I want to recap on how I started last week’s Q2 US earnings preview note:

Amazon, Netflix and Microsoft together this year are responsible for 71% of S&P 500 returns and for 78% of Nasdaq 100 returns. The three stocks make up 35%, 21% and 15% of S&P 500 returns, respectively, while making up 41%, 21% and 15% of Nasdaq 100 returns. Apple also makes up a large portion of both indexes, contributing 12% of both S&P 500 and Nasdaq 100 returns, while Alphabet and Facebook contributed 8% to each. In total for 2018, the six stocks make up 98% of S&P 500 and 105% of Nasdaq 100 gains.

Yes, you read that correctly, just six stocks: Amazon, Netflix, Microsoft, Apple, Alphabet (Google) and Facebook contributed 98% of the S&P500 gains this year and 105% of the Nasdaq 100 gains this year. I consider that a dangerously narrow rally particularly given that the valuation of Netflix, for example, is now ridiculous.

While Netflix (NFLX.US) shares seem to go up every day, and are now up 116% in 2018, the valuation is absurd in my opinion. It may well get more absurd, but paying a P/E of 288x trailing earnings or 145x 2018 earnings and a market capitalisation of US$180 billion doesn’t seem a sensible thing to do. The $180 billion market capitalisation for Netflix is the same as the Coca-Cola Company, higher than Walt Disney, double Caterpillar and closing in on Home Depot at $227 billion. It’s absurd, and a classic example of a stock and sector “peaking on euphoria” that will never deliver the earnings to justify the monster P/E.

Just remember, US equities in 2018 have been a “six stock show”. That is not healthy and when you overlay the flattest US 2-10yr yield curve in a decade (which signals recession ahead) there is cause for concern in US equities. That is why this earnings season is vital for US equities. The broader market needs to confirm and beat earnings expectations.

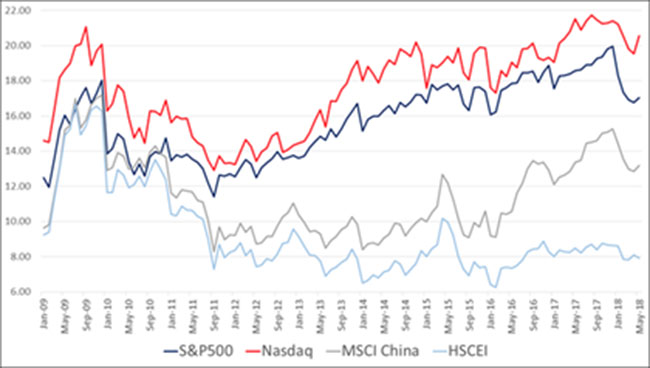

It’s worth remembering, that the growth (red line) versus value (blue line) relationship in equities is at its widest point since just before the bursting of the DOT.COM bubble in 1999. This chart is basically US tech versus everything else.

This is also important for the P/E premium US equities are commanding to the rest of the world (see chart below). If that is to hold, this US earnings and outlook season needs to deliver.

The numbers are in

Move forward to this week and Netflix saw an aggressive sell-off after reporting Q2 numbers well less than consensus estimates. Netflix reported domestic streaming total net adds of 674,000 (versus a consensus estimate of 1.21 million) and international net adds of 4.47 million (vs. consensus of 5.04 million). Total revenue came in at $3.91 billion, marginally lower than the consensus estimate of $3.94 billion. Guidance for Q3 was also considerably lower than street expectations. Netflix guided Q3 domestic streaming net adds of 651,000 (versus. consensus of 953,000) and international net adds of 4.35 million (versus consensus of 5.10 million). Netflix also acknowledged that they expect cash content spend to be back-half weighted and maintained full year cash burn guide of $3-$4 billion. It seems to us like an across the board miss on both Q2 and also Q3 guidance.

While the numbers still show good growth by any measure, when you’re priced on euphoric perfection you need to deliver better than “good”. Moreover, the consensus numbers highlight just how much is priced in and expected from Netflix.

More broadly, I think this Netflix reaction to weaker than forecast subscriber growth is trying to warn you about paying massive multiples for future earnings growth. This is particularly so when the growth versus value stock relationship hasn’t been this wide since the peak of the DOT.COM boom in 1999.

Clearly, parts of the global and local technology sectors are a complete bubble. Bubbles only become obvious when they burst.

Hot air

My advice is it is time to take profits in global and local technology stocks that are priced on “hot air” and have very little valuation or earnings support. If the momentum cycle changes many of these stocks could lose 50% of their value and still be expensive. Australian stocks I would put in that list include WiseTech Global (WTC), Appen (APX), and Afterpay Touch Group (APT) – three very high flyers.

Remember in the short-term the equity market is a “voting machine”, in the long-term it is a “weighing machine”. Eventually all stocks are priced off their profitability, the cash they generate, and what percentage of that profitability they return to shareholders (dividends, buybacks etc).

I would strongly suggest that many of the most popular momentum stocks right now, most of which are in the technology sector, will never be able to deliver on the huge expectations their current share prices are discounting. On that basis, if you are being paid for decades of future earnings right now, you should accept the markets current generosity and take profits.

There’s nothing wrong with taking profits in wildly expensive stocks. Netflix is telling you to do that, in my opinion, and you should be either rotating to value or cash. There’s nothing wrong with having a little more cash as volatility picks up.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.