The Budget was good for stocks on Wednesday and Thursday, then along came Friday and the banks gave into gravity. The S&P/ASX 200 Index lost 0.7% to finish at 5836.9 but it did sneak up a tad over the week.

So, just how bad was the Budget for the banks? Well, the CBA lost 3.2%, Westpac 3.8%, ANZ dropped 4.7%, while NAB lost only 0.6%, which wasn’t a bad effort. That said, I can’t think of anything else that happened in the world of banking that could have explained their share prices’ fight with gravity.

Part of the reason why the Index did OK, despite the big banks (which are good for about 25% of the Index) was the better performance of mining stocks and, of course, infrastructure stocks, with the Budget being so good for the latter sector of the stock market.

Retailers are also fighting negativity, with even a US hedge fund manager piling into JB HiFi this week. Its share price went from $26.65 to $23.88 over the five days trading but there are those out there who don’t believe JB haters.

A month or so ago, UBS identified a group of stocks that it labeled the B-team, with JB, Harvey Norman and Bluescope (and others) all tipped to have a good year ahead!

It comes when Gerry Harvey was flabbergasted by a Citi analyst, who said retail was verging on a recession! Gerry called it “fake news” pointing out that he, and other well-known retailers, are doing well. “There’d be a lot of retailers out there doing extremely well; it’s a good market at the moment,” Mr Harvey said. “For everyone to talk about being on the verge of recession, it’s such a stupid thing to say.” (SMH)

I think some parts of retail are troubled but others are clicking over nicely. I don’t like the retail figures for assessment of the economy because the modern consumer now spends a lot on services – massage, hair care, personal training, telco, cleaning, etc. – which don’t show up in the retail figures. They also buy more from overseas via the Internet and while that can be an economic problem for local retailers, it can mean higher disposable income for local consumers, who then spend it on more services and café lattes.

I’ve even been caught getting my toes and fingers manicured and that wouldn’t have happened 10 years ago!

I think the Amazon hype has been spliced into the share prices of JB and HVN, and UBS could well be on the money with these companies. By the way, Citi points to the slowdown in the housing sector but work started on 231,658 new dwellings over 2016 – a record for a calendar year. And unless the modern builder is a much better beast that those of yesteryear, I’d say a lot of these properties will still be built over the rest of this year. And then they have to be sold and then stocked with new stuff from the likes of JB and Gerry’s stores. Also, approvals for new builds remain historically high and many of these homes would not even have been started!

Retail did have a bad week in the USA, with JCPenney down 14% overnight and the likes of Macy’s and Nordstrom having a shocker when they reported. That said, the Commerce Department said retail sales increased 0.4% in April from March. This number was less than expected but was OK, considering it’s still a cold month for shopping in America.

I think department stores are a risky bet nowadays, as Myer has shown, but it doesn’t mean all retail is bad, with Nick Scali being a case in point.

What I liked

- The overall positivity of the Budget but the bank bashing was a pity.

- The NAB business conditions index rose from 12.3 points to 14.3 points in April, a 9-year high. Business confidence rose from 6.5 points to 12.9 points – a 7-year high.

- Job advertisements rose by 1.4% in April to 169,268 ads – a near 6-year high.

- The ANZ/Roy Morgan consumer confidence rating rose by 0.9% to a three-week high of 112.3 in the week to May 7. Confidence is down 1.4% over the year and below the average of 113.2 since 2014.

- US consumer prices rose 0.2% in April, in line with expectations and in the 12 months to April, the CPI increased 2.2%. (The 10-year average rise is only 1.7%)

- Boston Fed President Rosengren (he’s a non-voter on rates) delivered a speech saying that he sees three more rate hikes in 2017 as “reasonable” and that the Fed should begin to shrink its balance sheet “relatively soon”.

- The Greek stock market rose for the 12th straight day – the longest run of gains in 26 years – as Athens looked set to receive a further bailout tranche.

- Tourists from China and Hong Kong rose to a record 1,488,400 over the past year, up 12.1% over the year.

- In smoothed terms, discount airfares are up by 17.8% on a year ago. Restricted economy fares are up 3.5% over the year – the strongest growth in 13-months. This industry is on the comeback trail.

- The Macron victory in France’s election and the market reaction worldwide.

- Oil prices rose this week.

- US consumer prices rose from an annual growth rate of 0.9% in the year to March to 1.2% for the year to April. Economists had expected annual growth of 1.1%.

What I didn’t like

- Retail sales fell by 0.1% in March, after falling by 0.2% in February. Spending is up just 2.1% over the year – the weakest annual growth in nearly four years.

- Dwelling approvals fell by 13.4% in March, after rising by 8.9% in February. It was the largest decline in 16 months. (However, over the past year, 225,440 new homes were approved, down from the record high 241,994 in the year to August 2016.)

- The bank levy and its impact on stock prices and super.

- Bill Shorten’s reply! He needs some tutoring from Paul Keating on how to be pro-worker without being an enemy of business and higher income Australians.

- Big US retailers are in strife but I don’t blame the economy. It’s the Internet! Macy’s shares fell 17% on Thursday after weak quarterly performance. Kohl fell 7.9%, while shares in Nordstrom (-7.5%) and JCPenney (6.7%) also fell sharply on the day.

- President Trump fired his FBI director James Comey and impeachment talk escalated! The last time a US President was impeached and not acquitted, the stock market didn’t like it. And given Trump’s tax plans and their importance to the stock market, it’s a worry, but only a mild one now. However, it could get scary.

On the Budget

I can’t get excited about a Budget until I see what the wacky team of opportunists in the Senate decide to do. We really don’t need another Budget impasse but, if this does happen, it will hurt the economy and Malcolm Turnbull’s leadership. It could eventually hurt stock prices, as this is a pro-growth Budget but, if the growth is delayed, then there could easily be a reassessment of current stock valuations.

If the Budget largely goes through, bank share prices will recover, based on a stronger economy. However I suspect we’ll see some more downside for the big four banks, while Macquarie, with its foreign earnings and the expected lower $A, could easily do a bit better than its rivals. There will be buying opportunities then for our banks because I believe the growth story for Australia.

The week in review

- I discussed what the French election and the Federal Budget could mean for stocks.

- Despite the arguments for it, Australian investors are “underweight” offshore investing. Paul Rickard conducted a road test of a new LIC that offers access to a portfolio of global stocks. Find out more.

- James Dunn revealed five high-yielding stocks under a dollar.

- The brokers upgraded oOh!Media (OML), while Qantas (QAN) and Super Retail Group (SUL) were downgraded.

- Our Super Stock Selectors shared the stocks in their likes and dislikes list.

- What will the new tax mean for the major banks and investors? Charlie Aitken shared his views on this and explained why he likes Henderson Group (HGG).

- Portfolio taken a beating? Tony Featherstone discussed five ways small investors can get off the canvas and regain share market confidence.

- Travel services business Helloworld (HLO) has the formula for a great turnaround story and Ben Griffiths from Eley Griffiths thinks there’s growth ahead for the company. Find out why.

- In our second broker report, the Commonwealth Bank (CBA) received an upgrade and a downgrade this week, while brokers downgraded both Westpac and NAB.

Top stocks – how they fared

What moved the market?

- Pressure on the big bank’s after the Government’s Budget announcement of a levy on the top five was leaked.

- Stronger oil prices in response to a bigger-than-expected drawdown in US oil inventories.

- Retail spending figures, which fell 0.1% in March, and negative reports on the retail sector from Citigroup, weighed on some retail stocks.

Calls of the week

- ScoMo’s call to slap a $6.2 billion tax on Australia’s five largest banks, to be raised over four years. Watch Peter’s interview with Treasurer Scott Morrison here.

- US President Donald Trump’s call to dump FBI director, James Comey.

- Charlie Aitken said Henderson Group is a cheap stock with plenty of medium-term upside. Find out why.

- And French President-elect, Emmanuel Macron, announced 429 candidates for the parliamentary elections in June: half are women and more than half are new to politics.

The week ahead

Australia

- Monday May 15 – Housing finance (March)

- Tuesday May 16 – Weekly consumer confidence

- Tuesday May 16 – Reserve Bank Board minutes

- Tuesday May 16 – New vehicle sales (April)

- Wednesday May 17 – Lending finance (March)

- Wednesday May 17 – Consumer sentiment (May)

- Wednesday May 17 – Wage price index (March quarter)

- Thursday May 18 – Employment/unemployment (April)

Overseas

- Monday May 15 – US NAHB housing market (May)

- Monday May 15 – US Capital flows (March)

- Monday May 15 – US Empire Manufacturing survey (May)

- Monday May 15 – Chinese economic data

- Tuesday May 16 – US Housing starts (April)

- Tuesday May 16 – US Industrial production (April)

- Thursday May 18 – US Philadelphia Fed index (May)

- Thursday May 18 – US Leading index (April)

- Thursday May 18 – China home prices (April)

Food for thought

“The best thing I did was to choose the right heroes.” – Warren Buffett

Last week’s TV roundup

- Treasurer Scott Morrison joins Super TV to discuss the details of the Budget including the bank levy, infrastructure spending and more.

- For another view on this week’s Budget including the new bank levy, David Murray, who is a former CBA CEO and headed up the Financial System Inquiry, joins Super TV. Watch part two here.

- Last year the big-cap stocks had a nice comeback, and this year mid-caps are higher too, so when will the small- and micro-cap stocks join the party? Bill Laister from Contango Asset Management joins the show.

- One of the big pressure points for the Treasurer as he constructed his Budget was, how would the credit rating agencies view his efforts? Christopher Joye shares his views.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week one of the biggest movers was Bellamy’s Australia, with a 3.07 percentage point increase in the amount of its shares sold short to 11.26%.

{kind=link}

Source: ASIC

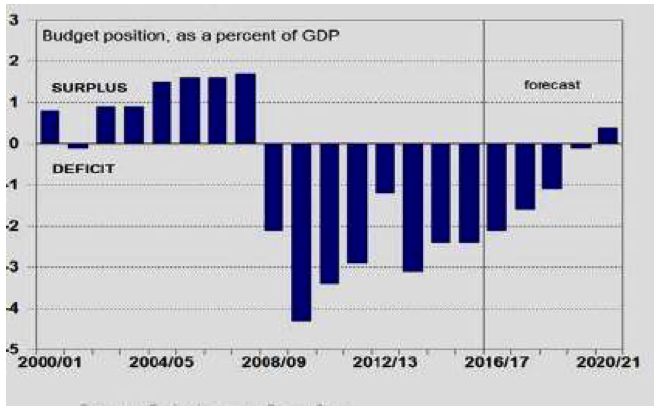

Chart of the week

Return to surplus in 2020/21?

Source: Budget papers, CommSec

A deficit of $29.4 billion or 1.6% of GDP is tipped for 2017/18 – down from $37.6 billion or 2.1% of GDP this year. And we’re expected to return to surplus in 2020/21. Let’s hope these forecasts become reality!

Top five most clicked stories

- James Dunn: 5 high yielders under a dollar

- Charlie Aitken: Short Scomo, long HGG

- Rudi Filapek-Vandyck: Buy, Sell, Hold – what the brokers say

- Peter Switzer: What France and the Budget can do to our stocks!

- Bernadette Morabito: Hot stocks: The Big Four and Bapcor

Recent Switzer Super Reports

- Thursday 11 May 2017: The “Beam us up, Scotty, Budget”

- Monday 8 May 2017: Budget week

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.