The direct correlation between share price movements and stockbroker ratings for ASX-listed stocks remained alive and well last week. As share market indices swung higher, the number of stocks receiving downgrades multiplied.

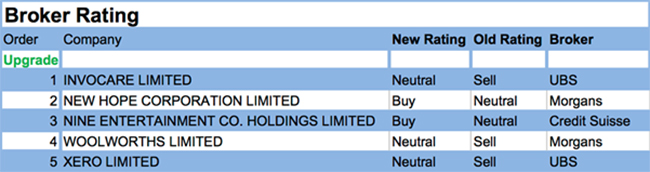

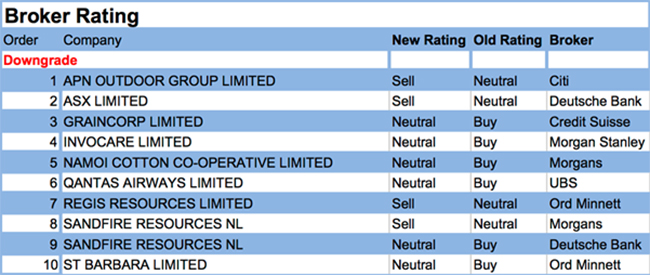

For the week ending Friday, 4th May 2018, FNArena registered ten downgrades and five upgrades. Equally noteworthy: only two of the upgrades moved ratings to Buy, while four of the downgrades moved to Sell.

The two stocks receiving upgrades to Buy during the week are New Hope (coal) and Nine Entertainment (media). Stocks downgraded to Sell include APN Outdoor, ASX Ltd, and Regis Resources.

The banking reporting season is proving yet another sad affair, with estimates and price targets in general taking another step backwards post results. Share prices have not followed suit, however, as share price weakness had preceded results reports. Macquarie, not a real “bank”, once again proved that trading on a sector premium does not mean the shares are “expensive” by any means.

Domestic reporting season continues throughout the remainder of the month, with numerous High PE stocks complementing banks, wealth managers and cyclicals.

In the good books

INVOCARE LIMITED (IVC) was upgraded to Neutral from Sell by UBS. B/H/S: 0/4/2. The broker believes InvoCare’s ‘Protect & Grow’ strategy offers long-term opportunities but in the short term, the negative impact of closures is greater than expected. The strategy is a good one but the new growth profile is yet to be proven and will require more capital. The broker is thus cautious but given share price weakness upgrades to Neutral. Target falls to $12.65 from $13.65.

See also IVC downgrade.

NINE ENTERTAINMENT CO. HOLDINGS LIMITED (NEC) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 3/2/1. Credit Suisse raises long-term forecasts to reflect a more efficient allocation of programming resources following the company’s capture of the Australian Open tennis rights and the relinquishing of its long-held domestic cricket rights. The broker increases FY18 TV advertising market growth forecasts to 2.0% from 1.2%. Rating is upgraded back to Outperform from Neutral as the broker now believes the business remains in an upgrade cycle. Target is raised to $2.60 from $2.35.

NEW HOPE CORPORATION LIMITED (NHC) was upgraded to Add from Hold by Morgans. B/H/S: 2/1/0. The Queensland Supreme Court has set aside the Land Court decision on Acland stage 3 and referred it for further consideration. Morgans considers this a significant win for the company in what has been a 10-year approvals process. Despite this news the broker notes the market ascribes no value to Acland 3, implying a free option on a potential positive outcome for investors. Rating is upgraded to Add from Hold and the target to $2.36 from $2.23.

WOOLWORTHS LIMITED (WOW) was upgraded to Hold from Reduce by Morgans. B/H/S: 4/2/2. March quarter sales were slightly better than Morgans expected. Big W was relatively weak, affected by the timing of New Year’s Day and the shift of the school holidays in NSW. Morgans rolls forward its model for FY19 and increases the target to $25.87 from $22.62. Given a forecast 12-month total shareholder return of -4% the broker upgrades the rating to Hold from Reduce. Morgans retains a preference for Wesfarmers (WES).

In the not-so-good books

APN OUTDOOR GROUP LIMITED (APO) was downgraded to Sell from Neutral by Citi. B/H/S: 2/2/1. The broker has used a sector update to pull back its rating to Sell from Neutral. The analysts remain confident strong growth for the outdoor media space is set to continue, but for APN Outdoor in particular they are concerned about costs and margin compression. Target price tumbles to $4.50. Citi prefers oOh!media (OML) in the sector. Management at APN Outdoor already admitted they will have to make additional investments to catch up with the competition. The analysts suggest more needs to be done.

ASX LIMITED (ASX) was downgraded to Sell from Hold by Deutsche Bank. B/H/S: 0/3/5. The March quarter trading update points to a strong FY18 result, although the company does expect fourth quarter expenses will step higher. Driven by strong results so far this year, the stock has reached record levels and Deutsche Bank believes the valuation is stretched. Rating is downgraded to Sell from Hold. Target is $55.90.

INVOCARE LIMITED (IVC) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 0/4/2. The disruption to the business from the capital expenditure program has been greater than expected and Morgan Stanley reduces forecasts for earnings per share by -6% for 2018-20.The broker’s main concern is that 43% of the volume decline in the March quarter could not be attributed to intentional one-off closures. Market share loss appears to have accelerated, excluding the impact of refurbishing initiatives. Target is reduced to $12.60 from $15.70. In-Line industry view.

See also IVC upgrade.

QANTAS AIRWAYS LIMITED (QAN) was downgraded to Neutral from Buy by UBS. B/H/S: 3/2/1. Qantas’ March quarter revenue performance beat expectations and management expects momentum to continue into the June Q, albeit at a more moderate pace. UBS has lifted earnings forecasts. The increase is offset by factoring in higher oil prices, although Qantas’ 70% hedge tempers the impact. A greater impact is nevertheless priced into latter years. UBS has lifted its target to $6.50 from $6.35 but with the share price already strong, the broker pulls back to Neutral.

REGIS RESOURCES LIMITED (RRL) Downgrade to Lighten from Hold by Ord Minnett. B/H/S: 1/1/4. Ord Minnett struggles to justify the valuation as, despite Regis Resources being a strong dividend-paying gold company, 20% of valuation is attributed to McPhillamys and preliminary environmental assessment submissions have recently been delayed. Target is raised to $4.20 from $4.10.

ST BARBARA LIMITED (SBM) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 1/3/1. Ord Minnett notes the gold sector continues to re-rate after the March quarter update and downgrades to Hold from Accumulate on valuation. St Barbara has been one of the broker’s preferences but, after a recent strong performance, more details are awaited from the Gwalia GMX project before becoming more positive. Target is raised to $4.50 from $4.30.

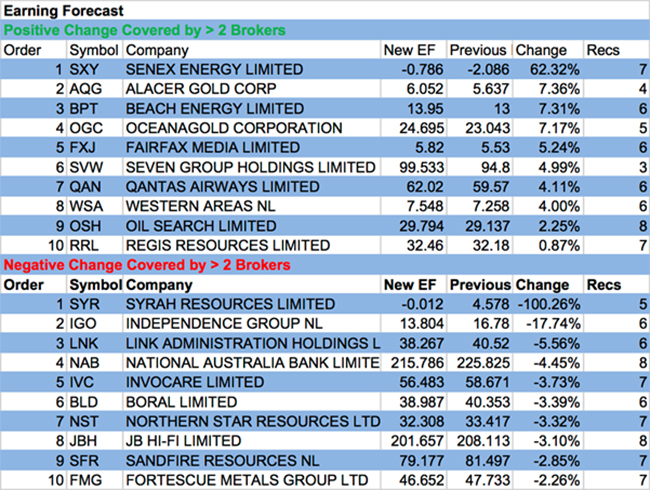

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.