The sharp recovery in (in particular) cyclicals and other laggards in the Australian share market has triggered a flurry in rating changes among stockbroking analysts. For the week ending Friday, 11th May 2018, FNArena counted twelve upgrades for individual ASX-listed stocks versus 19 downgrades.

Also obvious: most companies releasing financial results and quarterly market updates this month are triggering negative responses. If it weren’t for exceptions such as Macquarie Group, Xero and REA Group, and for positive momentum behind miners and energy producers, underlying momentum would be a lot weaker.

Local reporting season continues this week, alongside investor days, AGMs, quarterly updates and major banks going ex-dividend.

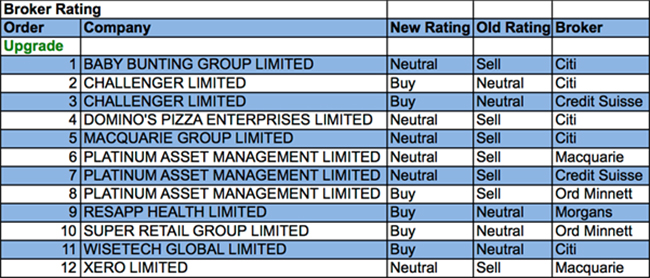

In the good books

BABY BUNTING GROUP LIMITED (BBN) was upgraded to Neutral from Sell by Citi. B/H/S: 2/2/0. Citi believes its sell thesis surrounding disruption from competitor closures has played out quicker than expected. The broker upgrades to Neutral/High Risk from Sell, envisaging the risks over the next 12 months as evenly balanced. Operating momentum is expected to improve following the latest round of competitor closures. The broker trims FY18 forecasts to reflect downgraded guidance but upgrades FY19 forecasts to reflect market share gains, and believes the company is well-placed to be the winner in the fall-out from competitors. Target is raised to $1.50 from $1.20

.

DOMINO’S PIZZA ENTERPRISES LIMITED (DMP) was upgraded to Neutral from Sell by Citi. B/H/S: 2/5/1. Citi analysts now believe the specific risks surrounding Domino’s Pizza have been priced in, suggesting limited downside, apart from day-to-day volatility. Interestingly, the analysts do not think the company will achieve its 20% growth target for the running year, but forecast 16% instead, with the added comment this is in line with market consensus. The analysts are anticipating a tighter trading range. Price target $44.60.

SUPER RETAIL GROUP LIMITED (SUL) was upgraded to Buy from Hold by Ord Minnett. B/H/S: 4/4/0. Ord Minnett considers the Australian consumer outlook robust because of employment growth, while the launch of Amazon has been underwhelming. Despite the company’s recent share price performance, the broker considers the risk/reward ratio for investors is attractive, even if only the automotive and capital targets are met. The broker upgrades to Buy from Hold and raises the target to $9 from $8.

WISETECH GLOBAL LIMITED (WTC) was upgraded to Buy from Neutral by Citi. B/H/S: 2/1/1. Following the company’s inaugural investor briefing, Citi upgrades to Buy from Neutral and increases revenue forecasts for FY19-20 by 3-10%. The target jumps to $14.12 from $9.51 because of the expansion in FY19 peer multiples and an increase to the stock’s premium, reflecting greater confidence in the company’s organic growth trajectory. Growth is expected to be led by new product developments and the ability to integrate acquisitions over the medium term.

XERO LIMITED (XRO) was upgraded to Neutral from Underperform by Macquarie. B/H/S: 1/3/1. The company reported a net loss of NZ$27.8 million, better than expected. Macquarie observes FY18 was a transition year as the company reported its first positive EBITDA and operating cash flow. The improvement reflects ongoing growth in the subscriber base. Earnings are beginning to highlight the significant operating leverage within the business and Macquarie upgrades assumptions. Rating is raised to Neutral from Underperform. Target is increased to $37.00 from $27.19.

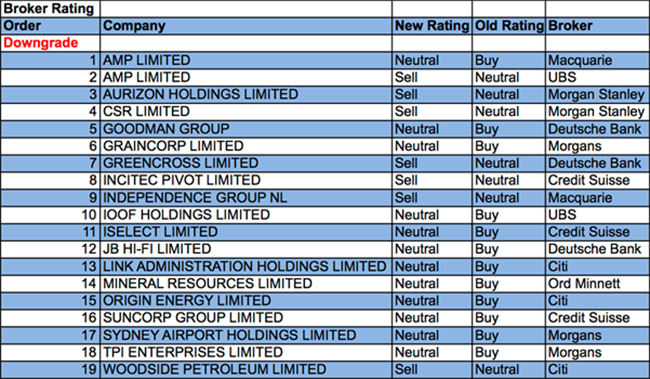

In the not-so-good books

AURIZON HOLDINGS LIMITED (AZJ) was downgraded to Underweight from Equal-weight by Morgan Stanley. B/H/S: 2/2/3. Morgan Stanley believes the company’s activist regulatory campaign adds uncertainty and reduces the opportunity for cost reductions and top-line growth. The broker suspects the market may not be fully pricing in the low margin for safety as the campaign will be long, public and drawn out and the Queensland intermodal sale may not proceed. Target is reduced to $4.00 from $4.88. Industry view: Cautious.

CSR LIMITED (CSR) was downgraded to Underweight from Equal-weight by Morgan Stanley. B/H/S: 1/3/2. FY18 results were broadly in line with Morgan Stanley. The main negative came from energy cost pressures in aluminium. The broker suggests earnings have likely peaked and downgrades to Underweight from Equal-weight. Target is reduced to $4.75 from $5.00. The inevitable decline in overall Australian housing construction suggests that FY18 is almost certainly to be the peak and the broker suggests a one-off spike in property sales may be the only thing that can change this scenario. Industry view: Cautious.

GOODMAN GROUP (GMG) was downgraded to Hold from Buy by Deutsche Bank. B/H/S: 3/4/0. Guidance for FY18 has been reaffirmed at 46.5c in earnings per share, up 8%. Although Deutsche Bank expects ongoing strength in the e-commerce sector will drive demand for industrial assets, the share price has increased 14% since it previously upgraded to Buy. Hence, now the stock is trading ahead of the target of $8.80 the rating is downgraded to Hold.

GREENCROSS LIMITED (GXL) was downgraded to Sell from Hold by Deutsche Bank. B/H/S: 0/3/1. The company’s update highlighted a sudden deterioration in the veterinary business, a segment which Deutsche Bank had expected to be more stable. Revenue has been affected by a reduction in visits to stand-alone clinics. The broker believes the earnings trajectory bodes poorly for FY19, especially given the competitive intensity in the industry and the large debt the group is carrying. Rating is downgraded to Sell from Hold. Target is $3.70.

IOOF HOLDINGS LIMITED (IFL) was downgraded to Neutral from Buy by UBS. B/H/S: 4/1/0. The business has not yet appeared in front of the Royal Commission and, therefore, UBS observes, sidestepped the direct fall-out affecting other vertically integrated operators. Still, as an almost pure play in the sector, the broker believes cost and flow implications are more pronounced. The business would be most impacted under a scenario where advice and platforms are structurally separated, and UBS ascribes a notional 20% probability to this. The broker downgrades to Neutral from Buy, given the value constraints until the risk dissipates. Target is reduced to $10.00 from $11.50.

INDEPENDENCE GROUP NL (IGO) was downgraded to Underperform from Neutral by Macquarie. B/H/S: 0/4/2. March quarter production was weak, Macquarie observes. Given the increased risk of misses to production and cost guidance the broker downgrades to Underperform from Neutral. Incorporating the weaker result drives a -10% reduction to earnings estimates for FY19 and FY20. Target is reduced to $4.60 from $4.90.

INCITEC PIVOT LIMITED (IPL) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 3/3/1. Headwinds in Australian explosives are increasingly apparent, and there is some uncertainty around capital expenditure and costs from an extended maintenance cycle, Credit Suisse observes. In the absence of a significantly improved outlook for fertiliser prices, the broker suggests earnings are likely to be relatively flat for the next two years. Rating is downgraded to Underperform from Neutral. Target is reduced to $3.39 from $3.85.

LINK ADMINISTRATION HOLDINGS LIMITED (LNK) was downgraded to Neutral from Buy by Citi. B/H/S: 2/4/0. It’s the “material uncertainty” that has triggered the downgrade to Neutral from Buy, with Citi analysts adding the loss of the CareSuper contract, while small in impact, is not helping sentiment either. The proposed measures in the Federal Budget are now overshadowing the positive narrative, and Citi analysts have decided to slightly reduce their forecasts, and cut their target to $8.10 from $9.85, on the uncertainty that will linger for longer.

MINERAL RESOURCES LIMITED (MIN) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 2/2/0. The company intends to sell 49% of Wodgina as part of an offtake and partnering process. Ord Minnett values Wodgina at $2.4 billion on a 100% basis. Wodgina accounts for $12.60 a share or 65% of valuation. The broker believes Wodgina can largely self-fund its vertical integration, so Mineral Resources will need to consider how much of the sale proceeds should stay with the joint venture, how much should be spent on other businesses and how much returned to shareholders. Ord Minnett downgrades to Hold from Accumulate. Target is $19.50.

ORIGIN ENERGY LIMITED (ORG) was downgraded to Neutral from Buy by Citi. B/H/S: 5/3/0. Citi transfers coverage of Australian energy to another analyst. In the large cap stocks the broker’s top pick is Caltex (CTX) followed by Origin Energy, which is downgraded to Neutral from Buy. The broker raises the target to $10.13 from $10.06.

SUNCORP GROUP LIMITED (SUN) was downgrades to Neutral from Outperform by Credit Suisse. B/H/S: 5/2/1. The share price has risen 10% since mid February and Credit Suisse downgrades the rating back to Neutral from Outperform. Target is unchanged at $14.50. The broker remains confident the business will deliver a significant turnaround in underlying insurance margin in the second half and supports the business improvement program. However, Suncorp has suffered from volume loss recently and ongoing premium rate increases may mean this continues and reduces some of the potential earnings upside.

SYDNEY AIRPORT HOLDINGS LIMITED (SYD) was downgraded to Hold from Add by Morgans. B/H/S: 5/2/0. The company has outlined its growth opportunities at the investor briefing. After the NSW and federal elections, the business intends to lobby for an easing of regulatory restrictions related to aircraft movement caps and regional flights. Morgans makes reductions to long-term forecasts and assumes a slowing of distribution growth beyond FY18. The broker downgrades to Hold from Add because of the recent strength in the share price. Target is reduced to $7.12 from $7.45.

WOODSIDE PETROLEUM LIMITED (WPL) was downgraded to Sell from Neutral by Citi. B/H/S: 2/4/2. Citi transfers coverage of its Australian energy sector to another analyst. The broker’s pecking order now places LNG-exposed names such as Woodside and Oil Search (OSH) as its least preferred. Target is raised to $28.68 from $28.34.

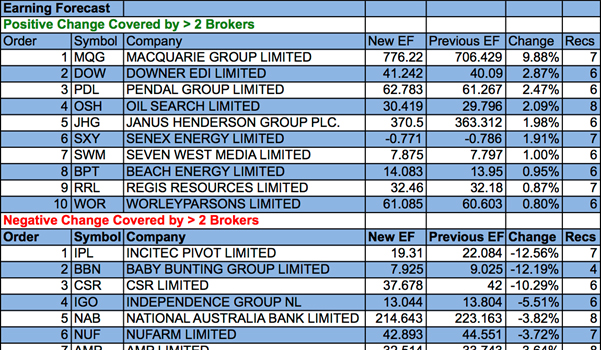

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.