The week ending Friday, 26th October 2018 proved unusually busy for a five day term outside of companies reporting financial results.

FNArena registered no less than 16 downgrades and 24 upgrades in recommendations for individual ASX-listed stocks. A number of stocks received multiple changes, with representations on both sides of the ledger, including AMP, Brambles, Regis Resources, Super Retail, and Northern Star Resources.

Local out-of-season financial reporting is about to ramp it up one notch, turning investor focus to banks and dividends, while macro concerns continue to weigh.

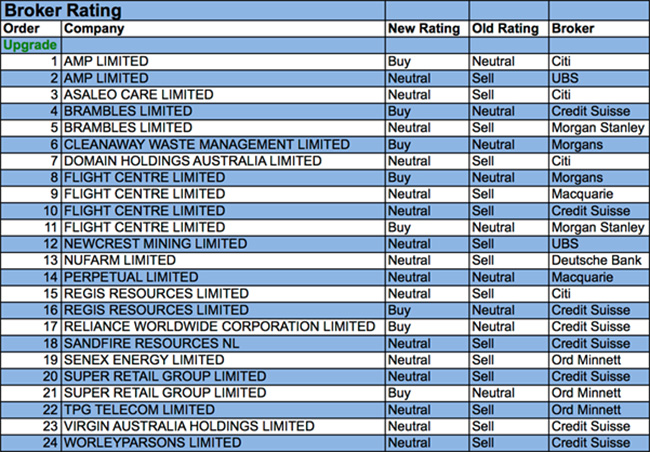

In the good books

AMP LIMITED (AMP) was upgraded to Neutral from Sell by UBS and to Buy from Neutral by Citi. B/H/S: 3/5/0. AMP has announced the sale of its wealth protection and NZ Life businesses for $3.3 billion. The company intends to divest its NZ wealth business via an IPO in 2019. A further $150 million will be realised from a reinsurance transaction with Swiss Re for NZ Life. After the share price decline UBS believes valuation support is beginning to emerge and upgrades to Neutral from Sell. Target is reduced to $2.50 from $2.80. After yet another sharp sell-off, Citi analysts dare to stick their neck out and declare “value” might now be emerging in the shares. Target price drops to $2.85 from $3.50.

See also AMP downgrade.

CLEANAWAY WASTE MANAGEMENT LIMITED (CWY) was upgraded to Add from Hold by Morgans. B/H/S: 3/3/0. Morgans observes the share prices declined by almost 20% from its high in August. This provides a buying opportunity, with the broker calculating total potential returns over the next 12 months of around 14%. The company continues to win large contracts while extracting synergies from the Toxfree acquisition, and has indicated it will not compromise the latter’s existing business. Target is raised to $1.89 from $1.86.

NEWCREST MINING LIMITED (NCM) was upgraded to Neutral from Sell by UBS. B/H/S: 3/4/1. UBS reduces the discount rate used to value Newcrest Mining. The broker acknowledges that valuing the stock with a 10% discount rate can undervalue the long mine life at the three key assets and now uses a 5% discount, upgrading to Neutral from Sell. Target is raised to $22.00 from $14.30. Nevertheless, the broker considers production and earnings momentum is worrying as this will peak in the next two years because of the grade decline at Cadia before Golpu enters production in the mid 2020s.

PERPETUAL LIMITED (PPT) was upgraded to Neutral from Underperform by Macquarie. B/H/S: 0/6/1. Perpetual’s outflows accelerated to $1.0bn in the September quarter from outflows of $0.3 billion in June, predominantly from Australian equities. A challenging environment for value managers and the departure of the general manager of wholesale distribution suggests to the broker further downside risk. A weak share price nevertheless suggests the emergence of valuation support.

RELIANCE WORLDWIDE CORPORATION LIMITED (RWC) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 4/1/0. Credit Suisse observes growing concern over the US housing market but contends that difficult end market conditions provide opportunities. The broker also finds no deterioration from Home Depot’s trial of competing PTC fittings. While the John Guest acquisition adds significant value, the broker suggests growth in Europe will be slower and more difficult than in the US. Target is reduced to $5.60 from $5.70.

SANDFIRE RESOURCES NL (SFR) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 1/4/2. September quarter production was strong, amid positive grade reconciliation, although continued outperformance in grade is not expected. Despite the development at Monty being behind schedule, it is now on a critical path and infill drilling has commenced. Credit Suisse upgrades to Neutral from Underperform on valuation grounds. Target is steady at $6.70.

SUPER RETAIL GROUP LIMITED (SUL) was upgraded to Neutral from Underperform by Credit Suisse and to Accumulate from Hold by Ord Minnett. B/H/S: 3/5/0. The company provided a subdued trading update and indicated its CEO would step down in the first half of 2019. Like-for-like sales growth slowed through the past 10 weeks and Credit Suisse suspects additional margin pressure is being experienced in an increasingly difficult retail environment. The broker upgrades to Neutral from Underperform on valuation grounds because of the slump in the share price but notes the potential for further disappointment in the near term. Target is $8.39. Ord Minnett believes the reaction in the share price to the AGM update is too severe, and upgrades to Accumulate from Hold. Target is unchanged at $9.50.

See also SUL downgrade.

TPG TELECOM LIMITED (TPM) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 2/1/2. Ord Minnett reviews its investment case and finds both upside and downside risk to its calculations. Upside would come from the fixed wireless broadband opportunity or lower wholesale NBN costs. This is offset by the risk that the Australian Competition and Consumer Commission blocks the merger with Vodafone Australia. The broker upgrades to Hold from Lighten as the stock is trading below the unchanged target of $7.90.

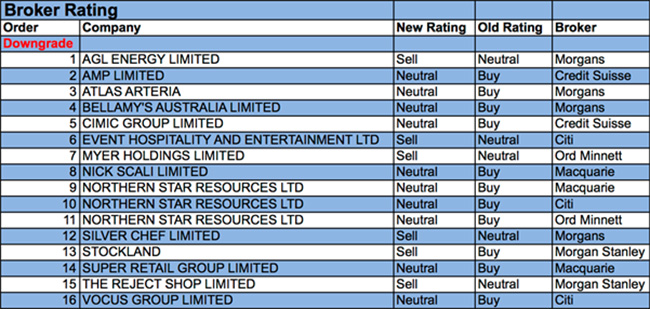

In the not-so-good books

AGL ENERGY LIMITED (AGL) was downgraded to Reduce from Hold by Morgans. B/H/S: 2/2/3. The federal government has asked the regulator to implement a default pricing policy to replace standing offers. The exact mechanism is yet to be determined and a new pricing structure will not be revealed until January 2019. While AGL has only 4% of its customers on standing offers, Morgans believes there will be pricing pressure across the retail market. The broker’s estimates show that a 10% reduction in retail prices from current levels would reduce FY20 net profit by over $100m. Target is lowered to $16.89 from $19.78.

AMP LIMITED (AMP) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 3/5/0. The company has announced the sale of Australian & NZ wealth protection and mature business assets at a much larger discount than Credit Suisse assumed. Furthermore, the broker is not confident investors will get to enjoy the proceeds for a number of years, if at all. The broker believes the willingness to go ahead with the deal indicates that AMP is prepared to write off significant value in an effort to reshape the company. The broker downgrades to Neutral from Outperform and lowers the target to $2.65 from $4.30.

See also AMP upgrade.

EVENT HOSPITALITY AND ENTERTAINMENT LTD (EVT) was downgraded to Sell from Neutral by Citi. B/H/S: 1/0/1. Citi analysts see downside risks to FY19 earnings momentum, which is driving their decision to downgrade to Sell from Neutral. Medium-to-long-term, the analysts admit this company has growth potential from its property development pipeline, plus the shares look “cheap” on current multiples. Estimates have been cut. Target price falls by 16% to $12.95.

MYER HOLDINGS LIMITED (MYR) was downgraded to Lighten from Hold by Ord Minnett. B/H/S: 0/2/3. Having toured the company’s Southland store, Ord Minnett notes a greater emphasis on gifting, discounting discipline and operating earnings. Given the share price performance since the FY18 result, and despite a recent retracement, the broker believes valuation support has reduced, leading to a downgrade to Lighten from Hold. Target is $0.43.

NORTHERN STAR RESOURCES LTD (NST) was downgraded to Neutral from Outperform by Macquarie, to Neutral from Buy by Citi and to Hold from Accumulate by Ord Minnett. B/H/S: 0/4/3. Northern Star posted a solid September quarter production report, Macquarie suggests. Costs were higher, but impacted by mill constraints at Pogo and an inventory build at Kalgoorlie.

First data from Pogo highlighted a key opportunity, the broker believes, and a more aggressive ramp-up leads to a target price increase to $9.80 from $9.40. The broker has nonetheless downgraded to Neutral from Outperform on valuation. Citi’s downgrade is the result of a firm rally in the share price. Citi acknowledges the Pogo acquisition will be “transformational” for the company, but it’s already in the price. Citi downgrades but adds $1 to the price target; $9.25 instead of $8.25, as a result of higher forecasts for gold in AUD for FY19-FY21.

September quarter production was below Ord Minnett’s estimates because of lower output at the Pogo operation. The company has flagged productivity gains and expects costs to fall from the March quarter 2019. While the stock is not particularly expensive, the broker observes it is trading ahead of mid-cap peers and downgrades to Hold from Accumulate. Target is steady at $9.

SUPER RETAIL GROUP LIMITED (SUL) was downgraded to Neutral from Outperform by Macquarie. B/H/S: 3/5/0. Super Retail’s sales growth in the September quarter was in line with expectations. Auto was solid, Rebel was good, Macpac was strong and, as usual, BCF brought the team down. Management commentary was cautious nonetheless, suggesting signs of weakening consumer sentiment and forcing the need to balance sales growth and manage margins. Investor sentiment is likely to remain cautious with regard the retail sector, and the departure of the CEO adds to uncertainty. Target falls to $8.70 from $10.50.

See also SUL upgrade.

THE REJECT SHOP LIMITED (TRS) was downgraded to Underweight from Equal-weight by Morgan Stanley. B/H/S: 0/1/1. Morgan Stanley has re-based expectations on the back of the company’s recent profit downgrade. Comparable sales have deteriorated in the first weeks of FY19, attributed to weakness in the retail environment, increasing competition and promotional pricing. Morgan Stanley finds it difficult to envisage this will ease in the lead up to Christmas. The broker does not rule out another profit downgrade post Christmas and, if conditions persist, believes there is a risk of a loss sooner rather than later. Target is reduced to $2.10 from $6.10. In-Line industry view.

VOCUS GROUP LIMITED (VOC) was downgraded to Neutral from Buy by Citi. B/H/S: 0/5/1. Vocus is in a transition year, Citi suggests, with new management in place, which should provide for a rebase for earnings growth from FY20. The broker sees a meaningful step-up in earnings over the longer term but it is a three-year recovery story. With no meaningful upgrades likely this year and the stock price approaching Citi’s target, the broker downgrades to Neutral from Buy. Target unchanged at $3.65.

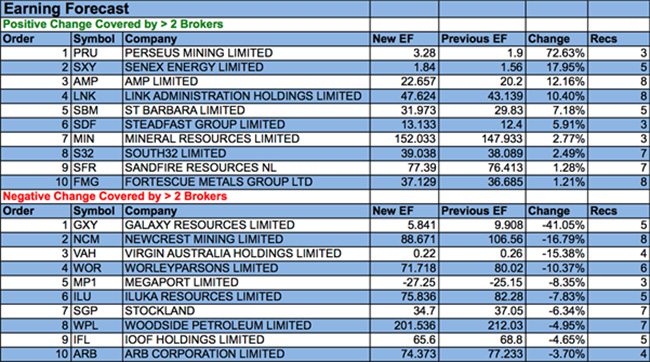

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.