Recent private equity sell downs have a patchy record. Nine Entertainment Company (NEC) has been a dog, while Healthscope (HSO) has done better than expected, although not quite as well on market as its main listed competitor, Ramsay Health Care (RHC). The latest sell down is the long awaited IPO of superfund administration and share registry provider Link Administration Holdings Limited (LNK), which is set to list on the ASX on October 27. A little like Healthscope, this is a stock that to invest in, you will need to get comfortable with the growth strategy – because the sellers aren’t doing investors any favours here.

The Link business

The Link business comprises three business units. Funds Administration, which provides back office services such as registry, benefit and contribution processing and member reporting to Australian super funds including Australian Super; Corporate Markets – which is the Link Market Services share registry business that shareholders of Commonwealth Bank and Telstra would be familiar with; and Information, Digital and Data (IDD) – which supports the other divisions with IT platforms and data analytics, and also licenses its IT to some external clients.

Following the acquisition of the Superpartners in December 2014 – a business that was owned by five of the largest industry super funds including Australian Super and Cbus – the funds administration business is forecast to generate 60.3% of Link’s revenue in FY 16. Corporate Markets contributes 18.5%, while IDD accounts for the balance of 21.2%. The Link Group has 4,300 employees and while operating in 11 countries, 95% of revenue is from Australia and New Zealand. Of its revenue, 91% is deemed to be recurring, although there is some client concentration risk with the largest five clients contributing 46% of revenue.

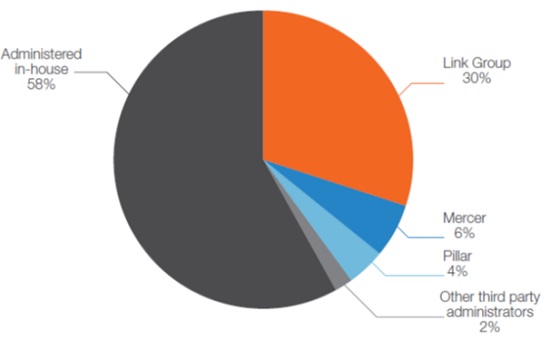

Link says that it has a 30% market share of a $2.0 billion revenue pool in superfund administration services, including clients such as Australian Super and REST. It notes the decline in individual superannuation accounts in Australia, from a peak of 33 million in 2010 to approximately 30 million in 2014, but sees opportunity in the 58% of “administered in-house” services that super funds may outsource in the future as they seek to concentrate on their core areas of expertise.

According to the chairman, Michael Carapiet, Link’s growth strategy “is focused on strengthening the company’s competitive advantage through innovation, executing the integration of Superpartners and the continuation of Link Group’s disciplined expansion and acquisition strategy by further expanding Link Group’s existing operations and pursuing opportunities adjacent to Link Group’s existing operations.”

Superannuation Administration Services by Provider

The sell-down

Existing shareholders Pacific Equity Partners, Intermediate Capital Group, Macquarie and management are offering 70.1 million shares for sale, and the Company is issuing 84.9 million* new shares, to raise approximately $913 million. At the conclusion of the offer, the existing shareholders will own 53.7% of the company.

New shareholders will pay between $5.41 and $6.37 per share for the balance of 42.3%, with the final price to be determined in an institutional book build. Based on these prices, the Company will have a market capitalisation of between $2.0 billion and $2.3 billion. The funds from the offer will be used to pay out existing equity holders and debt providers. New banking facilities will see the company’s debt position reduced to approximately $310 million. The existing shareholders have entered into a voluntary escrow arrangement with their shares – although this runs out in August 2016. In certain circumstances, the existing shareholders can also sell some shares as early as February 2016.

Pricing

On a proforma basis, Link is priced on a multiple of FY16 NPAT of between 25.3 times (at an offer price of $5.41) to 28.7 times at $6.37. Removing some significant items and adjusting for acquired amortisation costs, the multiple comes down to 21.2 to 24.0 times.

Not cheap. While not directly comparable, Computershare was, according to FN Arena, trading last Friday on a multiple of 14.5 times FY 16 broker consensus earnings and 13.6 times FY 17 earnings. ASX was trading at 18.4 times FY 16 earnings and 17.5 times FY 17 earnings. And Link it is not for income seekers. Dividends will be largely unfranked due to the utilisation of historical tax losses. The first dividend won’t be paid until late 2016 (for the second half of FY 16 only – shareholders won’t get any dividend for the first half), which on an annualised basis, puts it on a yield of approximately 2.4%.

My view

Given the method of pricing the IPO through an institutional bookbuild, this IPO will get away and there may even be a stag premium for initial investors. The question is whether this stock should be a part of a core portfolio, or if there is better value elsewhere. It is hard not to come to the conclusion that Link is expensive and there is better value to be found in other stocks such as Computershare. The latter is quite a different business – an internationally focussed share registry business – while Link is now largely a super fund administrator. The multiple difference, however, is stark.

There is upside with Link. For example, synergy benefits from the Superpartners business are outside the forecast period of FY16. And if Link can continue doing what is has done so well over the last 12 years (acquiring businesses, integrating businesses and value-adding), then the multiples aren’t that far out. There are, after all, few businesses that can boast compound annual growth rates in revenue of 23% and EBITDA of 24%.

While the growth story is plausible, it carries a number of risks – execution risk in the client migration of the Superpartners funds, and industry risks including margin compression and consolidation of super accounts. The balance sheet is largely intangible assets, not unusual for a service business, but there is little to fall back on for that inevitable “rainy day”. Link feels like a business that is priced close to or near to perfection – so on this basis, it is a pass from me. Computershare represents better value.

* Assumes the final price is mid-range at $5.89

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.