The local share market keeps treading water, trying to stabilise while keeping a watchful eye on whatever happens on Wall Street, but at least stockbroking analysts are responding in the most positive manner: by issuing recommendation upgrades for weakening share prices.

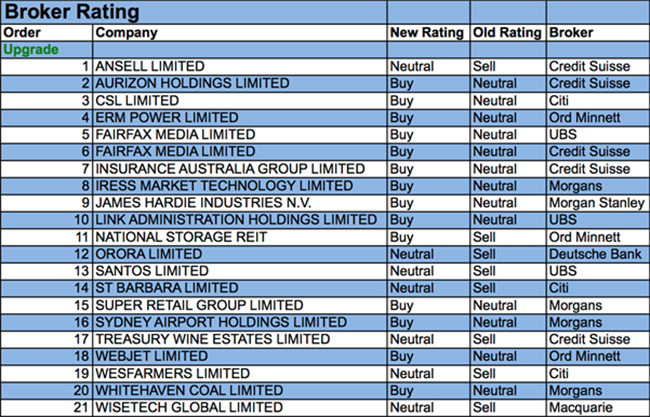

For the week ending Friday, 19th October 2018, FNArena registered no less than 21 upgrades for individual ASX-listed stocks, versus two downgrades only. So which stocks still received downgrades?

Actually, there is only one. Jewellery retailer Michael Hill cannot shake off the habit of releasing disappointing market updates and this time yet another tough admission has been met with two downgrades. Both went to Sell, or an equivalent of Sell.

Apart from macro-economic events, investors have plenty to keep an eye out for in the week(s) ahead, from AGMs, to trading updates, to quarterly reports, to (soon) Australian banks releasing financial results.

In the good books

ANSELL LIMITED (ANN) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 2/6/0. Credit Suisse observes, since the FY18 result, the share price has fallen 15%. The broker now considers the risks balanced and the share price supported by the buyback program, a net cash position and potential for M&A. The broker updates assumptions regarding foreign exchange and higher raw material prices, resulting in 3% downgrades to earnings estimates. Target is lowered to $23.50 from $24.00.

AURIZON HOLDINGS LIMITED (AZJ) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 2/3/3. First quarter above-rail volumes were down 8%. Credit Suisse lowers coal volumes for FY19 by 3% and reduces coal earnings by 4%. The broker raises FY19 bulk earnings by 8%, believing the company could reach agreement with Linfox to sell the Queensland Intermodal business. The Queensland Competition Authority has indicated it will consider a change to the averaging period for the risk-free rate and, if implemented, this could increase the company’s operating earnings by around $20m a year. Credit Suisse upgrades to Outperform from Neutral on valuation and a potentially favourable announcement by the QCA. The company’s court case against the Queensland Competition Authority, alleging the former chairman was conflicted, starts on October 22. Credit Suisse reduces the target to $4.50 from $4.60.

CSL LIMITED (CSL) was upgraded to Buy from Neutral by Citi. B/H/S: 3/5/0. Citi analysts have re-assessed their investment view and forward modelling now that the share price has corrected noticeably in line with rising bond yields. While the share price target has been reset at $218, from $238, with the added comment this includes some $12 for CSL112, the recommendation has also been upgraded to Buy from Neutral. Also, the analysts highlight at their revised target price, CSL shares will be trading on an FY20 PE of 31x; this compares with the three year average of 28x (thus still at a historic premium).

ERM POWER LIMITED (EPW) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 3/0/0. The company has signed an agreement to sell its US subsidiary Source Power & Gas to Direct Energy for US$27 million, effectively simplifying the investment proposition for investors, say the analysts. For company management, this deal now offers the opportunity to concentrate solely on Australian retailing with Ord Minnett adding the shares look cheap/attractive while offering a history of stable retail margins. Target price lifts to $1.90 from $1.60.

INSURANCE AUSTRALIA GROUP LIMITED (IAG) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 2/5/1. Over the past two years the company’s margin in commercial lines has not improved to the extent Credit Suisse had expected, despite premium rate increases. The broker suspects a large part of the reason stems from the exit of the Swann business. With some of the distortions to historical margins now explained, the broker is more comfortable about the guidance set by the company for FY19. Further capital management is also considered likely and Credit Suisse allows for a further $600 million, 50:50 special dividend to buyback. Target is steady at $7.90.

NATIONAL STORAGE REIT (NSR) was upgraded to Accumulate from Lighten by Ord Minnett. B/H/S: 2/1/1. Ord Minnett better understands how self storage is valued, where the transactions occur and the return on capital, after discussions with key stakeholders in the industry in Australia. The broker reviews the company’s financials and lifts free cash flow forecasts materially. The target is raised to $1.85 from $1.55. Ord Minnett forecasts compound annual growth in earnings per share for the next three years of 5-6%.

ORORA LIMITED (ORA) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 2/6/0. Deutsche Bank observes the share price has underperformed the market over the past three months, while the company has reiterated full-year guidance for underlying earnings growth, subject to global economic conditions. Target is $3.20.

ST BARBARA LIMITED (SBM) was upgraded to Neutral from Sell by Citi. B/H/S: 3/2/0. Citi is encouraged by the results coming from deep drilling at Gwalia and awaits the outcome of work on the expansion and mass extraction. The broker believes the slurry-pumping strategy could be a game changing technology for deep gold mines, if it works. The study is due in the March quarter 2019. Citi notes the shares have pulled back around 20% in the past three months, while the falling Australian dollar and commodity price outlook have lifted FY19 earnings expectations. The broker upgrades to Neutral from Sell. Target is raised to $4.30 from $3.70.

SANTOS LIMITED (STO) was upgraded to Neutral from Sell by UBS. B/H/S: 1/3/1. Sales volumes in the September quarter were ahead of UBS estimates. The company has lifted the lower end of its production and sales guidance for 2018 and reduced 2018 capital expenditure by $50 million. UBS observes the results are starting to demonstrate the positive impact of increased drilling in the Cooper Basin. Overall, September quarter production was slightly below UBS estimates because of the timing of asset sales to Ophir Energy. Target is raised to $7.55 from $5.70.

SUPER RETAIL GROUP LIMITED (SUL) was upgraded to Add from Hold by Morgans. B/H/S: 3/4/1. Morgans expects 10.9% growth in operating earnings in FY19, which requires around 5.7% growth from the base business. The broker expects the company to reduce its debt position materially and open the door for an increased pay-out ratio in future. The company’s ability to generate working capital efficiencies will continue to fund investment in stores and refurbishment as well as digital. With around 14% upside to the target, raised to $10.44 from $9.86, and a 5.7% dividend yield, Morgans upgrades to Add from Hold.

TREASURY WINE ESTATES LIMITED (TWE) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 2/4/1. Credit Suisse notes US retail sales data reflects a surprisingly resilient performance. Treasury Wines volumes were down 2% over the month ending October 6 but were a significant improvement and the best performance since the company started selling direct to national accounts. The broker suspects the company’s September promotion in the US has been quite profitable. A respectable performance in North America will help achieve FY19 operating earnings guidance, the broker suggests. Target is steady at $16.45.

WEBJET LIMITED (WEB) was upgraded to Buy from Hold by Ord Minnett .B/H/S: 2/3/0. Ord Minnett has downgraded estimates for earnings per share to reflect lower growth assumptions for the B2B business as well as marginally lower volumes in the B2C division. FY19 and FY20 estimates are downgraded by 7% and 4% respectively. The broker remains confident in the medium-term growth outlook, also believing the decline in the stock has created an opportunity. Target is reduced to $16.80 from $17.46.

In the not-so-good books

MICHAEL HILL INTERNATIONAL LIMITED (MHJ) was downgraded to Sell from Neutral by Citi and to Reduce from Hold by Morgans. B/H/S: 2/0/2. Citi analysts had already expressed their concerns about what precisely was unfolding at the jewellery retailer and Michael Hill’s trading update validated those concerns. The broker has responded by downgrading and cutting the price target to $0.65 from $0.95. Citi analysts have no confidence left that this company’s performance can improve materially in the short term. Morgans makes meaningful downgrades to sales and earnings forecasts. All regions experienced heavy same-store sales declines with Australia down 12.8%, New Zealand -7.6% and Canada -11%. Morgans lowers its target to $0.70 from $1.01.

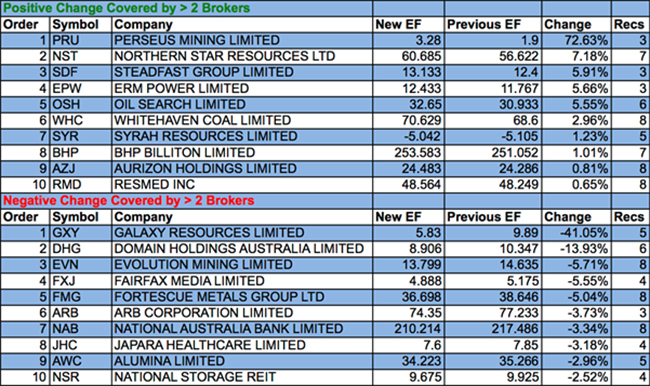

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.