In the good books

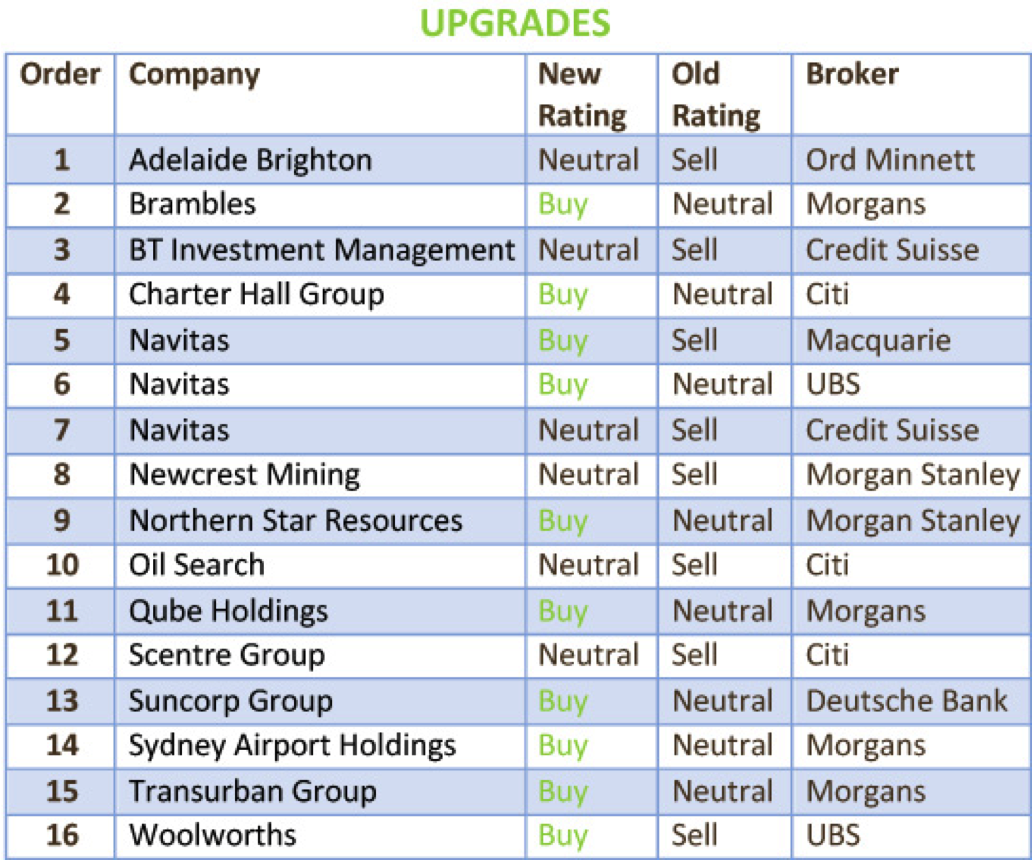

BRAMBLES LIMITED (BXB) Upgrade to Add from Hold by Morgans B/H/S: 5/1/1

Brambles’ recent first half trading update was a disappointment to Morgans, and the broker awaits new FY guidance at the company’s result release. Earnings forecasts have been trimmed in the meantime.

But Morgans believes Brambles’ longer term fundamentals remain solid, suggesting the recent pullback in price represents a buying opportunity. Target falls to $11.61 from $11.91. Upgrade to Add.

SUNCORP GROUP LIMITED (SUN) Upgrade to Buy from Hold by Deutsche Bank B/H/S: 5/2/1

While the fundamentals are in place, valuations for the general insurance sector are approaching that of the broader market and Deutsche Bank takes up a neutral outlook on the sector.

The broker transfers coverage to another analyst and updates its thesis on the sector, highlighting a preference for Suncorp as it is trading at a 20% discount to Insurance Australia Group (IAG), despite operating in broadly similar product lines.

Rating is upgraded to Buy from Hold. Target is raised to $14.00 from $13.70.

In the not-so-good books

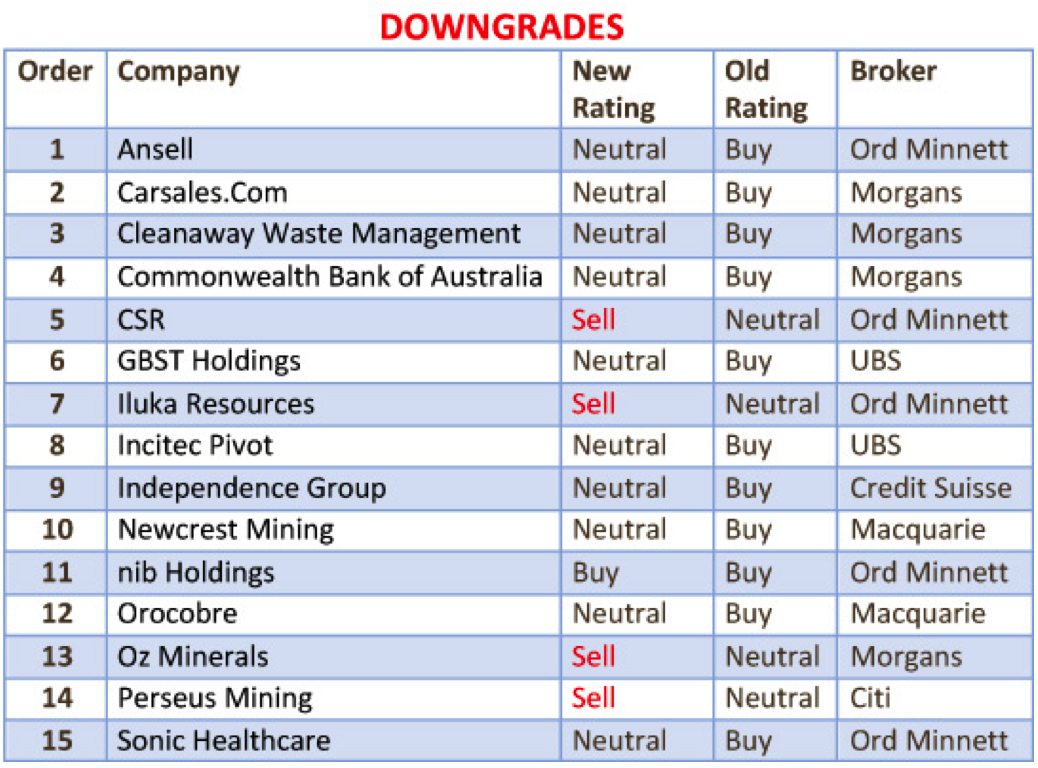

COMMONWEALTH BANK OF AUSTRALIA (CBA) Downgrade to Hold from Add by Morgans B/H/S: 0/6/2

Morgans believes the bank sector is now fully valued following the post US election rally, however an easing in capital requirement expectations supports the broker’s view dividends will remain robust.

CBA is downgraded to Hold. Target rises to $79.00 from $75.80.

CSR LIMITED (CSR) Downgrade to Lighten from Hold by Ord Minnett B/H/S: 1/2/2

Transport restrictions in China have led to tight supply for aluminium in recent months. As this unwinds in the first quarter of 2017, Ord Minnett expects the underlying commodity price to retrace.

In addition, a shift in the global supply/demand balance to an oversupplied position presents another risk. The broker downgrades to Lighten from Hold and raises the target to $3.80 from $3.75.

GBST HOLDINGS LIMITED (GBT) Downgrade to Neutral from Buy by UBS B/H/S: 2/1/0

GBST has issued a profit warning ahead of its result, cutting FY17 earnings guidance to 33% below UBS’ prior forecast. Project delays, deferred spending on major projects in the UK, and the weak GBP are all to blame.

While the risks are not new, the broker is concerned about the size of the downgrade. Improvement in FY18 is dependent on a recovery in services work and/or new contract wins. Elevated R&D costs will remain a significant drag over FY17, the broker notes.

UBS has cut earnings forecasts and lowered its target to $3.40 from $4.35. Downgrade to Neutral.

NIB HOLDINGS LIMITED (NHF) Downgrade to Accumulate from Buy by Ord Minnett B/H/S: 2/4/1

As the share price has rallied, Ord Minnett downgrades to Accumulate from Buy. The main issues the broker envisages in the upcoming first half results are Australian resident health insurance margins, claims inflation and growth trends.

The margins were upgraded at the AGM largely on the back of more favourable claims environment but the company also increased its drawing rate inflation range. The broker awaits further clarity from the commentary on claims inflation trends. Target rises to $5.00 from $4.90.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.