It was a trading week that will be easily forgotten but after a shocker the week before, when $50 billion of value was wiped off Aussie shares, I’m happy with even a 21-point gain for the week to close at 6165.30. And keeping us out of the red was another good week for tech and a nice rebound for the energy sector.

Oil prices spiked and it wouldn’t surprise any of the 2,000 people who went to the Switzer Listed Investment Companies conferences in Brisbane, Melbourne and Sydney last week, with two fund managers bullish on commodities, even with the Trump trade threat hovering over markets. Yep, anyone looking for reasons why our market can’t easily beat gravity, just think Donald plus Royal Commission plus the leadership squabbles in Canberra and the pending threat of a probable Prime Minister Bill Shorten out there for investors to consider.

On the US President, he was at it again overnight, with stocks erasing early gains, after he decided that the market had to hear, though it was clearly intended for his Chinese counterparts, that he wants to go ahead with his $US200 billion worth of tariffs on Chinese goods. That said, the negative reaction was not over-the-top, which either says key market players have adjusted their stock plays for an escalation of the Trump trade war with China or they don’t think it will eventuate.

“Trade has been the only thing holding this market back,” said Randy Frederick, vice president of trading and derivatives at the Schwab Centre for Financial Research, to CNBC. This implies that if a better-than-expected trade deal can be created, then stocks could take off. Gee, I hope that’s the method in the US President’s madness.

Back home and Origin Energy went up 7.9% for the week to $8.33, while Woodside put on 3.3%. Meanwhile, the speculators came back for Afterpay, up 15.1% to $17.27 over the week, while Wisetech Global gained 3.8%, Altium 2% and Appen 2.8%, while NEXTDC rose 3%. These are promising companies but the likes of Investors Mutual’s Anton Tagliaferro thinks they won’t rise forever and late-to-the-party buyers will learn the lesson of speculators versus investors.

Not helping the index track higher was another bad week at the office for bank and finance stocks and we ‘thank’ the Royal Commission for this. Anyone thinking I’m biased towards a future PM Bill Shorten, remember that he wants to extend the Commission so all people who want their day in court can get it! Personally, I’ve always argued that those wronged by bad behaviour from financial institutions get compensation through a consumer claims tribunal with no lawyers, would be better than a extended witch hunt that would not only be bad for the brand names of financial businesses but terrible for their share prices and therefore super funds!

Getting even for exploited consumers should not be political but it has to be meaningful for the bottom lines of the aggrieved and the perpetrators.

The past week also showed that leadership was an issue for the economy and it had to have some stock price effect. The NAB business confidence index dropped from 7 points in July to a 25-month low of 4.4 points in August, while the long-term average is 6 points. This was the first reading since Malcolm Turnbull copped the bullet. Meanwhile, the Westpac/Melbourne Institute survey of consumer sentiment index fell by 3% to 100.5 in September – the lowest level in 10 months! The index is now below its long-term average of 101.5. A reading above 100 denotes optimism.

Importantly, while these two readings on business and consumer expectations have told us that the future is less positive and leadership worries were relevant, the latest reading for business, i.e. business conditions, tells a different and very positive business yarn. Yep, the NAB business conditions index, which says what businesses are saying right now about their operations, rose from 12.6 in July to a 4-month high of 15.2 in August, with the long-term average being 5.7!

The job ahead for PM Scott Morrison is to show he’s a chance to be a long-shot threat to Bill Shorten at the next election. Morrison might not be able to peg back the Labor Opposition (which is ahead 56% to 44% on a two-party preferred basis) but he might be able to force Bill to hose down some of his harsher and more fiery anti-investor policies.

Finally, the Oz dollar crept higher over the week and helping this happen was the better-than-expected jobs report, when 44,000 jobs showed up when the economists’ tip was more like 20,000. The fingerprints of the ex-Treasurer turned PM could one day come back to actually help him as he tries to build his credibility as a leader and rebuild his Government’s credibility, which has been hurt by its leadership revolving door problem.

By the way, this higher dollar suggests the combined impact of the recent 3.4% economic growth number and the fact that the economy is still raining down jobs, says those tipping the first RBA cash rate rise will be 2020, should be proved wrong. I stick with my 2019 call.

What I liked

- Employment rose by 44,000 in August, after a revised 4,300 fall in jobs in July (previously reported as a 3,900 fall). Full-time jobs rose by 33,700 and part-time jobs rose by 10,200. Economists had tipped an increase in total jobs of around 18,000.

- Unemployment was steady at 5.3% in August. In trend terms, the jobless rate eased from 5.4% to 5.3% – the lowest since October 2012.

- The participation rate rose from 65.6% to 65.7%.

- In trend terms, the unemployment rate for 15-24 year old persons hit a 7-year low of 11.2%. The jobless rate for 15-19 year old persons was at a 5-year low of 16.2%.

- Unemployment expectations fell by 6.6% to near seven-year lows of 120.7 to be 9.6% lower than a year ago in September.

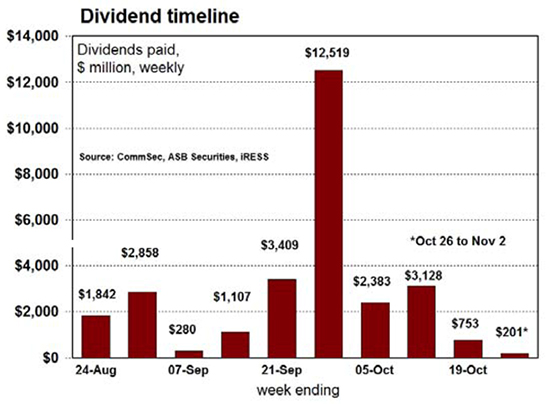

- Since late August, ASX 200 companies have paid out around $6 billion in dividends to shareholders but dividend payouts really start to ramp up from next week. Dividends totalling $21.4 billion will be paid out by listed companies to their shareholders in the next four weeks.

- The average credit card balance fell by $54.60 to $3,223.70 in July, down from five-year highs of $3,278.30 in June. But balances were up by 5% over the year – the strongest annual growth rate in a decade. In smoothed terms (12 month average), the average balance was up by 1.3% – the strongest annual growth rate in six years.

- In the US, the NFIB business optimism index rose from 107.9 to 108.8 in August (forecast 108.2).

- US consumer prices rose by 0.2% in August (forecast +0.3%), to be up 2.7% over the year. Excluding food and energy (core measure), prices rose by 0.1% (forecast +0.2%), with the annual rate down from 2.4% to 2.2%.

- The Turkish central bank lifted rates by 625 basis points, boosting the lira by 4% versus the US dollar.

What I didn’t like

- The leadership/confidence impact but I suspect it will be a short-term thing.

- China and the US remained open to the possibility of new trade talks but President Trump said he felt no pressure to make a deal.

- China told the World Trade Organisation it wanted to impose $7 billion a year in sanctions on the US in retaliation for Washington’s non-compliance with a ruling in a dispute, initiated in 2013, over U.S. dumping duties.

- The Goldman Sachs bear market indicator looks scary but it’s at odds with the Citi list of 18 indicators that say ‘don’t be worried’ (I will be investigating this discrepancy this week).

Thank you

I’d like to thank those who attended our conferences this week. The feedback was fantastic and it’s exhilarating to have so many people come up to me to thank my team and our fund managers for the insights they offered. If you missed out this time, I hope you can show up the next and we’ll always keep you posted when they’re on.

The Week in Review:

- I looked at 5 solid stocks outside the top 10 that pay reliable income, and whether or not you should buy Gerry.

- Paul Rickard wrote that it’s time to take advantage of the bank bashing and get back in.

- Reporting season proved to be good for these four stocks that are on the comeback trail according to James Dunn.

- Charlie Aitken explained why he has dropped former favourite Speedcast.

- RCR Tomlinson has been added to the Switzer Report takeover portfolio.

- Contango Asset Management’s Shawn Burns chose Scottish Pacific Group as the Stock of the Week.

- The first Buy, Hold, Sell – what the brokers say for the week saw an upgrade for Orocobre, while CBA and Origin Energy were among those in the good books in the second edition.

- In Questions of the Week, we shared a reader’s response on how to invest in the Asian BATS.

- Our Hot Stocks for the week are Mayne Pharma Group and Biotron.

Top Stocks – how they fared:

What moved the market?

- The US dollar dipped in response to weak inflation data, with the Australian dollar moving a fraction higher

- Commodities, particularly oil, saw a slight bounce

- Revelations from the banking royal commission hearings on life insurance

Calls of the week:

- Paul Rickard chose Westpac as the bank to buy.

- Charlie Aitken said for a stock like Speedcast, “it is prudent to fall on your sword, admit you made a mistake and sell”.

- The miners who struck $15 million worth of gold specimens in Kambalda, around 600km east of Perth.

The Week Ahead:

Australia

Tuesday September 18 — Weekly consumer sentiment

Tuesday September 18 — Residential price indexes (June Quarter)

Tuesday September 18 — Reserve Bank Board minutes

Wednesday September 19 — Speech by Reserve Bank Assistant Governor

Thursday September 20 — Business Sales Indicator (August)

Thursday September 20 — Population (March quarter)

Thursday September 20 — Detailed jobs data (August)

Overseas

Monday September 17 — US Empire State Manufacturing (September)

Tuesday September 18 — US NAHB housing market (September)

Wednesday September 19 — US Housing starts (August)

Wednesday September 19 — US Current account balance (June quarter)

Thursday September 20 — US Philadelphia Federal Reserve (September)

Thursday September 20 — US Leading index (August)

Thursday September 20 — US Existing home sales (August)

Friday September 21 — ‘Flash’ purchasing manager surveys (September)

Food for thought:

Where can you finish reading several books before you finish even one sentence?

Send in your answer to subscriber@switzer.com.au

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week:

Chart of the week:

Dividend payouts will begin to ramp up from next week. $6 billion in dividends has been paid out by ASX 200 companies since late August, with an additional $22.5 billion being distributed in the coming weeks, as seen in this chart from CommSec:

Source: CommSec

Source: CommSec

Top 5 most clicked:

- 5 solid stocks that pay reliable income – Peter Switzer

- Banks are a buy! – Paul Rickard

- 4 stocks on the comeback trail in 2018 – James Dunn

- Buy, Hold, Sell – what the brokers say

- Speedcast hits a speed bump – Charlie Aitken

Recent Switzer Reports:

- Monday 3 September: Bonanza buys

- Thursday 6 September: Know when to walk away

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.