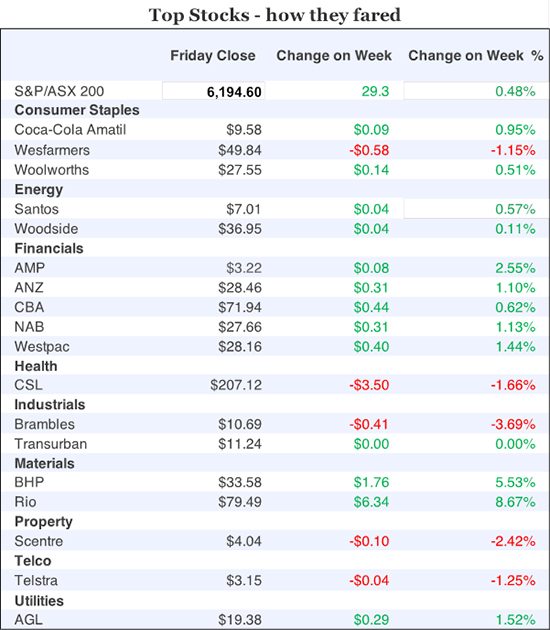

[table “355” not found /]

Trump-v-China on the trade war battlefield was always going to be the main game and because the exchange of tariff fire was less than expected, our stock market climbed higher. The S&P/ASX 200 rose 29 points (or 0.41%) to end at 6194.6, which was the best weekly showing for September.

Helping the positivity was the 10% tariffs rather than the possible 25% slugs once referred to by the US President. And the measured response by the Chinese allayed the worst of market fears. And because the trade war was more like a skirmish, metal prices rose, which helped the share prices of BHP and Rio.

In case you missed it, BHP was up 5.5% to $33.58, while Rio, which also announced a substantial buyback (a $3.2 billion whoppa!) spiked 8.7% to $79.49. And the banks sneaked higher, despite the continued bad headlines out of the Royal Commission.

One unexpected curve ball was the PM’s Aged Care Royal Commission announcement. Estia Health closed 18.3% lower, while Japara Healthcare dropped 17.9%. And the news was bad for others, such as Regis and Aveo.

One negative that might have subdued the rise in stocks was the higher Aussie dollar, which went from 71.5 US cents to nearly 73 US cents by week’s end. This appreciation was linked to the lack of a real trade war this week.

Another not entirely observed development of the week was nicely summed up by AMP Capital’s Shane Oliver. This is how he saw the week’s big market moving action: “The past week saw “risk on” with the latest escalation in the US/China trade conflict being less than feared and reports that China is planning cuts to its import tariffs. This saw shares rally, bond yields rise, commodity prices gain, the US dollar fall and the Australian dollar rise. While the Australian share market participated in the global share market rebound, over the last week it has gone back to underperforming again, reflecting its relatively defensive/high yield characteristics.”

Apart from the rising dollar, all the post-trade developments, such as rising bond yields, all say you can keep believing in the US economic growth and solid corporate profits story, which underpin rising stock markets.

Shane’s take on these important changes in policy by the Chinese makes for great reading. Let me share it with you: “The latest round of US/China tariffs announced over the last week had been long flagged and both the US increase (10% on $US200bn of imports from China, but not yet 25%) and China’s less than proportional retaliation (5-10% on $US60bn of imports) were less than feared.

This and China’s commitment not to use a devaluation in the Renminbi, as a weapon in the trade conflict, along with reports that China is planning a broad cut to its tariffs, leaves scope for negotiations. It’s also worth noting that we are still a long way from a full-blown trade war.

After implementation of the latest round, only about 12% of US imports will be subject to increased tariffs and the average tariff increase across all imports is just 1.6%, implying about a 0.2% boost to inflation and a less than 0.2% impact on economic growth. In China, the economic impact is likely to be less than 0.5% of GDP. This is all a long way from 1930 when the US levied a 20% tariff hike on all imports and other countries did the same making the depression ‘great’.”

My best read of the week came from Goldman Sachs, whose economics team gave the US economy three years before they could see a recession showing up. They say a recession any time soon is “muted” and the chances over the next three years is 36%, which is below the historical average.

“Our model paints a more benign picture in which robust growth – coupled with receding concerns that financial conditions were unsustainably easy – have so far put a lid on US recession risk,” Goldman economists wrote.

I’ve often argued that historically low interest rates should turn this bull market into a long one, with average ones around nine or so years. That’s how long this one has been going on for now. Of course, a black swan could upset my apple cart but right now I feel comfortable that known-knowns point to generally rising stock prices.

Watching the US for recession signs is very important for what our stocks will do and the Goldman team indirectly explained why: “Historical experience suggests that recessions in the U.S. have gone hand in hand with recessions elsewhere. Looking at the past four decades, the average chance of a recessionary quarter in the next year in another developed market economy is just over 20% if the US is not currently in recession but nearly 70% if it is!” (That’s my exclamation mark because this is an important fact about the role of Wall Street and the US economy.)

Consistent with this story about how the US stock market is good for ours is the fact that the Dow Jones index has finished in record high territory for the past two days and had not threatened these heady heights since January, showing how President Trump’s tariff play has been worrying markets.

The downgrading of trade concerns is putting the more important share price drivers into focus.

“I’ve been a bit surprised at how robust the rally has been given the chatter on trade,” said Michael Geraghty, equity strategist at Cornerstone Capital. He noted, however, equities are also benefiting from strong corporate profits. “The stock market is strong because the economy is strong and the economy is strong because corporate earnings are strong.” (CNBC)

And long may that be so, as it will help our market trend higher.

What I liked

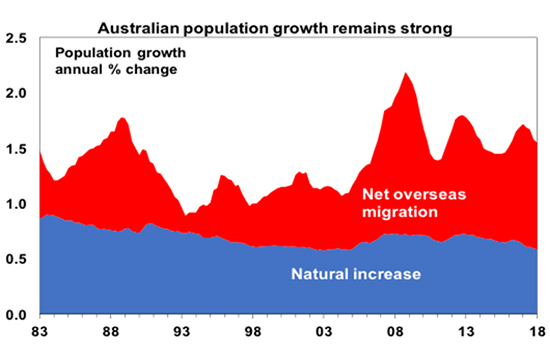

- Australia’s population expanded by 380,722 over the year to March 2018 to 24,899,077 people. Overall, Australia’s annual population growth rate fell from a downwardly-revised 1.58% (previously 1.59%) in December 2017 to 1.55% in March 2018.

- Employment rose by 103,600 in the three months to August after a gain of 65,300 in the previous three months. Over the past 12 months, 301,200 people have found jobs, down from 318,100 in the 12 months to May. A record 12.66 million Aussies are employed.

- The Internet Vacancy Index rose by 0.6% in August – the strongest growth rate in six months. The index is 4.5% higher than a year ago – still near six-year highs.

- Over the year to July, a record 1,433,300 tourists came to Australia from China, up by 9.4%. A record 339,200 Indian tourists travelled to Australia over the year to July, up by 19.5%. And a record 28,800 tourists came to Australia from Argentina, up by 37.8% over the year.

- The US leading index rose by 0.4% in August (forecast +0.5%).

- The Philadelphia Federal Reserve manufacturing index rose from +11.9 to +22.9 in September (forecast +17).

- Chinese retail rose at a 9% annual rate in the year to August, (forecast: +8.8%), up from 8.8% in July. Real retail sales (taking into account inflation) rose at a 6.6% annual rate in the year to August, up from 6.5% in July.

- Chinese industrial production rose at a 6.1% annual rate in August, above the forecast average (+6%). Production had risen by 6% in the year to July.

What I didn’t like

- On Monday, the US applied 10% tariffs on $200 billion of Chinese goods. The Chinese tariffs of 5% to 10% were smaller than those expected by analysts. (This was a better-than-expected result but I still don’t like these tariff tit-for-tat antics.)

- The lack of local economic data last week!

The dollar and stocks ahead

Here’s Shane Oliver’s views on stocks and the dollar, which I largely agree with, though he’s a little more negative on stocks than me, which shouldn’t surprise you.

For stocks: “We continue to see the trend in shares remaining up, as global growth remains solid, helping drive good earnings growth and monetary policy remains easy. However, the risk of a correction over the next two months still remains significant, given the threats around trade, emerging market contagion, ongoing Fed rate hikes, the Mueller inquiry in the US, the US mid-term elections and Italian budget negotiations. Property price weakness and approaching election uncertainty add to the risks around the Australian share market.”

For the dollar: “While the $A is working off very negative short positions and oversold conditions resulting in another short-term bounce, it’s still likely to fall to around $US0.70 and maybe into the high $US0.60s, as the gap between the RBA’s cash rate and the US Fed Funds rate pushes further into negative territory as the US economy booms relative to Australia. Being short the $A remains a good hedge against things going wrong in the global economy.”

By the way, the Fed will undoubtedly raise interest rates next week and what the associated statement says will be read very closely by major market players. We could see some interesting action next week.

The Week in Review:

- After our Switzer Listed Investment Conference (SLIC) last week, these are the stocks and strategies from SLIC that will make me money.

- While buying into a listed managed fund is a great way to get market exposure, Paul Rickard looked at whether you should choose an exchange traded fund or listed investment company.

- These are the five stocks you need to look at to ride the infrastructure boom according to James Dunn.

- Charlie Aitken wrote that it’s time to pick up some unloved potential at bargain-basement prices.

- Tony Featherstone listed the 10 things you need to know before investing in tech ETFs.

- Senior portfolio manager at Alleron Investment management, Alan Kwan, chose QBE as the Stock of the Week.

- There were two upgrades for Myer and one for Ansell Limited in the first Buy, Hold, Sell – what the brokers say for the week, while in the second edition Estia Health and Japara Healthcare were both downgraded on the back of the announced Royal Commission into aged care.

- In Questions of the Week, we responded to a reader’s concerns about an imminent financial crisis, and a question about how to give shares to grandkids.

- Roger Montgomery highlighted three companies that will be affected by electric vehicles

Top Stocks – how they fared:

What moved the market?

- The market improved after the latest trade war tariffs were lower than expected.

- Industrial and precious metal prices jumped, pushing BHP Billiton, Rio Tinto and other materials stocks higher.

- The aged care royal commission announced by the federal government saw aged care stocks drop.

Calls of the week:

- Charlie Aitken said that it’s time to buy rest of world value stocks with an Asian bias.

- Donald Trump followed through on his promise to impose further tariffs on China

The Week Ahead:

Australia

Tuesday September 25 — Weekly consumer sentiment

Wednesday September 26 — Engineering construction activity (June quarter)

Thursday September 27 — Finance & wealth (June quarter)

Thursday September 27 — Job vacancies (August)

Friday September 28 — Private sector credit (August)

Overseas

Monday September 24 — US Dallas Fed Manufacturing Index (September)

Tuesday September 25 — US S&P/Case-Shiller Home Prices (July)

Tuesday September 25 — US Consumer confidence (September)

Tuesday September 25 — Richmond Fed Manufacturing Index (September)

25-26 September — US Federal Reserve interest rate policy meeting

Wednesday September 26 — US New home sales (August)

Thursday September 27 – China Industrial profits (August, year)

Thursday September 27 — US Trade in goods (August)

Thursday September 27 — US Economic growth (final, June quarter)

Thursday September 27 — US Durable goods orders (August)

Thursday September 27 — US Pending home sales (August)

Friday September 28 — China Caixin purchasing manufacturing (Sep.)

Friday September 28 — US Personal spending/income (August)

Friday September 28 — US Consumer confidence (September, final)

Sunday September 30 — China official purchasing manufacturing (Sep.)

Food for thought:

What is 3/7 chicken, 2/3 cat and 1/2 goat?

Send in your answer to subscriber@switzer.com.au

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week:

Overseas migration continues to play a major part in the population growth of Australia as can be seen in this chart by AMP Capital:

Source: ABS, AMP Capital

Source: ABS, AMP Capital

Top 5 most clicked:

- The stocks and strategies from our SLIC conferences that will make me money – Peter Switzer

- 5 stocks to ride the infrastructure boom – James Dunn

- Buying the peak of gloom – rotate from growth to value – Charlie Aitken

- The best managed investment – Paul Rickard

- Buy, Hold, Sell – what the brokers say – Rudi Filapek-Vandyck

Recent Switzer Reports:

- Monday 17 September: Expert opinion

- Thursday 20 September: Is it different this time?

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.