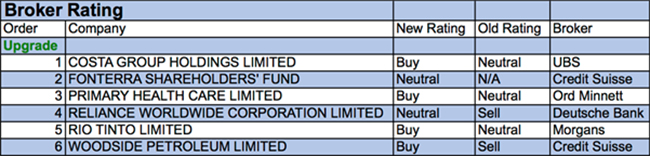

For the week ending Friday, 21st September 2018, FNArena registered a total of six upgrades and downgrades. The positive side doesn’t reveal one dominating theme other than most upgrades going towards share market laggards, including Rio Tinto, Reliance Worldwide and Primary Healthcare.

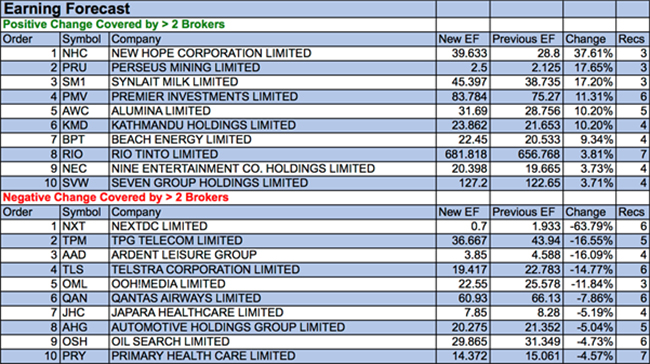

Positive earnings estimates adjustments were hefty, with New Hope Corp commanding the week’s lead, handsomely beating Perseus Mining, Synlait Milk and Premier Investments. Not so lucky were NextDC, TPG Telecom, Ardent Leisure, Telstra and oOh!media were earnings estimates took a large step backwards.

The share market overall continues to be dominated by international tensions and portfolio rotation into value laggards.

In the good books

PRIMARY HEALTH CARE LIMITED (PRY) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 2/2/3. The Fair Work Commission has intervened in a dispute relating to the Dorevitch pathology business, ordering Primary Health Care to offer pay increases of up to 20% to around 1800 workers. The company has confirmed the impact on underlying net profit in FY19 would be -$4.5 million and plans to take measures to mitigate the impact. Clarification on the long-delayed ruling removes an overhang, according to Ord Minnett. The broker reduces FY19 earnings estimates by 2%. The target increases to $3.30 from $3.10. The broker expects attention can now turn to improving the business under the new management team, with the potential for a boost to Medicare funding ahead of the next federal election.

RIO TINTO LIMITED (RIO) was upgraded to Add from Hold by Morgans. B/H/S: 6/1/0. Rio Tinto plans to return the $3.2 billion in net proceeds from the sale of its remaining coal assets through a new off-market share buyback, which will be carried out over the remainder of 2018. While the buyback is a positive, Morgans struggles with the move to divest coal, as it has further concentrated the business. The broker considers the recent weakness in the share price has uncovered attractive value, and healthy metal prices could mean additional capital management and growth is added. Target is raised to $81.32 from $80.67.

RELIANCE WORLDWIDE CORPORATION LIMITED (RWC) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 3/2/0. Deutsche Bank is pleased that John Guest is on track as it is the near-term catalyst for the business. The broker remains concerned that adequate US sales margin growth can be achieved, nonetheless, as the opportunities are largely in lower margin segments. While forecasts remain unchanged, given the recent underperformance in the share price, the broker upgrades to Hold from Sell. Target is $4.80.

WOODSIDE PETROLEUM LIMITED (WPL) was upgraded to Outperform from Underperform by Credit Suisse. B/H/S: 3/4/0. Credit Suisse believes Scarborough’s time has come. The broker, with a new analyst assuming coverage, considers Scarborough makes up for the aspects of the business it does not like, presenting a more de-risked project than is widely credited. Woodside’s unique industry position and appetite for greater LNG market exposure is the differentiator. Positive announcements regarding Browse are also expected and major downside risks, aside from the oil price, are believed unlikely to materialise in the near term. The broker raises the target to $40.50 from $27.20.

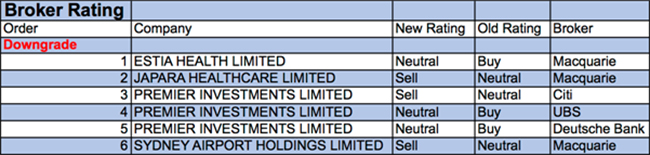

In the not-so-good books

See Thursday’s update for commentary.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.