent and Samsung.

- Paul Rickard suggested some actions investors can take to prepare for the possibility of an ALP Government.

- The Switzer Listed Investment Conference, for bringing together some of Australia’s best money managers. We’re giving away complimentary tickets to all of our loyal subscribers. Click here to claim your tickets and enter the promo code SSR.

The Week Ahead:

Australia

Monday September 3 — CoreLogic home value index (August)

Monday September 3 — ANZ job advertisements (August)

Monday September 3 — Business indicators (June quarter)

Monday September 3 — Retail trade (July)

Monday September 3 — Manufacturing purchasing manager surveys (August)

Tuesday September 4 — Reserve Bank Board meeting

Tuesday September 4 — Balance of payments (June quarter)

Tuesday September 4 — Reserve Bank Governor speech

Tuesday September 4 — Government finance (June quarter)

Wednesday September 5 — Economic growth (June quarter)

Wednesday September 5 — New vehicle sales (August)

Thursday September 6 — International trade (July)

Friday September 7 — Housing finance (July)

Overseas

Monday September 3 — China Caixin manufacturing index (August)

Tuesday September 4 — US ISM manufacturing index (August)

Tuesday September 4 — US Construction spending (July)

Wednesday September 5 — China Caixin services index (August)

Wednesday September 5 — US Trade balance (July)

Thursday September 6 — US ADP employment (August)

Friday September 7 — US Non-farm payrolls (August)

Saturday September 8 — China International trade (August)

Food for thought:

“Every ball went exactly where I wanted it to go until the ball that got me out.”

Don Bradman

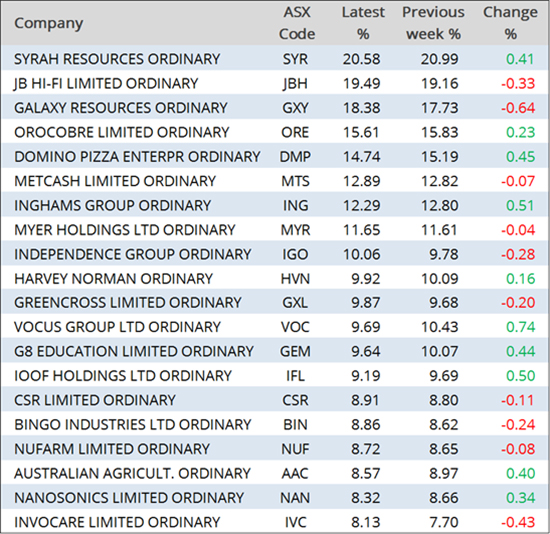

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week:

In celebration of Don Bradman’s birthday on Monday, here is a chart tracking The Don’s performance throughout his Test Match career:

Source: Wikimedia

Top 5 most clicked:

- Should you take action with crash talk increasing? I’m not! – Peter Switzer

- Preparing for Prime Minister Bill Shorten – Paul Rickard

- Emerging markets have bottomed – buy BATS – Charlie Aitken

- 5 fantastic stocks to follow after reporting – Tony Featherstone

- Hot stocks – the top 3 this week – Penny Pryor

Recent Switzer Reports:

- Monday 27 August: Crash trash talk

- Thursday 30 August: Batter up

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.