JB Hi-Fi (JBH) and Harvey Norman (HVN) have been slammed.

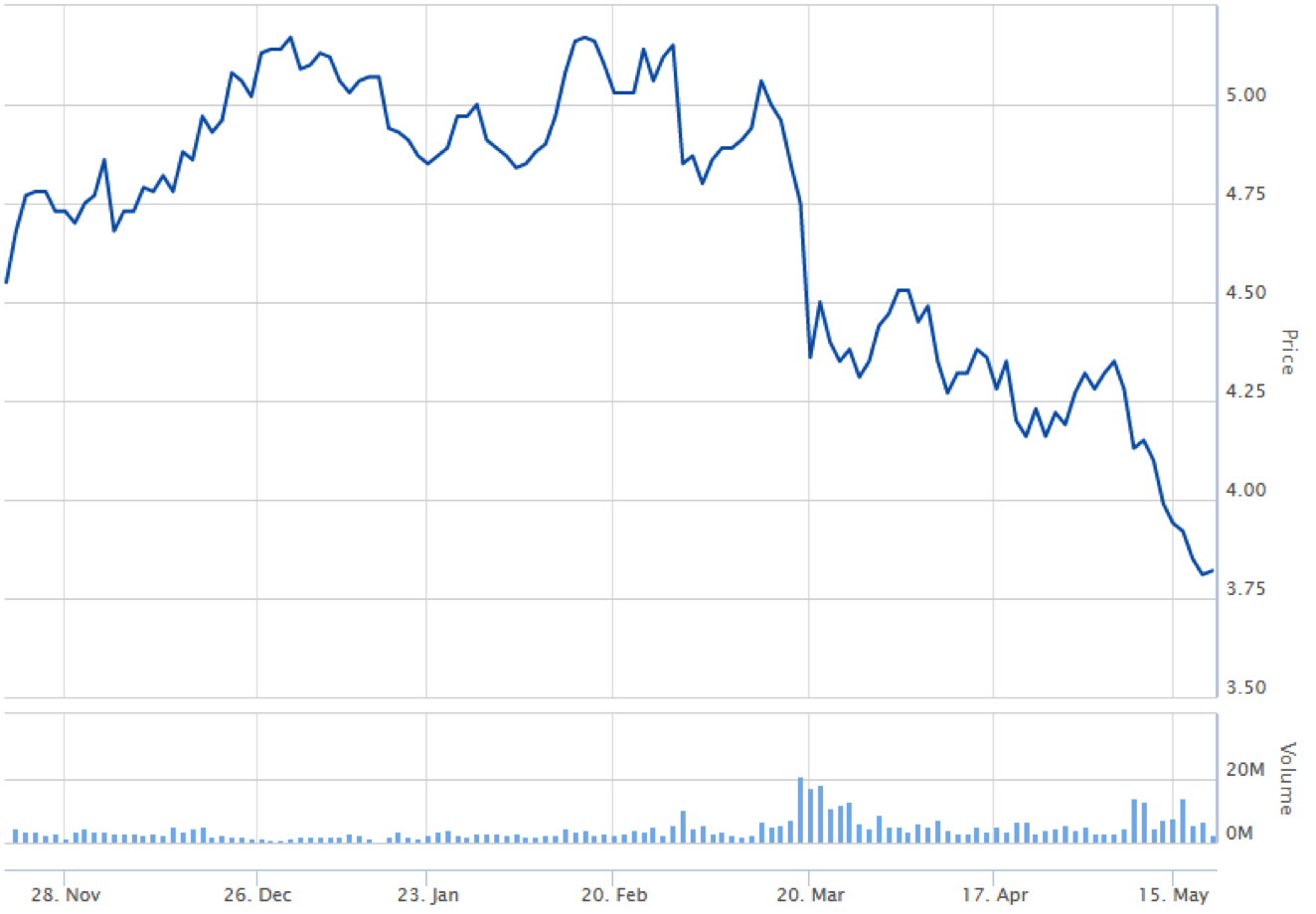

From its high of $30.78 on 13 February, shortly after the presentation of an outstanding set of half year accounts, JB Hi-Fi has almost 25%, closing Friday at $23.27.

JB Hi-Fi – 6 months to 19 May 17

Harvey Norman has fallen 27% since hitting a high of $5.24 on 28 February, again shortly after the announcement of its half year results. HVN closed on Friday at $3.82.

Harvey Norman – 6 months to 19 May

The shorters are active in both stocks and have been building positions. According to the latest ASIC figures this morning (which effectively show trade date positions from COB last Tuesday), 10.42% of JB Hi-Fi’s ordinary shares, or 11.93m shares worth around $300m, are short sold. For Harvey Norman, it is 8.47% or 94.3m shares worth around $360m.

And while the short interest is largely about the Amazon threat, there are a couple of other factors at play.

Subdued retail sales also causing concern

Flat retail sales are also causing concern. According to the ABS, retail turnover fell by 0.1% in March following a fall of 0.2% in February. Over the last 12 months, turnover is up by just 2.1%.

While the ‘department store’ category is the weakest (with a fall of 2.7% over the 12 months), the ‘household goods category’, which both JB Hi-Fi and Harvey Norman fit into, is up by just 0.6% over the 12 months.

Interestingly, this data seems somewhat inconsistent with recent sales data from JB Hi-Fi and Harvey Norman. JB Hi-Fi reported comparable store sales growth for the March quarter of 8.2% (1.2% for the Good Guys business), while Harvey Norman reported comparable store sales growth of 4.8% for the first 4 months of 2017 and 4.8% for the 10 months to April 30.

One other point to note from the ABS data is the relatively slow penetration of online sales. According to the ABS, online sales still only represent 3.7% of all retail turnover. Taking away the food and café/restaurant/take way categories boosts the proportion to 8.5%, but it is still less than 10%.

There is also a concern that a downturn in the housing market will impact furniture and home appliance retailers such as Harvey Norman, and increasingly JB Hi-Fi following its acquisition of The Good Guys.

How credible is the Amazon threat?

Every expert thinks Amazon is a very credible player. It has deep pockets, and potentially poses a material threat to Australian retailers.

However, the only thing that is publicly known about Amazon in Australia is that it plans to launch a business. While it recently invited small businesses to express interest in being a partner on Amazon Marketplace and has reportedly being lodging trademark applications, the timing or nature of its offer is not yet known. Many expect that the initial offer will focus on consumer electronics and household items, although an Amazon Fresh business (fresh food) can’t be ruled out.

If you want to see more on the Amazon threat, and in particular, how it approached the UK market with Amazon Fresh, retail expert Tristan Kitchener discussed this in The Switzer Super Report a few weeks back.

Shoppers in Australia are amongst the most price conscious in the world, so an offer from Amazon that is cheaper should be appealing. Citi analysts recently estimated that in three major retail categories, Amazon in the US, UK and Germany is around 15% cheaper than Australian retailers. This led them to slash their long-term earnings and price targets for JB Hi-Fi, the latter by a massive 35% to just $18.50.

Whether Australian consumers will be comfortable in paying a “membership fee” (in the US, Amazon Prime is $99 or $10 a month and comes with a number of benefits including free shipping) remains to be seen. Australia’s vast and sparsely populated geography may also make Amazon’s logistical challenges a little more acute than the USA or continental Europe.

And then there is the relatively slow take up of online shopping here. Perhaps Australian consumers are just waiting for Amazon and materially lower prices, or perhaps some view shopping as a recreational activity.

One thing for certain is that the market sees the threat as credible and real.

JB Hi-Fi reaffirms profit guidance

At a presentation to the Macquarie Australia Conference on 3 May, JB Hi-Fi re-affirmed its guidance for FY17:

- Group sales to be circa $5.58 bn (JB Hi-Fi $4.33bn cw $3.91bn in FY16, and The Good Guys $1.25bn); and

- Underlying NPAT to be in range of $200m to $206m, an increase of 31.4% to 35.4% on FY16 of $152.2m.

Harvey Norman doesn’t provide guidance, but did update the market on 16 May with 10 months’ sales data (see above).

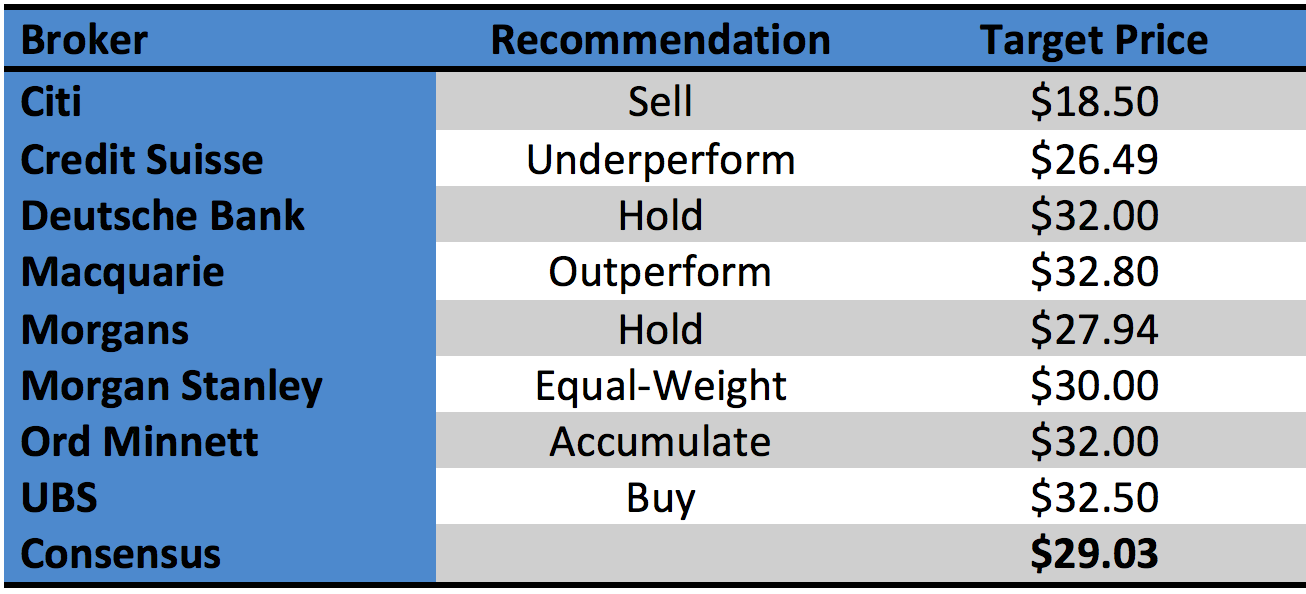

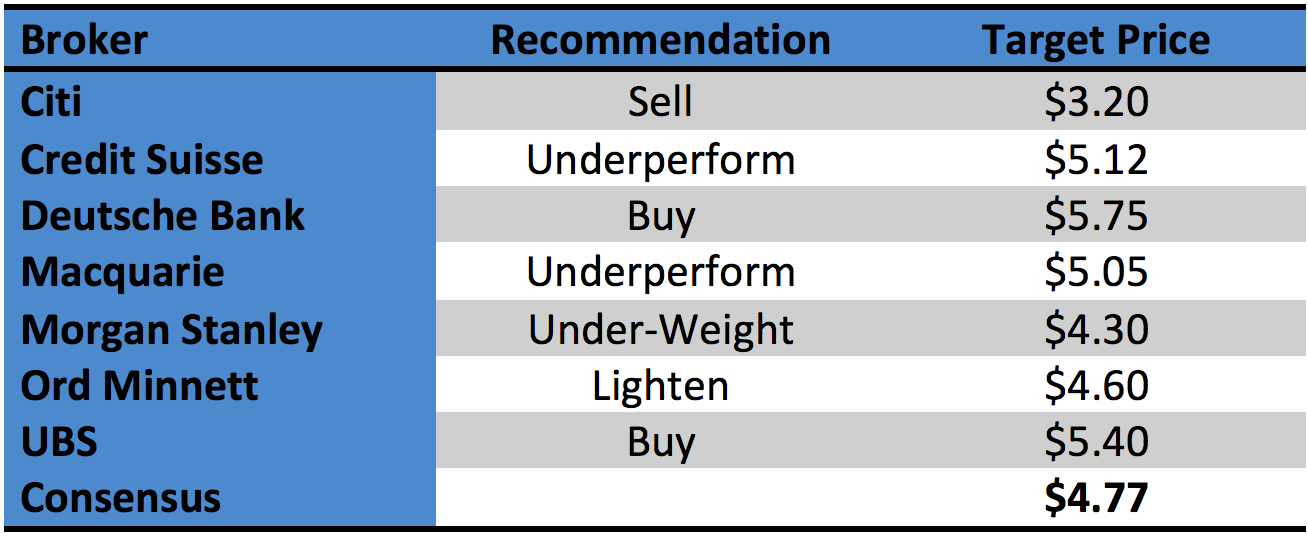

The Brokers

The brokers are largely in two camps. On the one hand, analysts such as Citi who maintain that Amazon will have a very material impact on long-term earnings, while others such as UBS maintain that the companies are executing well on strategy, winning share and trading on undemanding multiples. According to FNArena, there is a wide range in broker target prices.

Broker Target Prices and Recommendations – JB Hi-Fi

Broker Target Prices and Recommendations – Harvey Norman

On current prices, the Brokers have JB Hi-Fi trading on a multiple of 12.6 times FY 17 earnings and 11.3 times FY 18 earnings. Because of concerns about the headwinds from a slowing housing market, multiples for Harvey Norman are lower at 10.9 and 10.6 times. The brokers expect Harvey Norman to maintain dividends at about 30c per share, putting it on a yield of around 8% (fully franked).

Market Consensus Forecasts

Bottom line

I like both stocks. JB Hi-Fi a little more because I think it is the premier retailer in Australia. It doesn’t have the same exposure to the housing market as Harvey Norman (although the Good Guys acquisition has put it in this space), and doesn’t have to deal with franchisees.

Both businesses will have to compete with Amazon. They also have had a long time to prepare for its arrival.

In my experience with markets, “rumour/hype/perception” is usually worse than reality (ie “buy the rumour, sell the fact”), but I am not sure whether we have yet reached the peak of the “Amazon fear”. Hence, I think it is a brave investor who stands in front of the short train.

Long term buyers will need to be very patient investors, and potentially have to ware quite a bit of short term pain. They will, however, be rewarded with quite attractive dividend yields.

Courageous buys.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.