Amidst severe share market turmoil, stockbroking analysts issued more upgrades than downgrades for ASX-listed stocks. No surprise here.

Amcor received two upgrades (both to Buy) and Woodside Petroleum two downgrades (both to Sell). Interestingly, there were no oil and gas companies among the upgrades.

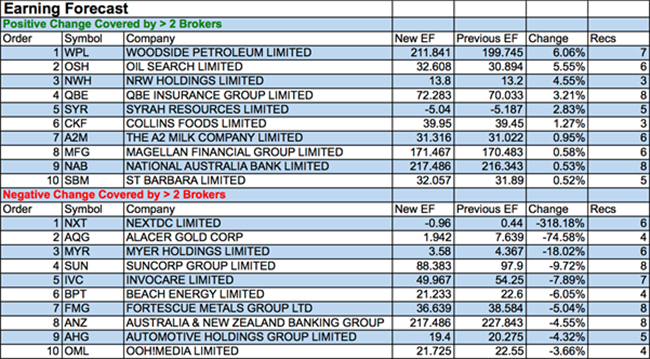

Earnings forecasts changes were considerably more benign on the positive side. Woodside Petroleum earned honours for the week, beating Oil Search, NRW Holdings and QBE Insurance. But there was a lot more action last week on the negative side, with significant cuts coming towards NextDC, Alacer Gold, Myer Holdings, Suncorp, invoCare, and Beach Energy and Fortescue Metals.

In the good books

AMCOR LIMITED (AMC) was upgraded to Buy from Neutral by Citi and to Outperform from Neutral by Credit Suisse. B/H/S: 6/1/0. Citi believes the risk/reward has turned favourable for Amcor. Rising bond yields may weigh on the macro outlook but higher oil prices have not affected the company’s raw material outlook, with only a modest impact expected in the first half. The Bemis merger is on track, with Citi noting immediate capacity for further acquisitions or share buybacks. Target is raised to $15.00 from $14.50. Credit Suisse expects the Bemis merger to go well and, if the company delivers on its synergy objectives in FY20 and FY21, growth should be around 8-9%. Credit Suisse’s target is $14.80.

INVOCARE LIMITED (IVC) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 0/6/1. The company has downgraded expectations for 2018 on the basis of weaker volumes. Historically, Ord Minnett observes seasonal variations in volumes have provided good trading opportunities in the stock. However, given the substantial capital expenditure in train and structural issues facing its UK-listed counterpart, the broker concedes the market is cautious about whether the near-term headwinds are structural. The de-rating of the share price leads the broker to consider the risk/reward equation as more balanced. Target is reduced to $12.00 from $12.30.

JAPARA HEALTHCARE LIMITED (JHC) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 0/3/1. Ord Minnett is confident the final recommendations from the inquiry into aged care will call for improved funding and increased compliance requirements, and this will raise barriers to entry. The broker believes there is valuation appeal in the sector, although there is a challenging period ahead with months of negative media coverage and potential cash flow pressures from a downturn in residential property prices. Target is reduced to $1.25 from $1.50.

RCR TOMLINSON LIMITED (RCR) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 0/4/0. The company has an interim alliance agreement with New Zealand’s City Rail Link regarding project services. The company’s joint venture with Opus International Consultants will develop a proposal that includes the provision of track, overhead line, signalling, control room and building works. Construction is due to commence in June 2019. Ord Minnett observes the prospect of the JV actually being awarded the contract is unclear but assumes the company’s chances are significantly enhanced following the announcement. Target is steady at $1.38.

In the not-so-good books

NAVITAS LIMITED (NVT) was downgraded to Neutral from Outperform by Macquarie. B/H/S: 0/4/0. Navitas has received a bid at $5.50 a share from a private equity-led consortium. Macquarie considers the transaction multiple to be fair. The proposal remains subject to further review. The proposal removes uncertainties regarding the incremental investment that is required to optimise the portfolio and would enable the realisation of value at levels consistent with the broker’s expectations. Macquarie downgrades to Neutral from Outperform, reflecting the move in the share price and the low probability of a competing bid. Target is raised to $5.50 from $4.80.

SENEX ENERGY LIMITED (SXY) was downgraded to Lighten from Accumulate by Ord Minnett. B/H/S: 3/1/0. Ord Minnett updates earnings estimates based on a review of the Brent crude forward price curve and its forecasts are now significantly above the market. The broker believes the sector is fully valued on an average price to net present value basis. Hence, Senex Energy is downgraded to Lighten from Accumulate. Target is raised to $0.47 from $0.46.

WOODSIDE PETROLEUM LIMITED (WPL) was downgraded to Underperform from Neutral by Macquarie and to Lighten from Hold by Ord Minnett. B/H/S: 3/1/2. Macquarie believes positive revenue momentum in the oil sector was recorded over the September quarter, as oil prices increased 7%. Despite speculation regarding a decision on a Browse tolling fee, Macquarie continues to believe the high cost will mean the project is unlikely to proceed. Target is reduced to $34.70 from $35.40. Ord Minnett updates earnings estimates based on a review of the Brent crude forward price curve and its forecasts are now significantly above the market. The broker believes the sector is fully valued on an average price to net present value basis.. Target is raised to $37.00 from $34.50.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.