[table “267” not found /]

Wall Street has been hijacked by the vote on Capitol Hill in Washington over Donald Trump’s plan to kill Obamacare. The vote was expected close to the closing bell and this is what happened – they pulled the vote!

Before this delay, the Dow was down over 100 points as fear mounted that the President’s health reform bill would not get up!

So what just happened? At 5am when I first put my fingers to work, the vote hadn’t taken place. Political experts said it would be at 3.30pm US east coast time, which is 6.30am our east coast time. So we thought Wall Street might get a chance to react to the actual vote but all it responded to was the pulling of the bill!

This means this market-anxiety we’ve dealt with last week will revisit us next week.

Back home, we gained 0.8% on the S&P/ASX 200 on Friday for a nice win but lost exactly that over the week. And Wednesday showed us all how vulnerable the Trump rally is with the concerns over the US President’s healthcare bill to replace Obamacare and its likelihood of getting up, explaining the Trump dump. It also brought the worst stocks sell off since November.

Of course, this was an overdue sell off after a fantastic rally since the US voter gave us the President the market and, maybe, the world economy had to have!

So to appease Pauline Hanson types, who might say “please explain”, after weeks of the stock market being virtually becalmed with a slight negative inclination, Donald Trump’s potential problems with Congress accepting his healthcare changes raised questions about his likely success on tax reform.

We’re in a testing phase for the market’s optimism about Trump’s policies and the economic outlook, which is unambiguously good for the USA. Australia is more than likely set for pretty good growth. China has surprised its doubters, while Japan and Europe are even bringing economic optimism to the table! Not many experts predicted that six months ago.

I must admit that the great finish to the week made me think that insiders had done the numbers and Donald had trumped the House Freedom Caucus – the extreme right-wingers who wanted a greater erasing of Obamacare than even Donald would do with his American Health Care Act!

All this market consternation was good for defensive stocks and I was happy to see Spark Infrastructure had a good week, up 2.6%. We can thank Investor Mutual’s Anton Tagliaferro for that one. He gave us this company last week.

On the other hand, it was a bad week for iron ore prices, down 7.9% for the week! It was called an “overdue correction” – there’s a lot of this type of thing around at the moment! That said, I liked this in the SMH: “It’s an overdue correction in prices, which have risen too much,” said Ralph Leszczynski, head of research at shipbroker Banchero Costa & Co, in an email on Friday. However he added: “Fundamentals for iron ore remain very strong at present.”

For numbers people out there, benchmark spot ore with 62% content in Qingdao slipped 1.5% to $US85.06 a tonne on Friday. But as I said, this was a 7.9% slump for the week.

Over the week, BHP lost 2.3% but the more iron-exposed Rio lost 4.5% and Telstra didn’t help the cause, giving up 3.6% for the week. I suspected if Trump won over Congress with the healthcare vote and we saw another Wall Street rally, Telstra would’ve been cut a bit of slack but that’s for another time now! However, until CEO Andy Penn comes up with a plan, the company is going to be seen as a no growth stock.

Banks were weak for the week but the rate rise by the CBA on Friday helped soften the anti-market sentiment for bulk of the week.

For those who are into specific stocks tips, FN Arena’s Rudi Filapek Vandyke likes Next DC, ARB, Bapcor, Technology One, Hansen Technologies and Link. Meanwhile, G8 Education, with its $213 million Chinese backer, continues to gain supporters who think the company looks well placed.

What I liked

- The China back down on import restrictions that cruelled the likes of Bellamy’s and Blackmores, with the former up 21% for the week!

- The CBA’s rate rise but only as a shareholder, it might have economic implications to the negative.

- This Monday, March 27 (a special day for me!), AGL Energy will pay its 110,000 shareholders the highest first half dividend in a decade, while its share price has climbed 50% in just six months to record levels around $26. (SMH)

- US existing home sales rose by 6.1% in February to an annual rate of 592,000 units – a seven-month high.

- The number of passengers on the Sydney-Melbourne route rose in January, up 1.6% on a year ago. The Sydney-Melbourne route is a key measure of business activity. For the country, the rise was 2.8% year on year.

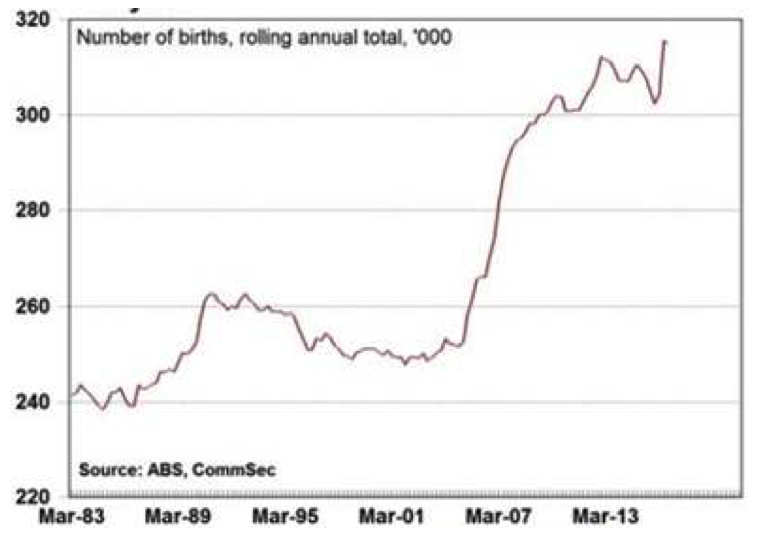

- Australia’s baby boom is well and truly in its 5th year. A total of 315,000 babies were born over the past 12 months – just shy of record highs.

- Employment rose by 80,000 in the three months to February, after a gain of 11,900 in the previous three months. Over the past year, employment lifted by 190,400, the strongest gain in a year.

What I didn’t like

- The House Freedom Caucus!

- The vote being pulled!

- As CommSec’s Craig James noted: “The minutes from the March 7 Board meeting show that the Reserve Bank has upped its rhetoric on the “build-up of risks associated with the housing market”. (My Weekend Switzer option of ‘temporarily’ killing negative gearing for sorting out silly house price rises in Sydney and Melbourne might need to be considered by our number crunchers in Canberra.)

- The Commonwealth Bank Business Sales Indicator (BSI) – a measure of economy-wide spending – rose by just 0.1% in trend terms in February. This is the slowest growth in two years.

- Downer shares tumbled to five-month lows, following a capital raising to finance a $1.2b bid for Spotless, with experts arguing they’re paying too much. Historically, this is a company that has been hard on shareholders! (I haven’t held this stock, ever!)

- The Harvey Norman blow up, which has gone from directors selling stocks to questions over Gerry’s books when it comes to franchisees and related losses. HVN was down 7.8% for the week but it was a bad one for retailers generally, with Myer off 6.2%. In the US, the retailers funeral continues, with Sears and Kmart to close 150 stores!

- The US and UK laptop ban on flights out of the Middle East and North African airports. I’d like better scanning technology.

One final like

My radio ratings doubled for my On the Money show on the Talking Lifestyle program in Sydney, Melbourne and Brisbane between 4pm and 5pm in the former two cities and 3pm to 4pm in Brissie!

The week in review:

- Sometimes it pays to be a contrarian, just look at BHP! So this week, I wrote about quality companies that are contrarian plays right now.

- This week, James Dunn revealed five promising – but highly speculative – miners.

- Roger Montgomery took the pulse of two healthcare stocks, Ramsay and Healthscope.

- The brokers upgraded BHP Billiton but CSL received a downgrade.

- In our second broker report, there were two downgrades for TPG, while Ramsay Health Care was upgraded.

- Our Stock Selectors liked IPH and JB Hi-Fi, while GPT was out of favour.

- Tony Featherstone explained why Catapult Group, a leading provider of athlete mentoring and analytics, could have a healthy long-term outlook.

- Charlie Aitken revealed an Aussie small cap to put on your watch list.

- And Lance Lai shared his notes from his appearance on Switzer TV.

Top stocks – how they fared

What moved the market?

- The “Trump slump”. Investors remained cautious on whether Congress will play ball with The Donald!

- News that China will back down from tougher e-commerce laws helped Bellamy’s and Blackmores.

Calls of the week

- My call that Blackmores, Domino’s and Vocus look like quality contrarian plays right now!

- Speaking of contrarian calls, Paul Rickard also said TPG is a contrarian buy. Find out why.

- Former PM Julia Gillard was named as the new chair of beyondblue, and will replace Jeff Kennett on July 1.

- Apple introduced a red iPhone 7, with contributions from purchases going to the Global Fund for HIV and AIDS programs.

- And British MP Tobias Ellwood made a heroic call to try to save the life of an injured policer officer in the London attack. Our thoughts are with the victims.

The week ahead

Australia

- Tuesday March 28 – Weekly consumer confidence

- Tuesday March 28 – Speech by Reserve Bank official

- Thursday March 30 – Finance and wealth (December quarter)

- Thursday March 30 – Job vacancies (February)

- Thursday March 30 – New home sales (February)

- Friday March 31 – Private sector credit (February)

Overseas

- Tuesday March 28 – US Case Shiller home prices (Jan)

- Tuesday March 28 – US Richmond Federal Reserve

- Tuesday March 28 – US Consumer confidence

- Wednesday March 29 – US Pending home sales (February)

- Thursday March 30 – US Economic growth (Dec quarter)

- Friday March 31 – US Chicago purchasing managers

- Friday March 31 – US Personal income (February)

- Friday March 31 – China purchasing managers

Food for thought

Only the guy who isn’t rowing has time to rock the boat.

- Jean-Paul Sartre

Last week’s TV roundup

- Treasurer Scott Morrison joins Super TV for an overview of the recent G20 meeting, the state of the Aussie housing market, and where the Australian economy is heading.

- Michael Heffernan from Phillip Capital joins the show to share his views on the stock market and the stocks he’s watching right now.

- King of charts Lance Lai from Accountancy Invest joins Super TV to share what the charts are saying about local and global markets and more.

- China’s backflipping on regulations have impacted the likes of Bellamy’s and Blackmores, so is the decision set to have any further influence on the Australian market? To discuss, Contango’s George Boubouras joins the show.

- What can the RBA do with interest rates? Should the Government remove negative gearing for two years? To share his views, AMP Capital’s Shane Oliver joins Super TV.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

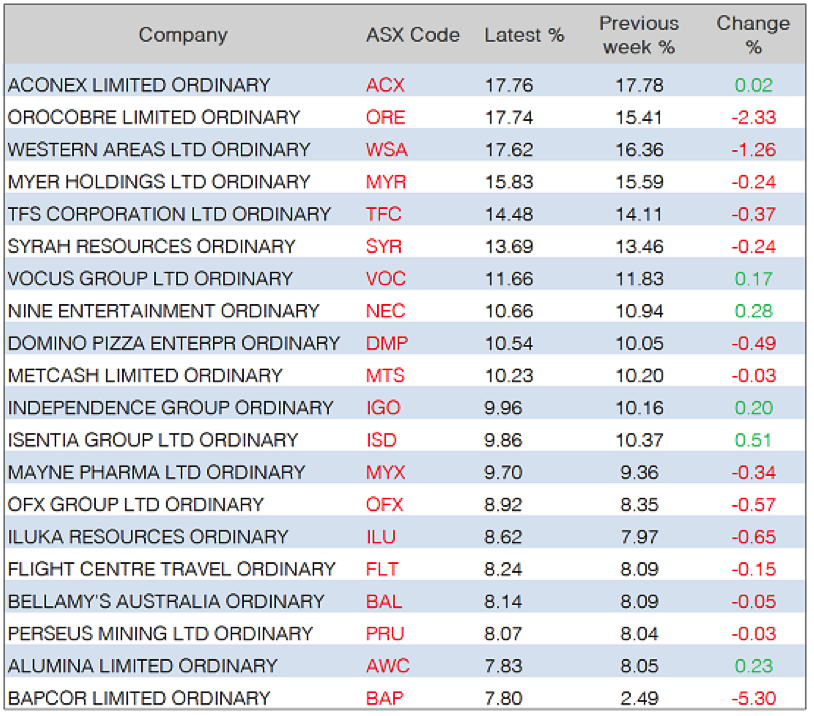

This week one of the biggest movers was Bapcor, with a 5.3 percentage point increase in its shares sold short to 7.80%.

Source: ASIC

Chart of the week

It’s a baby boom!

Source: ABS, CommSec

Check out this chart, which shows the epic amount of babies born over the past 12 months! According to CommSec, 315,000 little babes were born – just shy of record highs.

Top five most clicked stories

- Peter Switzer: What quality companies are contrarian plays right now?

- Paul Rickard: Is Telstra a buy, yet?

- Charlie Aitken: Stock to watch: another small cap with a growing dividend yield

- Roger Montgomery: A (re)visit to the hospital: Healthscope and Ramsay

- James Dunn: 5 promising miners

Recent Switzer Super Reports

- Thursday 23 March, 2017: Small caps in focus

- Monday 20 March, 2017: Big lessons

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.