Back in June, I reviewed Australia’s leading conglomerate, Wesfarmers (WES), and concluded that “the run up to $48.01 isn’t supported by material changes to the business’s prospects. Multiples and dividends are less attractive. Lighten, and take some profits.”

Clearly, I got the timing a little wrong as Wesfarmers ran all the way up to $52.77, before easing back to Friday’s close of $49.84. Overall, it has marginally outperformed the market over this period – up by 3.8% compared to the market’s 1.6%.

Wesfarmers (WES) – 1 yr (Sept 17 to Sept 18)

Source: nabtrade.com.au

A different ending

But the story hasn’t changed as managing director Rob Scott continues to re-position the conglomerate. Since June, he has announced the sale of three further non-core/lower returning businesses:

- Wesfarmers 40% interest in the Bengalla JV thermal coal mine in the Hunter Valley for $860 million. This completes Wesfarmers exit from coal mining (the sale of the Curragh mine was finalised in March), and will result in a pre-tax profit of circa $670 million;

- The Kmart Tyre and Autoservice business for $350 million; and

- A 13.2% indirect interest in Quadrant Energy for US$170 million.

These changes to the portfolio follow Scott’s call to divest Homebase, the chain of UK home improvement stores Wesfarmers tried to “Bunningsise” and failed dismally, and of course, the Coles demerger. Following shareholder approval expected in November, the demerger will see Wesfarmers shareholders receive one new share in an ASX-listed Coles Limited for each ordinary share they own in Wesfarmers.

Wesfarmers proposes to retain a 15% interest in Coles and keep its 50% interest in Flybuys. While the latter makes sense strategically, given the importance of loyalty and online initiatives, it is not clear why Wesfarmers will retain a minority interest in Coles. It is a bit like having a foot in both camps.

New shareholders in Coles Limited will have the choice of keeping shares in a low growth supermarket business competing with aggressive competitors in Aldi, Kaufland and Costco (and of course Woolworths and Metcash), or flogging them.

Scott’s repositioning of Wesfarmers has been rewarded by the market, with the shares rising from a multi-year trading range of $37-$44 to around $50. It is a case of improving the return on capital employed and to some extent “the sum of the parts being greater than the whole”. None of the initiatives are about increasing revenue per se.

The existing Wesfarmers business is trading satisfactorily, rather than outstandingly. Bunnings remains the star, although will be challenged to maintain sales growth rates, particularly if the housing market slows, while Coles has regained some sales momentum over Woolworths. Kmart and Officeworks are doing well, Target remains a basket case, while the industrials and safety division plods along.

The point is that the share price rise is almost entirely due to the divestments and demerger, rather than any sustainable increase in earnings. While the net effect might be to increase the earnings per share, at around 18 times forecast FY19 and FY20 earnings, Wesfarmers is no standout.

What do the brokers say?

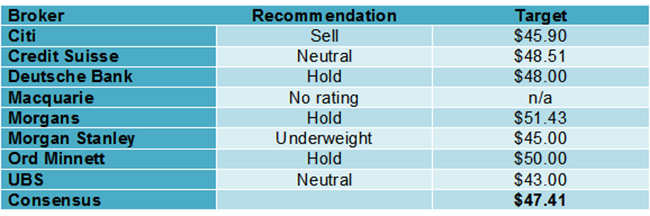

The brokers see Wesfarmers as being marginally overvalued. According to FN Arena, the consensus target price of $47.41 is some 4.9% below Friday’s close of $49.84. Of the major brokers, UBS is the most bearish, with a target of $43.00, while Morgans has the highest target price of $51.43. There are five neutral recommendations and two sell recommendations (no buy recommendations).

While acknowledging management’s zeal for capital discipline, the re-positioning of the portfolio and the possibility of a capital return, the brokers see limited opportunities for earnings per share growth. Execution risks remain around Target, and while Bunnings is a super business, the risk of a slowdown in the housing market could be a headwind.

On multiples, the brokers have Wesfarmers trading on a multiple of 18.2 times FY19 forecast earnings and 18.2 times FY20 forecast earnings. At a price of $49.84, the prospective dividend yield is 4.6% for FY19 and 4.7% for FY20.

Bottom line

Lighten and take some profits.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.