In the main, the long-term outlooks for both global and domestic equity markets are solid. Global growth forecasts will continue to increase steadily over the next few years, but in the short term, markets have priced in earnings upgrades and US corporate tax cuts, which are both EPS accretive.

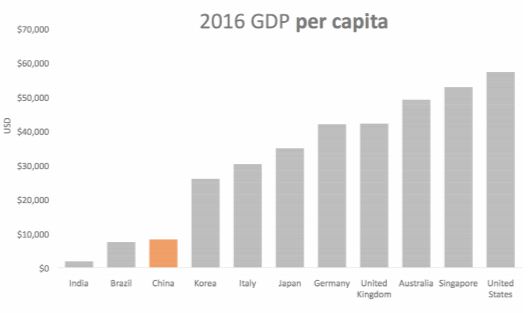

The recovery in emerging markets will continue to follow recent US market strength. Higher US liabilities may remain structural issues for some markets but forecasts for emerging market and developing economies continue to outpace advanced economies, with China’s structural growth story just beginning. The market will continue to second guess China’s growth rate but with a GDP per capita of less than $10,000, it still has a long way to go to catch up to world leader US’s GDP per capita of nearly $60,000.

Chart 1: Per Capita GDP. China is the second largest economy globally but will continue to grow their middle class. Structural growth for China to continue for the decade ahead.

Source: IMF 2016, USD

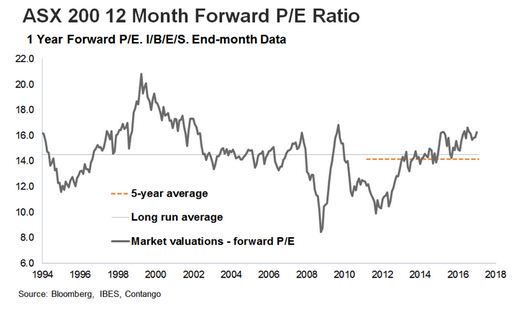

At a domestic level, Australian market valuations are not cheap compared to historical levels as, after a positive half-year reporting season, the market is now pricing in anticipated earnings recovery.

Chart 2: Australian Equity Valuations. Multiples remain above long run historical benchmarks. The long overdue and well anticipated earnings recovery was confirmed in the recent domestic reporting period.

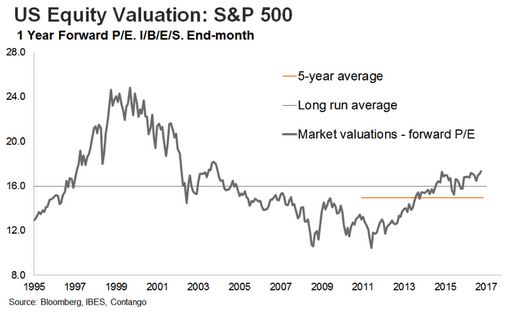

In the US, it’s a similar story. Equity market valuations there are also above long-run historical benchmarks with anticipated US stimulus and tax cuts being priced in.

Chart 3: US Equity Valuations. US equity valuations also above long run averages. Earnings growth momentum in the US has been solid. The current quarterly earnings period in the US is delivering ahead of expectations.

Global market valuations, on the other hand, are below their long-run benchmarks although anticipated upgrades to global GDP are being priced in.

Both Australian equities and international equities provide the domestic investor with different but complementary outcomes. Investors in Australian equities receive higher dividends. In the local market, our large cap sector, in particular, delivers consistent dividends versus offshore peers, with the added boon of franking. Smaller and micro cap sectors can provide higher growth opportunities but there are more of these available to the investor that looks offshore.

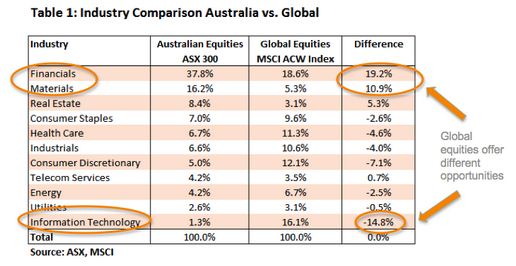

The benchmark index for Australia – the ASX/S&P 300 – has just 300 companies. Compare that to the 2500 companies in the MSCI All Countries World index.

Global equity markets provide access to global growth opportunities under-represented in the local market and have less concentration in certain sectors. One of most obvious examples of this is the IT sector, which makes up just 1.3% of the Australian market but 16.1% of the MSCI All Countries World Index.

The financial sector makes up nearly 40% of the Australian market but accounts for less than 20% of the MSCI All Countries World index.

Comparing a domestic equity growth fund and a global enhanced growth fund, the differences in outcomes become even starker.

The Australian share fund delivers a gross dividend yield of 4.4% net, compared to 1.5% for the global growth fund. In contrast, the global growth fund has EPS growth of 15.5% compared to 4.4% for the Australian share fund.

And let’s not forget that it’s all about the long run, with domestic equities averaging a return of 13.9% per annum since 1959. So, hold on tight for a possible rocky ride ahead, and remember you’re in it for the long haul.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.