The arguments for investing offshore are well known. Firstly, the Australian market is small – less than 2% of global stock markets by capitalisation. This means that 98% of opportunities are outside Australia.

Secondly, our market is dominated by financial and resources stocks. The financials sector makes up 39.2% of the Australian market, compared to 14.1% in the USA. For materials, it is 15.5% compared to 2.9%. Conversely, information technology stocks make up 22.5% of the US market compared to a trifling 1.2% in Australia. Our market simply doesn’t have the Apples, Alphabets, Amazons, Microsofts or Facebooks, or in the healthcare sector, pharmaceutical giants like Pfizer, or industrial giants like General Electric.

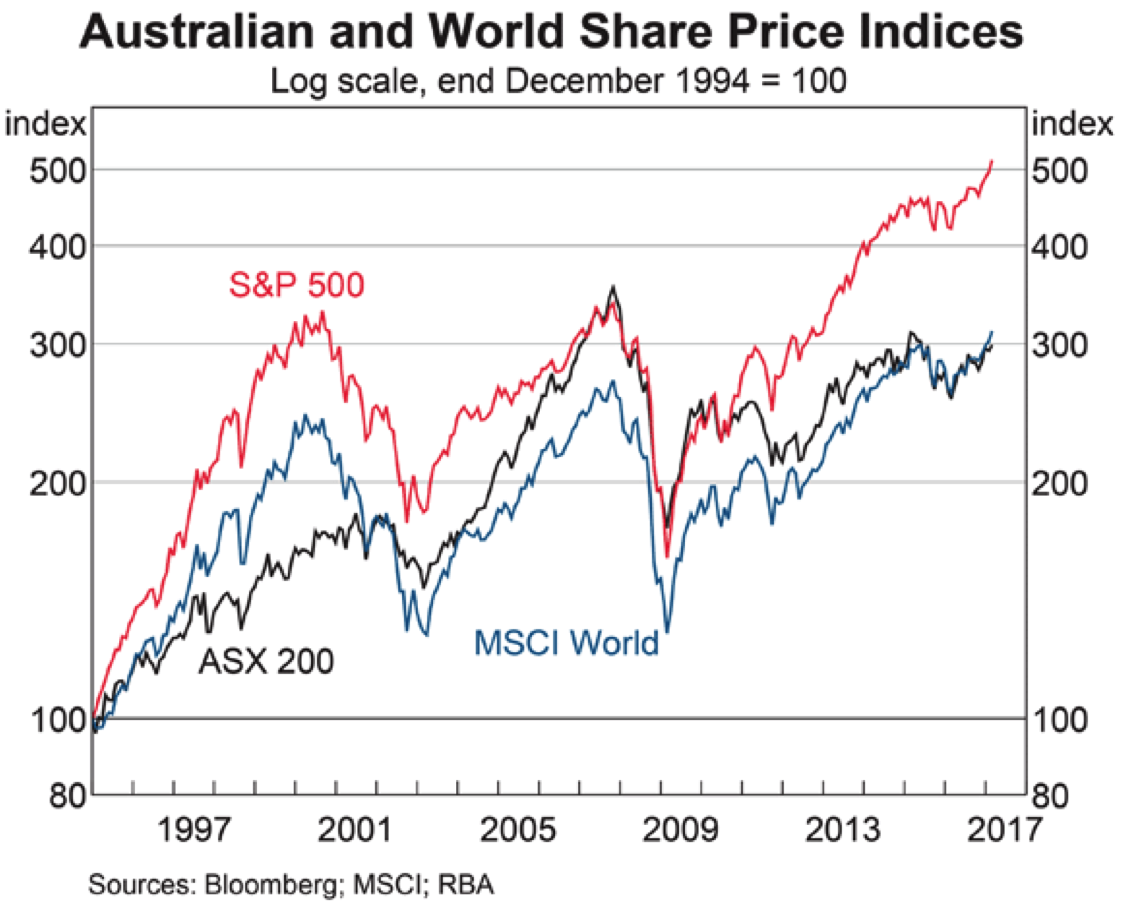

Thirdly, international share markets will often outperform the Australian market. While this can be true over any short term period, it is also true over a longer period. The following graph from the RBA shows the Australian (black), US (red) and World (developed markets, blue) over a 22 year period, using a common base and logarithmic scale. Over this longer period, the US market has outperformed the Australian market.

Yet, Australian investors remain “underweight” offshore investments.

So, a new IPO for an ASX listed investment company that offers easy access to a portfolio of global stocks managed by a very successful US fund manager should be a proposition worth considering.

But, before we road test the product, some very important disclosures. Firstly, I am a Non-Executive Director of the new listed investment company, Contango Global Growth Limited. My colleague, Mr Marty Switzer, is also a Director. Secondly, Switzer Financial Group will earn a broker firm selling fee of 1.5% of the value of successful applications lodged through us.

Contango Global Growth Limited

An ASX listed investment company, Contango Global Growth Ltd (CQG) provides investors with access to an actively managed portfolio of global equities. A high conviction portfolio, it will typically comprise 20 to 40 global growth companies.

Via an initial public offer, the Company is seeking to raise up to $330m via the offer of 300m shares priced at $1.10.

The Manager

The Company has appointed Contango International Management Pty Ltd (a wholly owned subsidiary of Contango Asset Management – ASX:CGA) to provide investment and portfolio management services. Contango Asset Management is led by George Boubouras, and manages two listed investment companies (Contango Microcap – ASX:CTN and Contango lncome Generator- ASX:CIE), as well as several wholesale equity mandates.

A specialist global equity manager, WCM Investment Management, will advise Contango and manage the portfolio. Established in 1976, WCM has a long term track record of successfully managing global equities. Privately owned by its active employees and based in Laguna Beach California, WCM has over A$23bn in funds under management. WCM is headed by Paul Black and Kurt Winrich.

The Investment Strategy

The portfolio targets quality global growth businesses with high returns on invested capital, superior growth prospects and low debt. It also requires each company to maintain a durable and growing competitive advantage, or ‘economic moat’.

Typically, this will be between 20 and 40 securities that WCM considers to have the highest expected returns and are reasonably valued. The Company is expected to be largely fully invested in equities, but may hold cash of up to 7.0% of the portfolio’s value.

The aim is to provide returns (before fees, costs and taxes) that exceed the benchmark, the MSCI All Country World ex-Australia Index, by more than 3% p.a. over rolling three-year time periods, but with lower volatility than the benchmark.

WCM will employ an investment strategy that is based on their ‘Quality Global Growth’ strategy, which has been in existence since March 2008. The differences will be the exclusion of any Australian securities, and other investment guidelines determined by Contango.

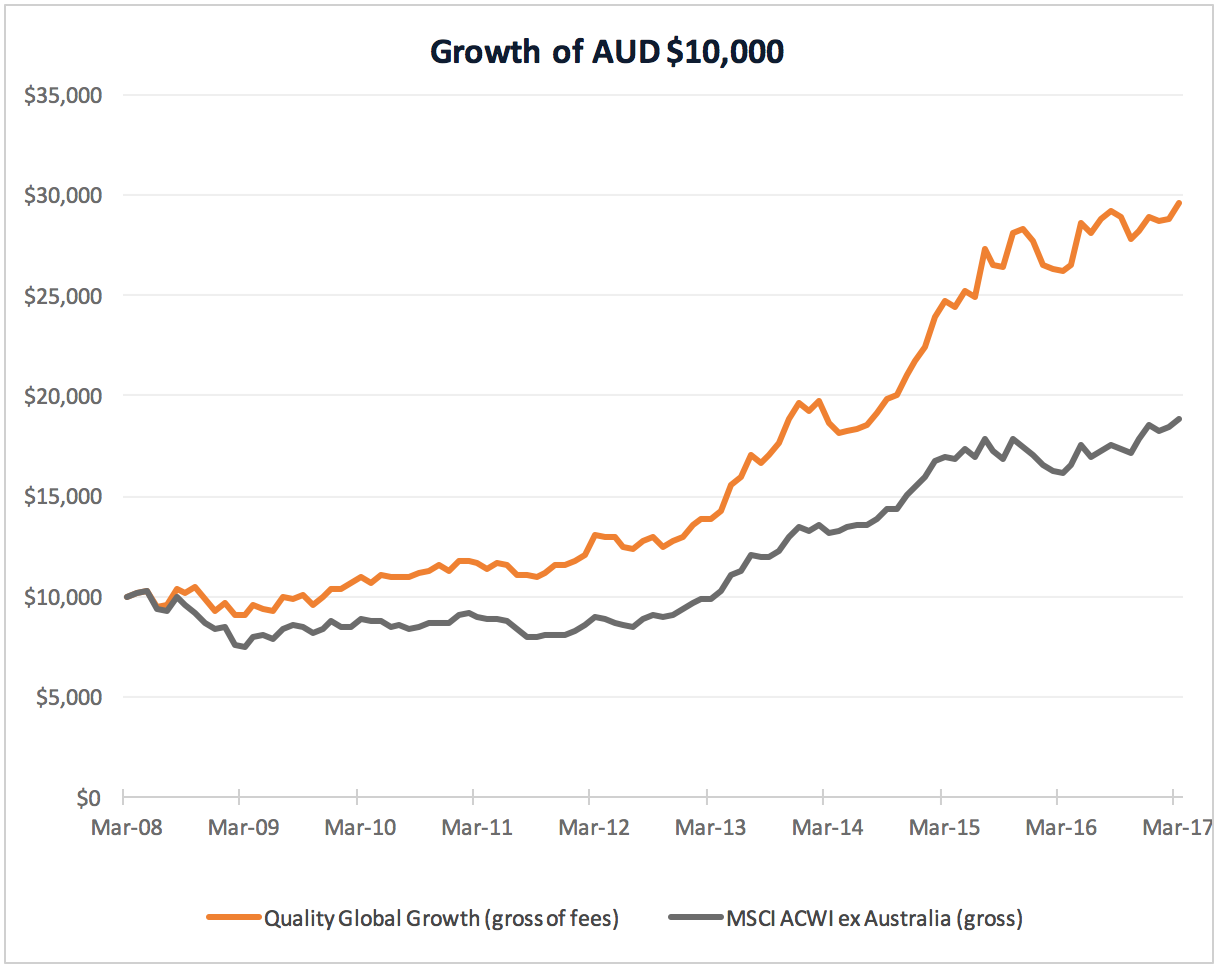

The Quality Global Growth strategy has been very successful. The following chart shows the growth of $10,000 invested in the strategy from March 2008 to March 2017, compared to the benchmark index, the MSCI All Country World ex-Australia. Assuming distributions are re-invested, $10,000 in the strategy (before fees) would be worth $29,568 compared to a theoretical $18,869 from the index.

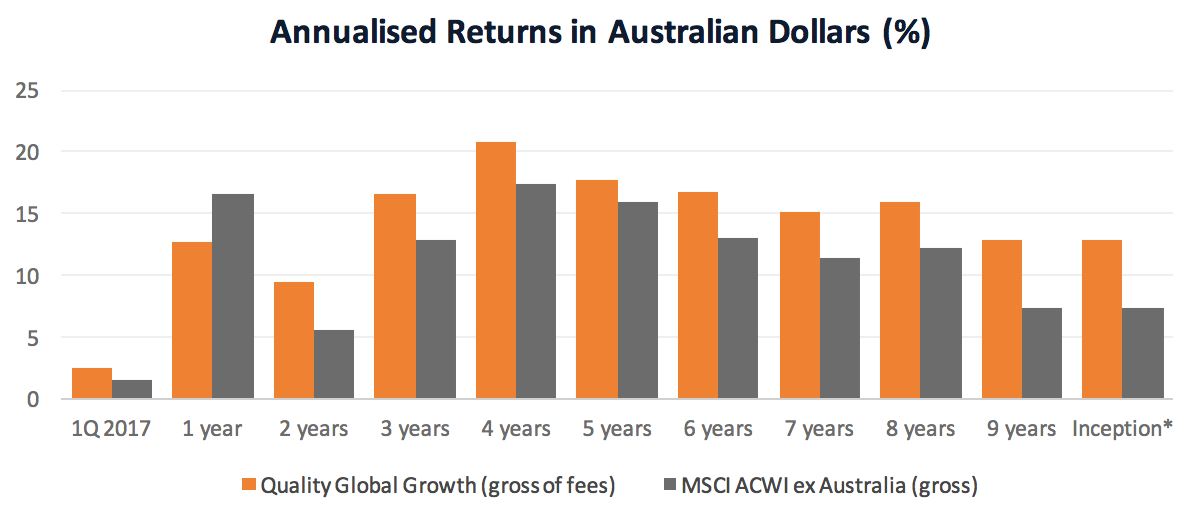

Moreover, the performance has been pretty consistent, with the strategy beating the index over most time periods.

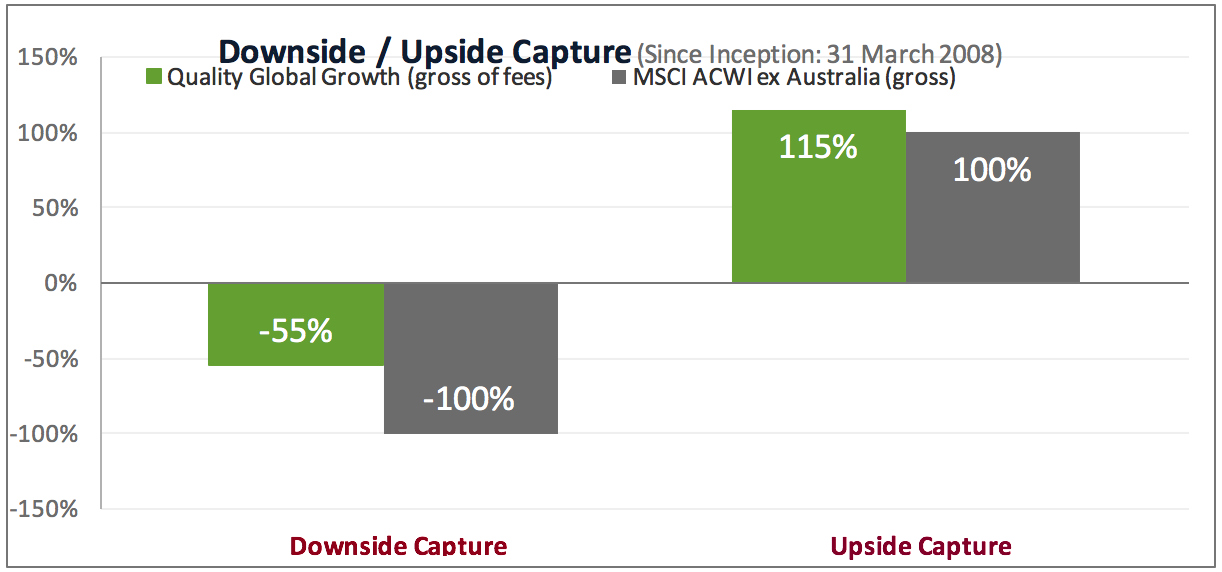

The strategy has also been effective at reducing the impact of market and stock downturns. While it has captured marginally more of the upside, WCM’s Quality Global Growth Strategy has only captured 55% of the downsides over this nine year period.

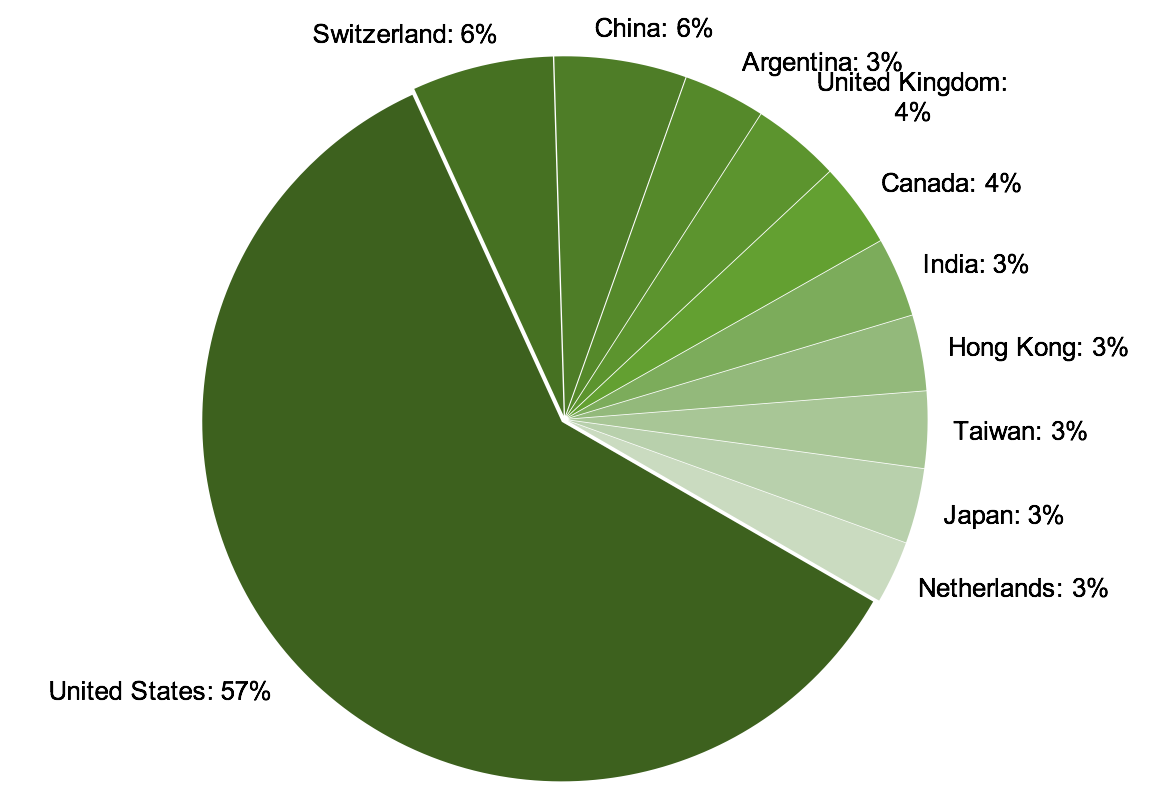

Exposure to developed markets for the portfolio is set at 65% to 100%, while exposure to developing markets in in the range of 0% to 35%. As at 31 March, the Quality Global Growth Strategy had 16% in developing markets. 57% was in the USA, as per the following chart.

The top 10 holdings at 31 March were as follows:

*Source: WCM, Quality Global Growth representative portfolio. March 2017.

Option

Investors in the IPO will receive one option for every share subscribed (1,000 shares will be accompanied by 1,000 options). The option allows holders to subscribe for an additional share at a price of $1.10 per share, and can be exercised at any time up until 24 June 2019.

The options will be separately quoted on the ASX, and will trade under stock code CQGO.

Fees

The Manager will earn a base fee of 1.25% plus GST. This includes the fee paid to WCM. There is also a performance fee (which will be paid in full to WCM) of 10% plus GST of the portfolio’s outperformance relative to the benchmark. This is capped at 0.75% of the portfolio’s value, and subject to recoup of any prior period underperformance.

As a listed investment company, there will also be other operational costs, including custody, registry, audit and directors’ fees. If the offer raises $330m, these are estimated to be 0.4% pa.

Risks

This has the usual risks for an offshore investment. The portfolio won’t be hedged, so investors will be exposed to movements in the value of the Australian dollar.

As an active growth portfolio, dependence on the skill and expertise of the Manager is high. It is also an investment utilizing a listed investment company structure. These and other risks are described in considerable detail in the Prospectus.

The suggested investment timeframe is for a minimum of five years.

IPO time table

The offer is expected to open on the 15th of May, and close on Thursday 8 June. The minimum investment is 2,000 shares at $1.10 per share, or $2,200.

Trading on the ASX is expected to commence on Friday 23 June, under stock code CQG.

The proforma NAV (net asset value) is $1.076 if $330m is raised, down to $1.067 if $55m is raised.

Our view

Apart from all the very sound reasons to invest offshore, investing in Contango Global Growth is essentially about backing an investment adviser (WCM) with an outstanding track record.

As it is a fairly narrow portfolio of 20 to 40 global stocks, there is a high dependence on the expertise of the investment management team. Hence, it is unlikely that Contango Global Growth would be your only offshore investment, or if it is, you should aim to diversify across managers.

If you are interested in considering this investment, please review carefully the Prospectus, which is available here.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.