Key points

- Ramsay might be fully priced but it is a company that has consistently met or exceeded its forecasts.

- CSL recently completed the acquisition of Novartis’ influenza vaccine business, making CSL the second largest influenza vaccine manufacturer in the world.

- Resmed’s FY15 revenue was US$1.7 billion, up 13% on a constant currency basis. It’s a little more speculative, but worth the risk.

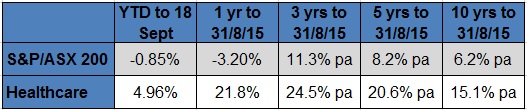

The healthcare sector has been the best performing sector on the ASX over the last decade. To the end of August, it’s up 15.1% pa compared to an average of 6.2% pa for the S&P/ASX 200 – or a massive outperformance of almost 9% per annum. The same is true over 5 years, 3 years, 1 year – and even this calendar year, where the S&P/ASX 200 (as measured by the accumulation index) is down 0.85% to last Friday, while healthcare is up by 4.96%.

Total Returns

An ageing population, government expenditure on healthcare growing at 2% to 3% above GDP growth, new technology, Australia having access to a world class health system and medical research infrastructure, a global market place for products, ideas and innovation – are some of the factors that have led to the performance of Australian healthcare stocks. Australia has global leaders in their fields – companies such as CSL, Cochlear and Resmed – and there aren’t too many other industry sectors where we can make this claim.

Like the rest of the market, healthcare stocks have pulled back in price over the last couple of months. They are not cheap, however, they are certainly more attractively priced – and the long-term factors are still in place. Here are three of my favourite stocks to put on your shopping list for the next pullback.

1. Ramsay Health Care (RHC)

Australia’s largest private hospital operator, Ramsay has been a superb performer on the ASX over the last several years (see chart below). More recently, it has diversified into the UK and France, completing the acquisition of Ramsay Générale de Santé on 1 July. Ramsay Générale de Santé is the largest private hospital group in France – Ramsay holds 50.9%.

Ramsay Health Care – September 2010 to September 2015

In the year to 30 June 15, Ramsay grew NPAT (net profit after tax) by 19% to $412.1 million, or its preferred measure, core earnings per share, by 20% to 196.6c. For the FY16 year, Ramsay is forecasting core NPAT and EPS growth of 12% to 14%.

On Friday’s close of $60.98, Ramsay is trading at a 10% discount to the broker consensus target price of $67.05. Sentiment is marginally positive (four buys/two holds/two sells). The multiple (27 times FY16 earnings) is high – with some brokers feeling that Ramsay is fully priced – however this is a company that has consistently met or exceeded its forecasts. On track record, a “must have” in growth portfolios.

2. CSL Limited (CSL)

CSL is a global specialty biotherapeutics company. With major facilities in Australia, Germany, Switzerland, the UK and US, CSL employs 14,000 staff working in 30 countries. CSL has two main operating divisions – blood plasma products through CSL Behring – and vaccines and pharmaceuticals through bioCSL. CSL recently completed the acquisition of Novartis’ influenza vaccine business, making CSL the second largest influenza vaccine manufacturer in the world.

In FY15, CSL grew sales by 7%, EBIT by 12% and NPAT by 10% (at constant currency and adjusting for acquisition costs). Reported NPAT of US$1.379 billion was up 6% on the previous period. For FY16, CSL is forecasting revenue growth of 7% (at constant currency), and due to an increase in investment and fixed asset depreciation, NPAT growth of just 5% (excluding the Novartis acquisition). With a further buyback foreshadowed, EPS growth is however expected to exceed NPAT growth.

CSL reports in US dollars. Almost 70% of its sales revenue is earned in the US and Europe. Like Ramsay, CSL has been a terrific share market performer.

CSL – September 2010 to September 2015

On Friday’s close of $90.57, CSL is trading at an 11.7% discount to the broker consensus target price of $101.14. Sentiment is positive (six buys/one hold/one sell), and the multiple (20.8 for FY16, based on an A$/US$ of 0.7200 cents) is more respectable. Noting the lower growth forecast for 2016 and investment in the business, brokers see a return to the previous growth trajectory in 2017. A core healthcare stock.

3. Resmed (RMD)

Resmed develops, manufactures and markets products for the treatment and management of respiratory disorders, most particularly sleep apnea. With more than 4,000 employees, Resmed sells its products to approximately 100 countries through direct offices and a network of distributors. For FY15, revenue was US$1.7 billion, up 13% on a constant currency basis, with NPAT up 2% to US$352 million. Resmed does not forecast earnings and reports in US dollars.

While Resmed has been a strong performer on the ASX, it has also had its ups and downs and is a more volatile stock. For example, issues with the SERVE-HF clinical trial saw its share price tumble from over $9.00 to around $7.00 in April.

Resmed – September 2010 to September 2015

On Friday’s close of $7.05, Resmed is trading at a 21.0% discount to the broker consensus target price of $8.53. Sentiment is marginally positive (four buys/two holds/two sells), and the PE for FY16 is down to 18.6.

Notwithstanding the significant discount to valuation, the brokers remain wary of competitor activity and the impact of this on sales and margin. A little more speculative, but worth the risk.

All charts sourced at: Yahoo!7 Finance, 21 September 2015

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.