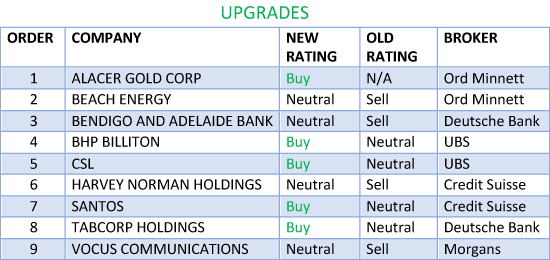

In the good books

ALACER GOLD CORP (AQG) Upgrade to Buy from Hold by Ord Minnett B/H/S: 5/0/0

Despite gold being Ord Minnett’s least preferred exposure, with valuations screening more expensive than peers, Alacer Gold is upgraded to Speculative Buy from Hold.

The broker recognises that cheap valuations are not a catalyst for the stock to re-rate but believes sentiment is likely to move back in the direction of risk-on over the medium term. Target remains unchanged at $2.70.

BENDIGO AND ADELAIDE BANK LIMITED (BEN) Upgrade to Hold from Sell by Deutsche Bank B/H/S: 0/2/4

Deutsche Bank’s sector update is all about “mitigation” with the analysts taking the view the major banks should be able to offset the negative impact from the government’s levy by half, reducing the impact to -1-2% per annum.

On this basis, Deutsche Bank suggests all bad news has been priced in, plus some. Top picks in the sector remain National Australia Bank and Westpac. Bendigo and Adelaide Bank is the sole recipient of an upgrade in rating; to Hold from Sell, following share price weakness.

BHP BILLITON LIMITED (BHP) Upgrade to Buy from Neutral by UBS B/H/S: 5/3/0

The stock is down around -5% in the year to date, underperforming rival Rio Tinto (RIO) by -10%. UBS observes near-term momentum in China is negative but the company is still expected to report robust second half earnings and pay a $0.56 per share dividend.

BHP remains out of favour and under growing pressure to show its strategy is working. UBS envisages potential for further disposals near term, which will accelerate de-leveraging and position the company to step up its returns more aggressively in FY18.

On this basis the broker upgrades to Buy from Neutral. Target is $28.

BEACH ENERGY LIMITED (BPT) Upgrade to Hold from Lighten by Ord Minnett B/H/S: 1/4/1

The stock has fallen -32% since December, making the valuation more attractive. Ord Minnett raises its recommendation to Hold from Lighten. Target is $0.65.

The broker envisages the next catalysts are further exploration, that may mean reserve life extensions, mergers or acquisitions, and increased uncommitted production which could mean realisation of attractive domestic gas prices.

CSL LIMITED (CSL) Upgrade to Buy from Neutral by UBS B/H/S: 5/1/0

UBS now believes the company can sustain around 11% volume growth for plasma to FY25 to meet the robust end-product demand globally.

The broker finds it increasingly apparent that competitor Shire will pursue a less capital intensive brand & price strategy. This confirms a long-term structural advantage to CSL.

The broker upgrades to Buy from Neutral and raises the target to $145.00 from $132.15.

HARVEY NORMAN HOLDINGS LIMITED (HVN) Upgrade to Neutral from Underperform by Credit Suisse B/H/S: 2/2/2

Credit Suisse reduces earnings and valuation estimates for the company, assuming the market becomes increasingly competitive.

Electrical retail faces increasing challenges from delivery economics at scale and downward pressure on delivery fees, as well as higher promotional expenditure and stranded costs as the electrical market moves increasingly online.

While there has been considerable discussion about the consolidation of franchisee accounts, the broker believes a materially adverse outcome is unlikely. Rating is upgraded to Neutral from Underperform because of the significant underperformance of the share price. Target is reduced to $4.08 from $5.12.

SANTOS LIMITED (STO) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 5/3/0

With oil at the lower end of its trading range and much weakness priced into the stock since the Australian domestic gas security mechanism was first floated, Credit Suisse envisages some short-term upside for the stock.

The mechanism may hurt Santos but the broker believes much of this hurt has been priced in. Acknowledging a brave call, the broker upgrades to Outperform from Neutral. Target is $3.80.

TABCORP HOLDINGS LIMITED (TAH) Upgrade to Buy from Hold by Deutsche Bank B/H/S: 3/0/1

Deutsche Bank upgrades to Buy from Hold as the stock is trading at a -6% discount to valuation and this excludes any benefit from the proposed merger with Tatts (TTS).

The broker estimates a merger could provide earnings and valuation upside of 11% and the regulatory environment is improving for traditional wagering operators.

While the Australian Competition Tribunal has delayed its determination on the merger to no later than September 10 2017, from June 13 previously, the broker believes this could still result in a positive outcome, albeit subject to conditions.

Target is reduced to $4.80 from $5.00.

VOCUS COMMUNICATIONS LIMITED (VOC) Upgrade to Hold from Reduce by Morgans B/H/S: 0/8/0

KKR’s $3.50 bid for Vocus is preliminary, indicative, non-binding, and comes with no less than 13 exit clauses. There is therefore no guarantee the bid will proceed, Morgans notes.

The market has nevertheless priced in success, and even if nothing happens, Morgans sees little further downside risk to earnings from here. Target increased to $3.50 from $1.97 to match the bid. Upgrade to Hold.

In the not-so-good books

CALTEX AUSTRALIA LIMITED (CTX) Downgrade to Underweight from Equal-weight by Morgan Stanley B/H/S: 5/0/1

Morgan Stanley believes consumption of premium petrol across Australia has peaked and is now declining and lower volumes are likely to lead to price-based competition across retailers, particularly for premium fuels.

Moreover, the Australian consumer is under pressure and this is likely to affect premium fuel volumes further, and there is a global movement under way to cleaner fuels.

The broker also notes a growing probability that the Australian government will ban regular unleaded and impose lower sulphur limits on all fuel types.

The broker believes investors will price Caltex on an underlying basis excluding the Woolworths (WOW) supply contract and downgrades to Underweight from Equal-weight. Target is reduced to $27.00 from $32.60. In-Line industry view.

GOODMAN GROUP (GMG) Downgrade to Lighten from Hold by Ord Minnett B/H/S: 2/4/0

Ord Minnett observes the operating performance was solid in the third quarter. Development yields are increasing and work in progress stated at $3.5bn.

Despite the good numbers, Ord Minnett downgrades to Lighten from Hold on valuation grounds as the stock is trading on a forward price/earnings ratio of 19.7x.

Historically, the broker observes stock traded at a price/earnings discount versus the sector but the recent strong run has meant the relationship has inverted to a premium, and in the last 12 months the stock has recorded a total shareholder return of 21% versus the sector’s gain of just 2%. Target is raised to $7.80 from $7.60.

IOOF HOLDINGS LIMITED (IFL) Downgrade to Neutral from Buy by Citi B/H/S: 0/4/1

Citi analysts observe the company is presently surrounded by positive news flow. They anticipate the trend in Funds under Administration (FuA) growth should be accelerating at this point in time.

Alas, the share price has rallied too, and this triggers the downgrade to Neutral from Buy. Target price remains untouched at $9.40. Estimates haven’t moved either.

MACQUARIE ATLAS ROADS GROUP (MQA) Downgrade to Hold from Add by Morgans B/H/S: 2/4/0

Morgans has trimmed its target for Mac Atlas to $5.98 from $6.05 to reflect the performance fee the broker expects Mac Atlas to owe Macquarie Group (MQG) for this financial year.

Otherwise, a co-investor in the APRR has announced it will exit its 31.2% stake. Macquarie Atlas has sixty days to decide whether or not and how much of the stake it might acquire. A capital raising may be required, Morgans notes. Given a lot of uncertainty, the broker pulls back to Hold.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.