In this crazy market, where the big banks are seemingly friendless and growth stocks like CSL are pushed to trade on multiples of 34 times forecast FY19 earnings, the big consumer staples stocks, Wesfarmers and Woolworths have also been big winners. Wesfarmers, which has traded in an incredibly narrow range of $38.00 to $44.00 over the last five years, has broken out to hit a 10-year high. On Friday, it closed at $48.01.

Wesfarmers (WES) – 1 yr (June 17 to June 18)

Source: nabtrade.com.au

Wesfarmers (WES) – 10 yrs (June 08 to June 18)

Source: nabtrade.com.au

Is this breakout due to a fundamental improvement in Wesfarmers prospects? Or rather, is it just due to market momentum and stock/sector rotation and hence now presents as a selling opportunity? Here is my assessment.

What’s changed?

There have been three important changes at Wesfarmers under new managing director Rob Scott. Firstly, it has almost completed the divestment of Homebase, the chain of UK home improvement stores that it acquired in 2016, tried to “Bunningsise”, and failed dismally. Wesfarmers will record a loss on disposal of £200 million to £230 million in its full year accounts. It has already written off £531 million ($931 million) in its half-year accounts.

The good news for Wesfarmers shareholders is that the operating losses will cease. In the first half, Bunnings UK lost $165 million.

Secondly, it plans to demerge the Coles supermarket business next financial year. We have previously remarked in The Switzer Report that demergers in Australia have a pretty good track record. A re-energised and incentivised management team, set free from “head office” control and bureaucracy, with the right balance sheet, capital structure and focussed board is now able to exploit the business that it knows best. That’s the theory.

In the main, it has largely worked. Think of Orora and Amcor, Bluescope and BHP, South32 and BHP, CYBG and NAB, Pendal and Westpac, Dulux and Orica, Treasury Wine Estates and Fosters. For shareholders, there is often a period of underperformance for the first six or so months, as the overhang of spun-off stock finds a home before the stock steadies and starts to outperform.

But there have also been some demerger disasters. Arrium (formerly OneSteel) from BHP and Paperlinx from Amcor are two that come to mind. And of course, a demerger involves costs (stamp duty and transaction costs) that existing shareholders ultimately pay.

Coles and Wesfarmers is arguably a little different from other demergers. Whereas demergers often involve a sometimes forgotten/unloved/capital starved division being spun out (companies rarely get rid of the “crown jewels”), Wesfarmers, which is one of Australia’s few real conglomerates with divisions ranging from retailing through to industrial safety and mining, operates a very thin head office. Its divisions are highly autonomous and independent, with returns strictly measured against the capital employed. Coles is not a business that has been capital starved.

Possibly, it is a story of “the sum of the parts being greater than the whole”, but it is not the usual demerger story.

The third change is to reposition the portfolio and drive opportunities for growth. This involved the sale the Curragh coal mine for $700 million, capital expenditure being focussed on higher return businesses, and investments in improving store networks and online capabilities. The growth opportunities haven’t yet been revealed to the market, although Wesfarmers says that it plans to establish an advanced analytics centre and is strengthening its business development team.

What do the brokers say?

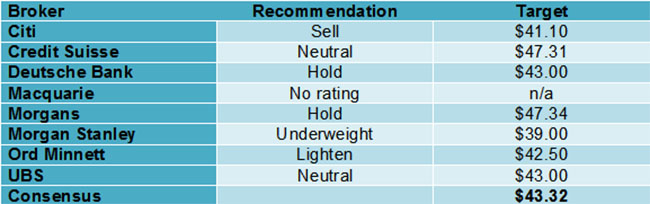

The brokers see Wesfarmers as being overvalued. The consensus target price of $43.32 is some 9.8% below Friday’s close. Of the major brokers, Morgan Stanley is the most bearish with a target of $39.00, while Morgans has the highest target price of $47.34. According to FN Arena, there are four neutral recommendations and three sell recommendations (no buy recommendations).

While acknowledging management’s new found zeal for capital discipline, the re-positioning of the portfolio and the possibility of a capital return, the brokers see limited opportunities for earnings per share growth. Execution risks remain around Target, and while Bunnings is a super business, the risk of a slowdown in the housing market could be a headwind.

On multiples, the brokers have Wesfarmers trading on a multiple of 21.0 times FY18 forecast earnings and 18.5 times FY19 earnings. At $48.01, the prospective dividend yield is 4.5% for FY18 and 4.7% for FY19.

Bottom line

The run up to $48.01 isn’t supported by material changes to the business’s prospects. Multiples and dividends are less attractive. Lighten, and take some profits.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.