With Grand Final fever in the air in Melbourne and Sydney, you might not have noticed that it was the end of a quarter that promised so much, with a 10-year high being registered. Eventually, however, the impact of the Royal Commission into the finance sector and President Trump’s trade war strategies worked against a sustained rise of stocks here in Australia.

However, it’s working for the Yanks, with the Dow up 9.4% for the three months to the end of September!

“The S&P 500, meanwhile, is set to post its best quarter since fourth quarter 2013, having risen 7.3 percent,” CNBC tells us. “The Nasdaq is also up more than 7 percent, on pace for its best biggest one-quarter gains since first quarter 2017.”

Locally, we were up only 13 points for the week and the quarter and the S&P/ASX 200 index reminds me of that champion racehorse Chautauqua, who was retired yesterday, after again refusing to play ball and jump when the barriers flew open.

This eight-year old gelding won around $8.8 million and beat the world’s best but has decided he’s had a gutful of racing and has virtually said “no more!” Interestingly, he recently did jump in a trial and zoomed home with all his old gusto. That’s why I think our stock market resembles this great horse. There’s a great run left in us as well.

Trump and Hayne have kept us in the barrier but if we can just get out, our market could fly home late this year!

That said, we still have Donald with his tariff plays and a mid-term election to hold stocks back. And then we have to see what the new Morrison Government will come up with post-Hayne and his interim recommendations that were handed in yesterday.

For stock players, the good day for bank stocks yesterday was a nice sign but it might be too early to declare that the bad news for financial stocks is over.

It’s still a ‘wait-and-see’ game for a longer-term investor and I’m prepared to miss a few percentage points of rises before I declare the worst is over for the embattled banks.

The S&P/ASX 200 ended 13 points for the week to close at 6207.6. CBA was up 1.9% on Friday to $71.41, NAB rose 1.76% to $27.81, Westpac put on 1.16% to $27.93 and ANZ jumped 1.4% to $28.18. And that’s despite Commissioner Kenneth Hayne’s scathing assessment of the major players in our financial landscape.

What the Government comes up with to fix the sector is not only going to be huge for bank stock prices and the index, it’s going to be a political football that will be kicked around until election day. If the Libs can hold the seat of Wentworth on October 20, then the big poll should be May 18. That’s going to be a lot of kicking and politicking on the subject, which could be another roadblock for stocks, especially with Bill Shorten’s policies on negative gearing, capital gains tax and tax rebates for self-funded retirees.

Now I think you can see why market experts talk about stock markets climbing a “wall of worry.”

Keeping us positive yesterday was the rising price of oil and this is a pretty good assessment from the AFR: “Brent crude oil prices hit a near four-year high this week, rising on the back of supply concerns in Iran and OPEC’s unwillingness to lift production levels. Energy stocks were the main beneficiary on the market with BHP Billiton the market’s best performer due to its oil exposure, its shares rising 3.1 per cent to $34.63.”

Back to the US stocks overnight and the market is concerned that a trade deal with Canada has not been inked so it can join the Mexico-USA trade pact recently agreed to.

Historically, the fourth quarter in the US is good for stocks and especially December but the next three months have more tariff negotiations and the mid-term elections to cope with. However, I think the next reporting season and what business leaders say about how their operations are being affected by tariffs could determine how good or bad the December quarter will be.

“Unless we see some resolution, trade talks are going to heat up,” said JJ Kinahan, chief market strategist at TD Ameritrade. “But first, we have to go through the earnings season and hear what CEOs have to say on the matter.” (CNBC)

I can’t wait to see our market jump out of that cursed “barrier” but it might have to wait until December, though I am still prepared to buy any significant dips of the index because I don’t think this bull market is dead yet.

What I liked

- The latest job vacancy data from the ABS has shown that there was an increase of 240,900 job vacancies in August 2018, an increase of 3.4% for the quarter. “Over the year, job vacancies increased by 19.3 per cent, with private sector vacancies increasing by 20.3 per cent and public sector vacancies by 9.5 per cent.” (ABS) It’s the strongest annual growth in 7½ years.

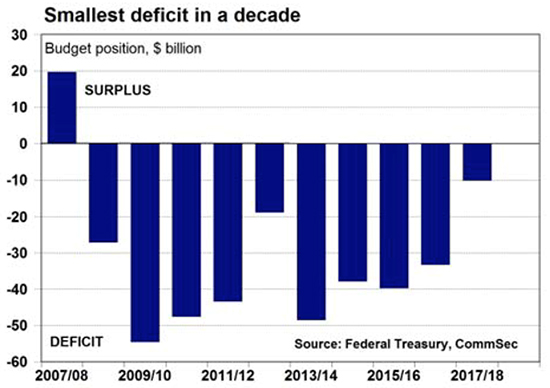

- The 2017-18 budget deficit came in at $10 billion, which is $8 billion less than expected in May and $19 billion less than was tipped on Budget night in May 2017!

- The ANZ-Roy Morgan consumer confidence rating fell 0.7% from 5-week highs to 117.2 in the past week. The index is comfortably above the average of 114.1, held since 2014, and above the longer term average of 113, held since 1990. But importantly, the survey found that the estimate of family finances compared with a year ago stands at 8-month highs.

- Excluding resources, engineering work yet to be done stands at $43.1 billion, below record highs. But outstanding road and railway work were both just below record highs. And electricity generation, transmission and distribution work was at five-year highs.

- With banks held back from lending because of the Royal Commission, this is a positive development: “Loans and advances by non-bank financial intermediaries rose by 10.3% over the year to August, up from 6.2% in July and the strongest annual growth in a decade.” (CommSec)

- Private sector credit (effectively, outstanding loans) rose by 0.5% in August after a 0.4% rise in July. Credit was up 4.5% over the year, up from the 4½-year low of 4.4% in July.

- Foreigners held a record $604.9 billion of Aussie shares in the June quarter, up from $563.6 billion in the March quarter. It reinforces my view that Aussie stocks look attractive.

- Economic growth (GDP) forecasts from the Fed were increased to 3.1% in 2018, up from the previous forecast of 2.8%. The 2019 forecast was lifted to 2.5%, up from the previous projection of 2.4%.

- Comments by Fed Chair Jerome Powell in his press conference, signalling that he didn’t see inflation surprising to the upside: “It’s not in our forecasts” and this sent bond yields lower.

- The Conference Board’s consumer confidence survey in the US rose by 3.7 points to 138.4 (survey:132) in September and that’s an 18-year high!

- The Richmond Fed Manufacturing Index in the US rose by 5 points to 29 (survey:22) in September, which could be tariff-related.

- Eurozone economic sentiment slipped in September but remains strong and private lending continues to accelerate.

What I didn’t like

- A2 Milk shares closed the week down 9.4%, finishing at $10.24, after chief executive Jayne Hrdlicka sold all her shares in the company following just two months in the job! What a message to the market and the share price slump was to be expected, so what was she thinking?

- The China-Trump tariff rhetoric won’t cool down, with Trump accusing China of getting involved in the upcoming mid-term elections. On Monday, the US applied tariffs of around 10% on US$200 billion of Chinese goods.

- This from Shane Oliver after the Fed raised rates by 0.25%: “Continuing US rate hikes mean ongoing downwards pressure on the Australian dollar and the risk of more ‘out of cycle’ rate hikes by Australian banks to the extent global borrowing costs rise.”

- News that the Italian coalition Government will target a 2019 budget deficit of 2.4% of GDP has pushed the Euro down and is a negative for Italian shares and bonds.

- And this from Shane: “The risks around the housing market are continuing to mount, with more banks withdrawing from SMSF lending and signs of a crackdown on property investors with multiple mortgages, as the banks move to comprehensive credit reporting (i.e. sharing information on customer debts) and focusing on total debt to income ratios. The latter is significant, given estimates that nearly 1.5 million investment properties are held by investors with more than one property.”

Donald is a gem

With the Canadian trade negotiations floundering, this is how President Trump adds his unique input into the mix. He actually said this: “We don’t like their representative very much.” Her name is Chrystia Freeland but I’ve never heard a national leader ever get so playground personal in politics. It’s nearly like a comedy line you might have expected from Norman Gunston.

He’s hurting our stock market for the moment but he is a media entertainment machine!

The Week in Review:

- I wrote about why I disagree with great investors like Warren Buffett who say diversification is for wimps.

- Paul Rickard reviewed Wesfarmers again and looked at whether the conglomerate is still a sell.

- If you have some surplus cash and are looking to add to your portfolio, James Dunn listed four company bargains worth considering.

- Ahead of the Global Gaming Expo next month, Charlie Aitken wrote that Aristocrat Leisure offers a compelling opportunity.

- Chris Bedingfield, Principal and Portfolio Manager at Quay Global Investors, selected Scentre Group as the Stock of the Week.

- Looking at the Australian dental-services industry, Tony Featherstone highlighted two stocks to smile about.

- Resources and industrials were in the good books for the first edition of Buy, Hold, Sell – what the brokers say for the week, while in the second edition Woolworths received an upgrade and Whitehaven Coal received a double upgrade.

- In Questions of the Week, we helped a reader out with some ETF basics and suggested some ETFs that offer an inroad into Asia.

- CBA’s head of SMSF Customers, Marcus Evans, wrote that SMSF investors are shaking their home bias and are getting more adventurous than their fellow non-SMSF investors.

- Our Hot Stocks this week are Brickworks and Northern Star Resources.

Top Stocks – how they fared:

What moved the market?

- The release of the interim report from the banking royal commission boosted the banks.

- Trade talks between the United States and China stalled, while Japan began negotiating with the US for a free-trade agreement and Canada appeared less likely to agree to Trump’s NAFTA deal.

- The US Fed raised interest rates 0.25%, the eighth rise since 2015.

Calls of the week:

- Paul Rickard said it is time to lighten and take some profits on Wesfarmers.

- Charlie Aitken picked Aristocrat Leisure as a potential bargain.

- The NRL judiciary found Billy Slater not guilty of a shoulder charge, clearing him to play in the grand final.

The Week Ahead:

Australia

Monday October 1 — CoreLogic Home Value index (September)

Monday October 1 — CBA/AiGroup manufacturing gauges (September)

Tuesday October 2 — Reserve Bank Board meeting

Wednesday October 3 — CBA/AiGroup services gauges (September)

Wednesday October 3 — Building approvals (August)

Wednesday October 3 — New vehicle sales (September)

Thursday October 4 — International trade (August)

Friday October 5 — Retail trade (August)

Friday October 5 — Speech by Reserve Bank official

Overseas

Sunday September 30 — China Purchasing manager indexes (September)

Monday October 1 — US ISM Manufacturing Index (September)

Monday October 1 — US Construction spending (August)

Tuesday October 2 — US New vehicle sales (September)

Wednesday October 3 — US ADP private employment (September)

Wednesday October 3 — US ISM Services index (September)

Thursday October 4 — US Challenger Job Cuts (September)

Thursday October 4 — US Factory orders (August)

Friday October 5 – US Non-farm payrolls (September)

Friday October 5 — US International trade (August)

Food for thought:

I have cities, but no houses. I have mountains, but no trees. I have water, but no fish. What am I?

Send in your answer to subscriber@switzer.com.au

Stocks shorted:

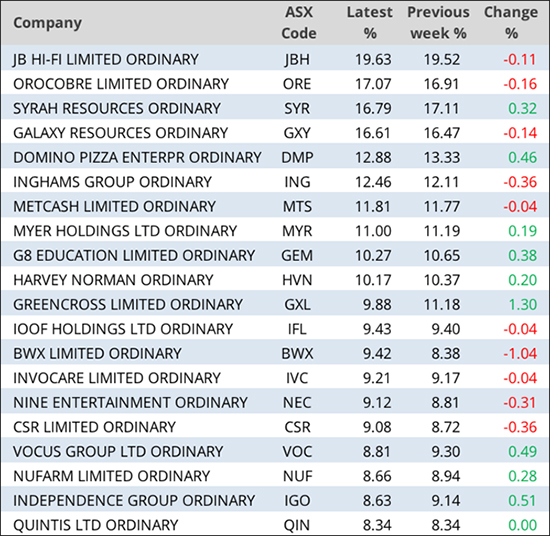

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week:

Chart of the week:

The federal budget deficit for the 2017/18 financial year was the lowest it has been in a decade, as this chart from CommSec shows:

Source: Federal Treasury, CommSec

Source: Federal Treasury, CommSec

Top 5 most clicked:

- 4 company bargains under $4 – James Dunn

- Aristocrat Leisure – buy ahead of Global Gaming Expo (G2E) – Charlie Aitken

- Buffett said diversification is for wimps. He was wrong! – Peter Switzer

- 2 stocks to smile about – Tony Featherstone

- Is Wesfarmers still a sell? – Paul Rickard

Recent Switzer Reports:

- Monday 24 September: Challenging the oracle

- Thursday 27 September: Play the game

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.