We banked on banks this week ahead of their reporting season, with rising interest rates set to help their bottom lines. In truth, the bank-created higher rates were at the behest of APRA but they might have followed the script more than they needed to!

The S&P/ASX 200 Index went up 1.2% for the week but the market remains gun shy when it comes to the 6000 level, with the overall market measurer ending the week at 5924.

And with Donald Trump still providing a reducing modicum of market excitement by uttering the words “tax reform”, and with the US economy not yet showing it’s actually going gangbusters, a lot of smart players are being won over to stocks because of the earnings outlook.

This is a really solid sign for the market.

“Although global events have buffeted our market around week to week, underlying all that market earnings are growing pretty strongly for fiscal 17,” said Tony Brennan, head of equity market strategy at Citi and a very bright former student of mine. “The continuation of these earnings will see the market over 6000 points I would think,” said Brennan. (SMH)

Meanwhile, those gutsy enough to buy gold had a bad week, as North Korean fears and good economic tidings out of Europe suggested that the panic play is going off the boil.

In the US, stocks were up 1% but it might have been more if economic growth had come in stronger. Those whingeing about Australia should note that US growth was only 0.7%, compared to a Reuters consensus call of 1.2%. Fortunately, however, earnings’ stories remain very positive.

“It seems like the earnings and the reduced anxiety over the policy agenda are driving the markets this week,” Michael Arone, chief investment strategist at State Street Global Advisors told CNBC.

That said, even with the historical softness of US growth in the first and coldest quarter of the year for weather, that growth number was not stellar, given what business and consumer confidence readings have been saying since Donald T became the main man.

Back home and the focus is now zooming in on the Budget, which is revealed on May 9. And in a step of overdue wisdom, the Treasurer has introduced the new narrative about good debt – infrastructure-type spending – and bad debt, which is borrowing to pay for social policies. Clearly, education and welfare policies aren’t bad policies but, if they rest on borrowing, the question becomes: how do you pay for it?

How the Government negotiates between these thorny issues and the Senate will be the ultimate test of the Budget.

It goes without saying that Malcolm Turnbull, Scott Morrison and the economy need a good, accepted Budget or there will be both economic, market and political consequences.

What I liked

- One measure of incomes in Australia, the terms of trade, (or ratio of export prices to import prices) has posted the biggest back-to-back gain in almost seven years. But, notably, it is also the second biggest six-monthly gain in 44 years and the third biggest increase ever recorded. If export prices are outpacing the price of imports, this indicates a broad-based lift to incomes in Australia. The lift in export prices (especially iron ore and coal) also serves to benefit the bottom line of the government accounts. (CommSec)

- The Consumer Price Index rose by 0.5% in the March quarter, below expectations for a lift of 0.6%. The annual rate of inflation rose from 1.5% to 2.1% and the RBA wants it in the 2-3% band.

- The US tax reform package, with corporate tax coming down from 35% to 15%, if Donnie gets his way. And the one-time tax on trillions held by US companies domiciled overseas, which might make our taxing authorities get serious about collecting tax from these leading international companies. No border adjustment tax was another good sign.

- The French election result and the market reaction. Europe is becoming the flavor of the year for fund managers.

- US earnings continue to surprise on the upside. We have now seen 54% of companies report, with 81% beating on earnings and 65% beating on sales. Earnings are up 12% year-on-year and on track for the fourth quarterly gain to new record highs.

- In April, European consumer confidence readings in the Eurozone pushed up to the highest levels since before the GFC.

- Eurozone inflation jumped to 1.9% in April, up from 1.5% in March. Inflation is now at the highest level since 2013.

What I didn’t like

- Durable goods orders in the US rose by 0.7% in March (forecast +1.2%).

- US consumer confidence fell from a 16-year high of 124.9 in March to 120.3 in April (forecast 122.5) but it still is at elevated levels.

- This damn Michael Corleone flu that I can’t shake. The more I try to get away from it, “the more it drags me back in!” Dr. Ross Walker says it’s influenza A and it’s at times like this that I wish I was a B-grade player!

The week in review

- What is a quality stock and how do you find them? This week I outlined some ‘disciplines’ to follow, plus stocks to watch too.

- Since Paul Rickard last visited Telstra and asked whether it’s a buy, there has been one major change: TPG’s plans for a new mobile network. He shared whether his view on the stock has changed.

- James Dunn revealed his top four stocks that have a track record for business growth.

- Retail is the second largest employer in Australia, but the sector also faces challenges. Roger Montgomery shared three retail stocks worth watching.

- The brokers upgraded NAB and Rio Tinto this week, while ResMed copped a downgrade.

- An upsurge in online ordering has fuelled a takeaway eating trend. Tony Featherstone discussed some companies that could benefit.

- Charlie Aitken explained why he thinks we’re in a passive bubble, and why it’s providing opportunities for active stock pickers.

- Graeme Colley explored a question around the capital gains tax cost base reset: Is it the right thing to do?

- And in our second broker report, Bendigo and Adelaide Bank were among the upgrades while AGL was downgraded.

Top stocks – how they fared

What moved the market?

- Centrist Emmanuel Macron taking out the first round of the French election.

- Solid US earnings data.

- The details of Donald Trump’s tax plan.

- And slightly weaker-than-expected inflation numbers (0.5% in the March quarter compared to an expected 0.6%) weighed on the Aussie dollar.

Calls of the week

- US President, Donald Trump, revealed his tax plan. It includes reducing the number of personal tax brackets from seven to three (10%, 25% and 35%), and cutting the corporate tax rate from 35% to 15%. Will this push our Treasurer to cut too?

- Deborah Thomas stepped down as CEO of Ardent Leisure after two years in the role. She will become the chief customer officer and chief operating officer for Australasia.

- In this week’s Switzer Super Report, Charlie Aitken said a massive passive bubble is providing “tremendous contrarian opportunities” for active investors. Read it here.

- And PM Malcolm Turnbull made the call to intervene in the energy market by imposing export restrictions on gas producers.

The week ahead

Australia

- Monday May 1 – AiG Performance of Manufacturing Index

- Monday May 1 – CoreLogic House Price Index (April)

- Tuesday May 2 – Weekly consumer confidence

- Tuesday May 2 – Reserve Bank Board

- Wednesday May 3 – AiG Performance of Services (April)

- Thursday May 4 – Speech by Reserve Bank official

- Thursday May 4 – International Trade (March)

- Friday May 5 – New Home Sales (March)

- Friday May 5 – Statement of Monetary Policy

Overseas

- Sunday April 30 – China Manufacturing purchasing managers

- Monday May 1 – US ISM Manufacturing survey (April)

- Monday May 1 – US Construction spending (March)

- Tuesday May 2 – US Domestic vehicle sales (April)

- Wednesday April 26 – US ADP Employment change (April)

- Wednesday April 26 – US FOMC Rate Decision

- Thursday May 4 – US Trade Balance (March)

- Thursday May 4 – US Factory Orders (March)

- Friday May 5 – US Non-farm Payrolls (April)

Food for thought

- “You are where you are and what you are because of what you believe yourself to be.” – Brian Tracy, motivational speaker and author

Last week’s TV roundup

- Catapult’s products are used by some of the biggest sporting outfits of the world. To discuss the business, CEO Joe Powell joins Super TV.

- Paul Rickard and George Boubouras share the story behind the Switzer Dividend Growth Fund, how it invests, and more (Switzer Investor Strategy Day – Tuesday 4 April, 2017).

- Aitken Investment Management’s Charlie Aitken joins the show to share his views on the stock market, Amazon hype, and why he’s backing China.

- Shane Oliver from AMP Capital discusses the latest inflation number, and where Australia’s economy is headed.

- And to discuss house prices and the best places to buy, Destiny’s Margaret Lomas joins Super TV.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week, one of the biggest movers was Vocus Group with a 1.92 percentage point increase in the amount of its shares sold short to 12.97%. Syrah Resources and Orocobre weren’t far behind, increasing by 1.75 percentage points each.

Source: ASIC

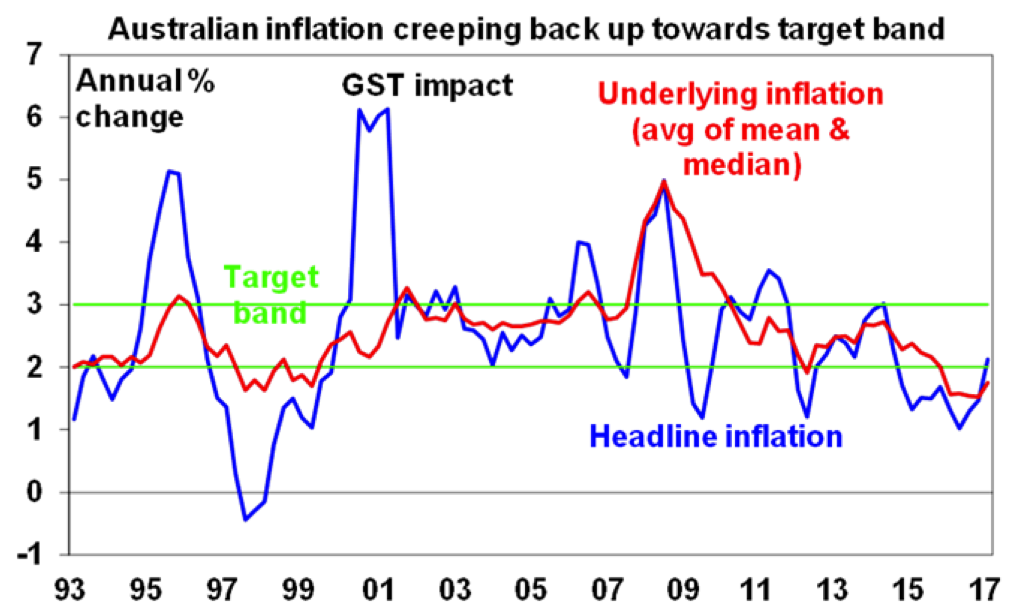

Chart of the week

Source: AMP Capital, ABS.

The main measure of inflation – the Consumer Price Index or CPI – rose 0.5% during the March quarter. Annual growth in prices (blue line) rose from 1.5% to 2.1%. Underlying inflation rose 0.4% in the quarter and 1.8% over the year (red line). The good news is that it’s creeping back towards the RBA’s target band of 2-3% (green lines).

Top five most clicked stories

- Peter Switzer: How to pick quality stocks, and here are a few!

- Paul Rickard: Is Telstra a buy, yet, again?

- James Dunn: 4 top stock picks

- Tony Featherstone: Four ETF strategies

- Roger Montgomery: Shopping for retail stocks – 3 to watch

Recent Switzer Super Reports

- Thursday 27 April 2017: Dining boom

- Monday 24 April 2017: Picking quality stocks

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.