Ahead of reporting season, good sense at long last prevailed on the local stock market, with the banks back in favour. And in what looks like an oddity, we’ve put together three positive trading sessions in a row.

I’m now only hoping that news out of the US overnight doesn’t make it hard for our market to make it four in a row!

The S&P/ASX 200 index put on 31 points (or 0.5%) to end the week at 6121.40 – a 1.2% gain.

Energy has been another stellar performer and Charlie Aitken’s pick, Woodside, climbed up 2.1% on Friday, after a survey of oil producers surprisingly showed that the OPEC and non-OPEC producers are sticking to their quotas!

My Sky News colleague Julia Lee from Bell Direct has a noteworthy reason for the action this week. “This is all about positioning for the late stages of the bull market,” said Julia. “The stocks that do well in this environment are commodities, oil and gas, and growth stocks.”

While in the commodity space, I’ve fielded many questions about the outlook for commodities. I can’t see a scary fall and I suspect they’ll creep higher but Goldman Sachs is more excited on the subject.

“We maintain our overweight recommendation in commodities as the environment for investing in commodities is the best since 2004-2008,” its Commodity Watch report revealed this week.

Fairfax says: “Goldman lifted its 12-month target on copper to $US8,000 a tonne, from $US7,050 previously. It raised its six-month target on Brent to $US82.50 a barrel from $US62. As for iron ore, Goldman increased its three-month target to $US85 a tonne from $US55; its three-month target for met coal is now $US220 a tonne from $US165.”

There’s no clear reason for the banks’ share price turnaround but it has coincided with CBA announcing that its new CEO would be its retail boss, Matt Comyn. While my media colleagues bagged the bank for an internal appointment, given the banks bad brand-clobbering run lately, market players bought the bank on the news!

Meanwhile, the bond proxy stocks – REITS and utilities – are struggling as interest rates rising talk overseas has made these interest-rate sensitive stocks less appealing.

Yep, and interest rates are now really back in focus with bond market yields in the US spiking on a better-than-expected January jobs number – 200,000 showed up when experts tipped 180,000.

Ahead of the close, the major stock market indexes were on track for the worst week in two years! Not helping the Dow was a 5.4% slide in Exxon Mobil. And just when energy was a great story this week, as I mentioned above, some doubts about its longevity have crept in, though it smells more of profit-taking.

But the big story is that damn bond market. On Monday’s TV show on Sky, I had two bond market experts – Anne Anderson from UBS and Steve Goldman from Kapstream Janus Henderson – who warned that yields were on the rise but they weren’t spooked by what they expect this year. In fact, both were comfortable with their exposure to stocks, personally!

The big market-shifting news out of these job numbers was the annualised wages rise of 2.9%. The real smell of real inflation ultimately on the way, because of a good wage rise, sent yields up and stocks down. Ahead of the close, the Dow was down over 500 points.

I warned about volatility and I fingered the bond market as the ultimate problem child for stocks but I hoped we could get a good local reporting season out of the way to see our stock market ride higher before the inevitable US pullback happens.

The only positive take out of all this is that any sell off will be another buying opportunity because the fat lady in this bull market show has only just got out of the cab and is entering her dressing room! There will be a number of exhilarating as well as dramatic moments ahead over the next two years before she treads the boards for her parting song.

That said, it’s timely to remind you, as Mike Baele, managing director at U.S. Bank Wealth Management said to CNBC after the jobs data: “The key for the market today is rising interest rates.” He then pointed out: “The old adage is: ‘Bull markets don’t die of old age, they are killed by higher interest rates.’ That looms large.”

I clearly agree but time is still on the bulls’ side, with the US reporting season revealing that 78% of the companies so far have beaten profit expectations, while 80% have clobbered sales forecasts. And that’s after about half of the S&P500 companies have reported.

Experts think the next reporting season will be even better!

What I liked

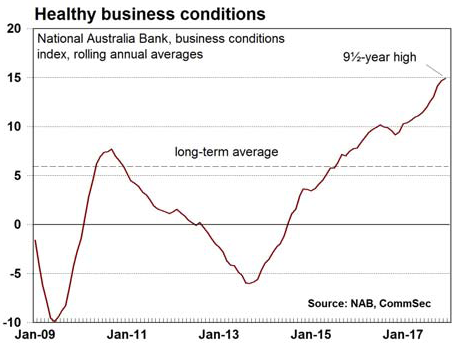

- The NAB business conditions index rose from +13.0 points to +13.2 points in December. The business confidence index rose from to +6.8 points to +11.1 points. That’s huge!

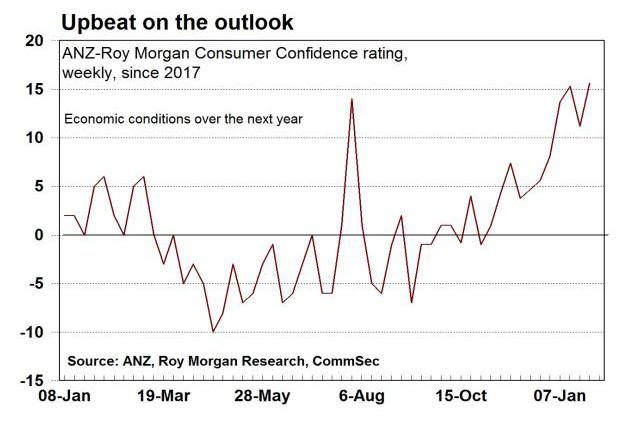

- The weekly ANZ/Roy Morgan consumer confidence rating rose by 1.3% last week. The short-term outlook for the economy is the brightest since April 2013.

- The Producer Price Index (PPI), or final stage prices, rose by 0.6% in the December quarter to stand 1.7% higher than a year ago. Of final stage prices, domestic goods prices rose by 0.5% (1.9% on an annual basis), while import goods prices rose by 0.6% in the quarter (0.5% annual).

- The CBA/Markit Manufacturing index eased to 55.4 in January from 57.1 in December.

- The Australian Industry Group (AiG) manufacturing index increased to 58.7 in January from 56.2 in December. Readings above 50.0 indicate that the sector is expanding.

- The CoreLogic Home Value Index of capital city home prices fell by 0.5% in January to stand 3.2% higher over the year. The national home price index fell by 0.3% in January to be up 3.2% over the year. It was the smallest annual growth in national prices in 16 months, which is what the RBA was looking for to cool down a hot property market.

- The Consumer Price Index rose by 0.6% in the December quarter, below expectations for a lift of 0.7%. The annual rate of inflation rose from 1.8% to 1.9%. That’s only just likeable. I’d rather slightly higher inflation but it’s coming this year.

- The ISM manufacturing index in the US eased from 59.3 to 59.1 in January (forecast 58.8). The prices paid index hit 6½ year highs.

- Construction spending in the US rose by 0.7% in December (forecast +0.4%).

- The Fed left the target rate for the federal funds at 1.25% – 1.50%.

- The ADP report showed that private payrolls rose by 234,000 in January (forecast +185,000).

- US consumer confidence rose from 123.1 to 125.4 in January.

- US personal income rose by 0.4% in December (forecast +0.3%), with spending up 0.4% as expected.

- The National Bureau of Statistics manufacturing purchasing managers’ index edged down to 51.3 in December from 51.6 in November. But the services sector purchasing managers’ index increased to 55.3 from 55.0. Any reading above 50 signifies expansion or growth of activity.

What I didn’t like

- The S&P 500 was set to have its worst week since February 2016 but I have to admit a pullback would be healthy, so I’m not that annoyed by the fact that the US economy is proving the doubters, who complained that wages would never rise significantly, wrong!

- Rising bond yields in the US hit stocks – it was an overreaction but the Fed has to be careful with its rate rises this year.

- Approvals by local councils to build new homes declined by 20% in December, after increasing by an upwardly revised 12.6% in November (previously 11.7%). It was the weakest monthly outcome in nearly 5½ years. In trend terms, approvals declined by 1.7% – the third consecutive monthly decline.

- Private sector credit (effectively outstanding loans) rose by 0.3% in December after a 0.4% rise in November. Annual credit growth fell from 5.2% to a 3½-year low of 4.8%. It’s what the RBA wanted – slower credit creation for homes – but we have to watch the slowdown.

Complaints

I’ve received numerous emails this week wondering what has happened to Switzer on the Sky News Business Channel. The new owner, News Corp, has changed the format, so for now I’m on Monday at 7.30pm for half an hour. As I don’t run the operation, would you direct any feedback you have to Sky?

The Week in Review:

- Wall Street’s put on a fantastic performance of late, but you have to ask, is this just euphoric madness? And how long can it last? I discuss a stock from the smartest hedge fund on the planet!

- Unlisted trusts typically pay higher yields than listed trusts and are smaller in size. Find out which latest offering Paul Rickard is keeping an eye on.

- Find out why this UK bank remains one of Charlie Aitken’s top picks for international exposure.

- If you think the new reporting requirements for SMSFs are confusing, you’re not alone. Graeme Colley offers a guide on when and what to report to avoid losing out.

- With the kids back in the classroom this week, Tony Featherstone looked at four higher-quality small and mid-cap education stocks.

- In Buy, Hold, Sell- what the brokers say, Alumina, Boral and Orica are all upgraded while St Barbara is downgraded.

- And in the second Buy, Hold, Sell – what the brokers say, Super Retail Group is downgraded while two major banks are featured ahead of reporting season.

- In this week’s Hot Stocks is a popular soft drink company and a major retail company. Find out which ones!

- Plus, Paul Rickard answers your Questions of the Week about Domain Holdings, unlisted property funds and Australia’s growing debt.

Top Stocks – how they fared

What moved the market?

- Inflation edged up 0.6% over the quarter and 1.9% over the year, slightly below the RBA’s target band of 2-3%.

- US markets: 10-year Treasury yield rises to fresh four-year high at just under 2.8%

- S. equities pulled back on Thursday as investors worried about rising interest rates.

- Thursday marked the busiest day of the U.S. earnings season, with about 70 companies reporting. Alphabet, Amazon, Apple, Visa and Mattel are among the companies scheduled to report. UPS, AutoNation and Blackstone are among the companies that reported before the bell.

- Bitcoin just keeps falling and has plunged to 13% sparking a $133 billion January loss. Where is this cryptocurrency heading!?

Calls of the week:

“If you don’t make a fortune in the next ten years, it’s your own fault” – 19 year old bitcoin millionaire Erik Finman

Commonwealth Bank appointed their new CEO, Matt Comyn

Tony Featherstone says that these 4 education stocks will school you.

The Week Ahead:

Australia

- Monday February 5 – New vehicle sales (January)

- Monday February 5 – Services sector surveys (January)

- Monday February 5 – ANZ job advertisements index (January)

- Tuesday February 6 – Reserve Bank Board meeting

- Tuesday February 6 – Retail trade (December & December quarter)

- Tuesday February 6 – International trade (December)

- Wednesday February 7 – AiGroup Performance of Construction index (Jan)

- Thursday February 8 – Speech by RBA Governor Philip Lowe

- Friday February 9 – Housing finance (December)

- Friday February 9 – RBA Statement on Monetary Policy

Overseas

- Monday February 5 – US ISM non-manufacturing index (January)

- Monday February 5 – China Caixin Services purchasing managers (Jan)

- Tuesday February 6– US trade balance (December)

- Tuesday February 6 – US JOLTS job openings survey (December)

- Wednesday February 7 – US Consumer credit (December)

- Thursday February 8 – China trade balance (January)

- Friday February 9 – US Wholesale inventories and sales (December)

- Friday February 9 – China consumer price index (January)

- Friday February 9 – China producer price index (January)

Food for thought:

“The most valuable commodity I know of is information”. – Gordon Gekko

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Charts of the week: Source: ANZ, CommSec, Roy Morgan Research

Source: ANZ, CommSec, Roy Morgan Research

Source: CommSec, NAB

Source: CommSec, NAB

Top 5 most clicked:

- CYBG PLC: continues to offer value, growth and growing yield – Charlie Aitken

- Buy, hold, sell – CBA and Westpac – Staff reporter

- 4 education stocks to school you – Tony Featherstone

- Professional’s Pick – Speedcast – Michael Wayne

- Take this Emerging Markets Stocks Tip from the smartest hedge fund on the planet! – Peter Switzer

Recent Switzer Super Reports:

Monday 29th January – Back to business

Thursday 1st February – Get schooled on stocks

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.