I have consistently warned you of the downside risks in Ramsay Health Care over the last two years and today I want to confirm that my fund remains short Ramsay and why I think this stock has further to fall over the year ahead.

Ramsay shares have fallen -34% since mid-2016. This is despite universal bullishness from sector analysts and commentators. Nobody seems to want to believe that the best is behind Ramsay and that is why it still has further to fall.

Stocks do not bottom until we see complete analyst and investor capitulation. That hasn’t happened yet in Ramsay, in fact, most analysts keep reiterating their buy recommendations and lowering price targets.

Key concerns

I want to start by reminding you of my key concerns with Ramsay, which I have consistently stated.

- Expensive: significantly higher than its long-term price to book ratio (currently at 5.3x book value vs. long-term median of 3.0x)

- Regulatory Risk: review into Prostheses pricing has not been reflected in Ramsay’s earnings as yet, and could have an impact on profitability, along with tariff cuts in France & UK.

- Significant Insider Selling: New managing director Craig McNally sold $4.8 million worth of stock only 8 weeks ago.

- Competitor Downgrades: biggest competitor, Healthscope (HSO), has experienced management turnover, earnings downgrades and significant insider selling.

In their recent update, Ramsay advised that its FY18 Core EPS growth is now expected to be 7% compared to previous guidance of 8% to 10%. There are currently 7 buys, 4 holds and 1 sell recommendations on the stock and the consensus share price target is $67.38. We believe that, despite Ramsay’s share price weakness and earnings downgrade cycle, the analysts still look at this stock historically. We continue to target a $54.00 share price for Ramsay.

In delivering the core EPS downgrade, Ramsay cited the following reasons:

- A downturn in NHS volumes in the UK

- Weaker growth rates in procedural work and inpatient admissions in Australia

- Delays in the rollout of the Pharmacy franchises in Australia

This is the first time we have seen Ramsay own up to the Australian weakness and we think this will continue to impact through FY19. Ramsay themselves noted they are “facing more challenging market conditions in Australia with lower growth in procedural work and inpatient admissions” and that they expect operating conditions to “remain challenging”.

Normal abnormals?

In addition to this, Ramsay took a $125 million provision for onerous leases in the UK – just another abnormal. All of Ramsay’s UK hospitals operate from rented premises and no hospitals are being relocated or closed down, therefore it represents just another significant operating expense being taken below the line.

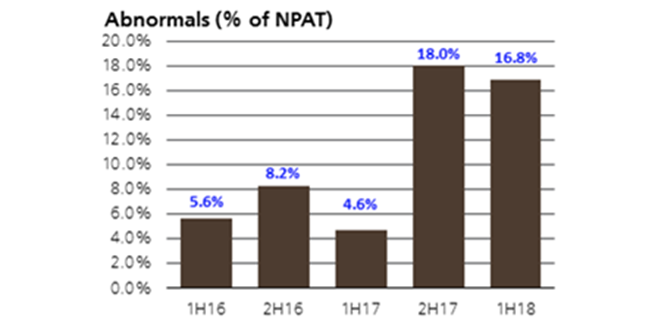

This is on top of the clear earnings deterioration highlighted in the most recent half yearly result. The result showed that to achieve NPAT guidance Ramsay are booking high levels of abnormals. This means it is relying heavily on taking costs below the line to meet expectations. “Non-core” expenses grew to 17% of H1 statutory NPAT from 11% in FY17 and 7% in FY16. The only major significant cost to be singled out by Ramsay management was a restructuring charge taken at its French operations to centralise non-core functions. A pre-tax charge of €44m was taken (“below the line”) for a program which is targeted at producing €5m of annual (“above the line”) cost savings once the program is fully implemented in three years. By most metrics a program that has implementation costs approximately nine times the targeted annual cost saving is marginal. However, it does serve to help preserve “normalised earnings”. The below graph shows the abnormals, as a % of NPAT over the last five halves:

Source: UBS

As we mentioned in our last Ramsay note, when you are trading on a premium P/E rating you simply can’t consistently book high percentages of abnormals. High P/E’s need clean earnings streams, not messy ones. It’s a simple as that.

The half yearly result also revealed that sales growth in Ramsay’s Australian operations moderated to 4.3% yoy, whilst the French and UK operations went backwards.

It was also clear that operating cash flows were showing a diverging trend from reported profit growth. Gross cash receipts for the business (cash from customers minus payments to suppliers and employees) went backwards in FY17 and again went backwards in 1H FY18. This is now starting to show through in the company’s earnings.

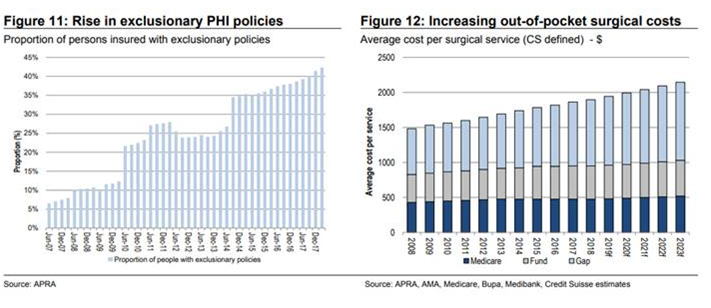

Industry dynamics (notably Private Health Insurance affordability issues) also mean that we are unlikely to see a recovery in Australian private hospital volume growth in the near term. Australian private hospital industry volume growth slowed to 2.8% in 1H18, below the long-term average of 4.2%, as more patients shifted to the free and high quality public substitute. According to Credit Suisse this is a structural shift due to 1) Funding incentives for public hospitals to admit more private patients; 2) A deterioration of Private Health Insurance (PHI) hospital cover and rise in exclusionary policies; and 3) A rise in out-of-pocket surgery costs. This is highlighted below:

Therefore, we continue to think there is more to play out in this re-rating cycle with more near term negative news flow and also the lowering of FY19 expectations. As a result, maintain a short position in Ramsay Health Care.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.