[table “282” not found /]

In case you were feeling a little nervous with one US negatively-inclined market expert tipping we’re one event away from a 5%-6% drop in stocks, along came two biggies on Thursday with the UK election and the James Comey testimony.

I said in Switzer Daily that it was arguably the most eventful Thursday since Holy Thursday, with the possibility of a ‘stock market crucifixion’, if things went wrong.

That might be ahead of us, with the UK election result getting worse by the minute. And who knows what the Comey show-and-tell will bring out?

In the final wash up, the UK election saw the Tories have to rely on the Democratic Unionist Party of Northern Ireland to stay in power but the FTSE still managed to rise 61 points, which just shows how positively-inclined markets overseas are now. The rest of European stock markets ended higher as well.

Over to the USA and CNBC says Tomey’s revelations were “explosive but there’s no smoking gun” but I guess what you think could rest on what you’re smoking! Wall Street’s reaction was always going to be a big watch and this is what happened: the Dow was up 89 points, while the S&P 500 was down 2 points. In summary, the Yanks couldn’t give a toss about the UK and the FBI boss’s case against the President is not an issue, at least for the moment.

The economic readings and company earnings are dominating in the US for now and optimism is trumping pessimism, and well may it remain so.

Of course, the UK and US stuff is all unsettling for markets and while we finished on Friday just in the green, the UK result wasn’t totally known and we did lose 110 points for the week (or 1.9%) on the S&P/ASX 200 index.

Fortunately, the European Central Bank didn’t make the waters muddier. Mario Draghi lifted his forecast for growth for the Eurozone from 1.8% to 1.9% for 2017 and he didn’t touch interest rates.

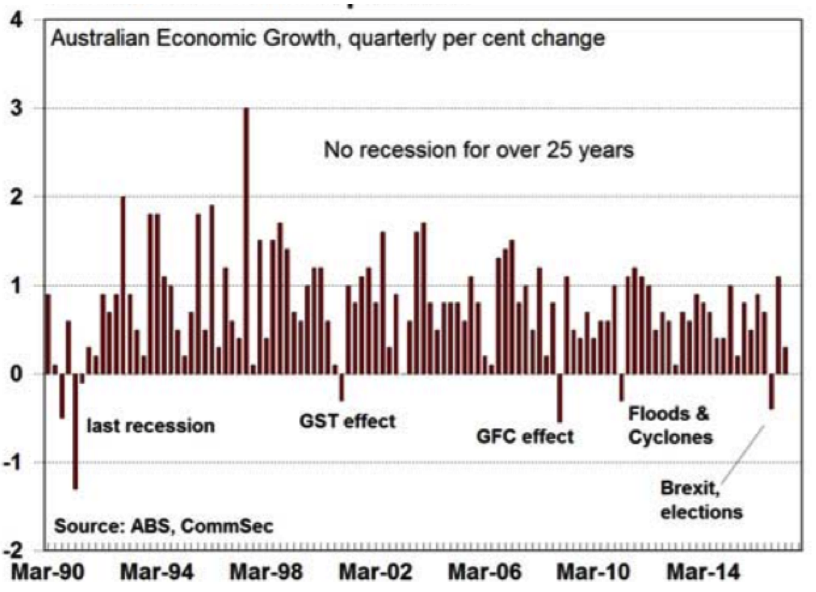

Good news for the week locally was the March quarter economic growth number that came in at 0.3%, when some economists were tipping a negative result. We’ve now gone 103 quarters without a recession, so we’re tying with the Dutch, who did the same until the GFC ended their good run of growth. And after we see the June result, we will be world record holders.

This week, I looked at the economic readings for the June quarter so far and it looks like we’ll see another positive quarter. This is what I dug up:

- Employment rose by 37,400 in April, after rising by 60,000 in March. Full-time jobs fell by 11,600, while part-time jobs rose by 49,000. Economists had tipped a 5,000 increase in jobs.

- Unemployment fell from 5.9% to 5.7%.

- Job advertisements rose to six-year highs, up by 0.4% in May and up 7.5% on a year ago.

- The weekly ANZ/Roy Morgan consumer confidence rating rose by 0.7 points (0.6%) to an 8-week high of 112.9 in the week to June 4.

- The NAB business conditions index rose from +12.3 points to +14.3 points in April, a 9-year high. The business confidence index rose from +6.5 points to +12.9 points, a 7-year high.

- The Performance of Services index fell 1.5 points to 51.5 in May. The index remains over 50, signifying expansion of the services sector.

- New motor vehicle sales totaled 102,901 in May, up 6.4% on a year ago and a record for a May month.

- Retail trade rose by 1% in April – the biggest rise in over 2½ years. Annual growth rose from a 4-year low of 2.2% to 3.1%.

- Over the last six months, investment expectations have lifted by 5.1%.

- The CoreLogic Home Value index of capital city home prices fell by 1.1% in May but was up 8.3% over the year. It was the biggest monthly fall in prices in 18 months but the RBA, APRA and the Government want to kill this bubble talk, so we’ll take it as a good thing!

- The Performance of Manufacturing index fell from near 15-year highs, down by 4.4 points to 54.8 in May. A reading above 50.0 indicates that the sector is expanding. This was the eighth consecutive month of expansion.

- Housing approvals rose by 0.8% in April. Meanwhile, ‘lumpy’ apartment approvals rose by 8.9% in April.

- New home sales rose by 0.8% in April, after falling by 1.1% in March.

- One ‘baddie’ was this: private sector credit rose by 0.4% in April, after a 0.4% gain in March. However annual credit growth of 4.9% is the slowest in three years.

That’s good news but I can’t jump up and down pointing to good news ahead so I suspect we will be in this negative phase until some catalyst for positivity comes along. That said, don’t be too negative, as Morgan Stanley upgraded its target for the S&P 500 Index by 11% to 5700 for 2017 only this week. Its current level is 2433.9, so go Morgan Stanley!

Unfortunately, for this May, there were plenty of reasons to sell and go away but I bet you a lot of sellers will become buyers later this year.

What I liked

- UBS upgraded BHP from a “neutral” rating to a “buy” rating today, sticking with its price target of $28.

- The thought that the banks and Telstra are becoming another contrarian play opportunity – watch this space.

- Good news for Vocus shareholder sufferers, with the private equity bid pumping up the stock price by 33%. Those investors needed that!

- Chinese inflation rose 1.5% in May, which was seen as a good sign.

- Craig James of CommSec on Comey: “The testimony of former FBI director James Comey to the Senate intelligence committee contained no surprises. Investors shifted back to the Trump “reflation trade”, with sectors linked to infrastructure spending getting a boost.”

- This from James on our record growth story: “But importantly the record expansion remains on track. Especially positive is the health of the business sector with business conditions the best in nine years. The hope is that employment and investment will continue to lift, maintaining economic momentum.”

- This from the RBA this week: “Business conditions have improved and capacity utilisation has increased. Business investment has picked up in those parts of the country not directly affected by the decline in mining investment. Year-ended GDP growth is expected to have slowed in the March quarter, reflecting the quarter-to-quarter variation in the growth figures. Looking forward, economic growth is still expected to increase gradually over the next couple of years to a little above 3 per cent.”

What I didn’t like

- Oil prices down 4% this week. This hit our energy sector.

- Supermarket war talk and Wesfarmers down 4.6% this week.

- The banks’ slide, with NAB down 2.8%, ANZ 2%, CBA 1.5% and Westpac off 1.8%.

- The number of home loan approvals fell 1.9% in April and was more than was expected but it’s what the RBA and APRA want to slow down house prices.

What I’d like to see

Some unambiguously good piece of news, such as Trump’s tax bill being passed!

The week in review:

- This week, I explained why I don’t think it’s time to sell everything. Here’s my case.

- The Aussie share market fell in May and while the income and growth portfolios underperformed during the month, they are up in the calendar year. Read Paul Rickard’s analysis here.

- James Dunn explained why it’s important to do your homework when confronted with a private equity IPO proposition.

- Premier Investments was in the good books this week, while AGL and Wesfarmers were downgraded.

- Tony Featherstone revealed 3 niche A-REITs that stand out in a sluggish market.

- Charlie Aitken said last week’s “sell everything” stories were a case of fake news. He also thinks there’s opportunity in APN Outdoor.

- In our second broker report, Boral was in the good books while Westfield was downgraded.

Top stocks – how they fared

What moved the market?

- A better-than-expected GDP number. The Aussie economy expanded by 0.3% in the March quarter.

- Britain’s general election.

- Former FBI director James Comey’s Senate testimony.

- A weaker oil price.

Calls of the week

- The RBA kept the cash rate on hold at a record low of 1.50%.

- Last week, Tony Featherstone tipped Vocus Group as a takeover target. This week, KKR lobbed a takeover bid for Vocus at $3.50 a share!

- And Charlie Aitken doubled down on his view about that eccentric Fundie’s highly publicised “sell-everything” call from last week. He called the coverage a serious case of “FAKE NEWS”.

The week ahead

Australia

- Monday June 12 – Queen’s Birthday holiday

- Monday June 12 – Speech by Reserve Bank official

- Tuesday June 13 – NAB Business survey (May)

- Tuesday June 13 – Weekly consumer confidence

- Tuesday June 13 – Overseas arrivals/departures (April)

- Tuesday June 13 – Credit & debit card lending (April)

- Wednesday June 14 – Monthly consumer confidence (June)

- Thursday June 15 – Employment/unemployment (May)

- Thursday June 15 – Speech by Reserve Bank official

- Thursday June 15 – Reserve Bank Bulletin

Overseas

- Monday June 12 – US Federal Budget (May)

- Tuesday June 13 – US NFIB Business Optimism (May)

- Tuesday June 13 – US Producer prices (May)

- June 13 & 14 – US Federal Reserve meeting

- Wednesday June 14 – US Consumer prices (May)

- Wednesday June 14 – US Retail sales (May)

- Wednesday June 14 – China activity data

- Thursday June 15 – US Philadelphia Fed survey (June)

- Thursday June 15 – US Industrial Production (May)

- Friday June 16 – US Housing starts (May)

Food for thought

The entrepreneur always searches for change, responds to it, and exploits it as an opportunity.

Peter Drucker

Last week’s TV roundup

- With Amazon set to enter the Australian market, what does it mean for local retailers like JB Hi-Fi? Michael McCarthy from CMC Markets joins Super TV to answer this and more.

- It’s not long until the super changes come into effect. To discuss the actions you should consider taking now, Frank Paul from Spring Financial Group joins the show.

- Tom Elliott from Beulah Capital discusses private equity firm KKR’s share offer for Vocus Communications, plus other takeover news.

- Is the housing market cooling? Destiny’s Margaret Lomas shares her property tips.

- And don’t miss our video on the top ten tips you should be thinking about ahead of the end of financial year.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

One of the biggest movers this week was Select Harvests, with its short position increasing by 2.07 percentage points to 9.98%.

Source: ASIC

Chart of the week

25 years without a recession!

Australia’s better-than-expected GDP figure for the March quarter showed those doomsayers where to go! The economy grew 0.3% in the quarter, while annual growth was 1.7%. As you can see from CommSec’s chart above, our economy hasn’t experienced a recession for more than 25 years!

Top five most clicked stories

- Peter Switzer: Is it time to sell everything? The case against it, now

- Paul Rickard: Product Road Test – Contango Global Growth

- Charlie Aitken: “Sell everything” is “fake news”… APN Outdoor is good value

- Tony Featherstone: 2 telco takeover targets

- Rudi Filapek-Vandyck: Buy, Sell, Hold – what the brokers say

Recent Switzer Super Reports

- Thursday 8 June, 2017: Fake news

- Monday 5 June, 2017: Big call merchants

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.