Although the interest rate cycle has begun pushing upward in the US markets, there is still not much joy for Australian income investors.

As the official Reserve Bank of Australia (RBA) cash rate sank from 7.25% in 2008 to its record low of 1.5% – where it has now been since August 2016 – the salad days of average five-year term deposit rates offering 7.5%–8% a year (which investors were receiving as recently as 2010) have become a distant memory. The average five-year rate is now about 2.7%.

According to financial research firm Canstar, the average one-year term deposit rate is just under 2.5%, and the best you can do is 3%. For a three-year investment, the best rate is about 3.1%; for four years, it’s 3.2%; and for five years, it’s about 3.4%.

And with official inflation running at 2.1%, those returns don’t translate into alluring real returns.

That has been the situation for some time, but many yield-oriented investors have come to rely heavily on income from shares, through the largesse of the dividend imputation system, where a self-managed superannuation fund (SMSF) operating in accumulation phase, with a tax rate of 15% on earnings, receives a partial rebate of the franking credits attached to a fully franked dividend, because it does not need all of the franking credits to offset tax on the dividend.

An SMSF in pension phase (paying pensions to all members), with no tax on its earnings, receives a full rebate of the franking credits, because it has no tax to offset. For SMSFs, for now at least, a dollar of fully-franked income is effectively worth much more than a dollar. This could all change of course if Opposition leader Bill Shorten gets his way.

SMSFs have looked to stocks such as Telstra and the big four banks for gross yields in the range of 7.5%–9% – but over the last three years, for a variety of share market-wide and company-specific reasons, investors have re-learned the lesson of incurring capital risk. Telstra is down by 52% from its 2015 peak, and the big four banks are down anywhere from 28%–32% – heavily punishing investors who focused only on yield.

Yield-oriented investors and SMSFs have been forced to look elsewhere – to some well-known sources of yield, and to some newer avenues.

1. Peer-to-peer lending

Peer-to-peer (P2P) lending marketplaces have evolved through advances in financial technology, or “fintech.” They facilitate individual investors lending money to borrowers, and thus tap into one of the largest asset classes in the world – loans – which are typically held on the balance sheet of a bank.

P2P lending can be considered an extension of the spectrum of yield-bearing investments, where investors can get a greater return on their money – for taking a bit more risk – through the principal-and-interest return on loans, while also diversifying their income-generating portfolio. The attraction of this kind of investment is that it generates a return that is not correlated with the stock market.

There is a wide range of P2P lending marketplaces in Australia, offering investors the ability to fund property development loans, livestock loans for farmers, business loans and unsecured personal loans. Some of the P2P marketplaces offer unsecured loans, while some offer loans secured by a registered mortgage over the borrower’s real property. Some offer the ability to invest in a whole loan, some offer fractionation of loans and diversification across many different individual loans.

The point of P2P lending as an investment is that just as loans are assets on the balance sheet of banks or financial institutions, they can be assets owned by individual investors. P2P lending is investors lending money to borrowers without the direct intermediation of a traditional financial institution, such as a bank. The loan is transferred through an online platform, and is enabled by proprietary borrower assessment and credit-checking technology.

In most cases P2P lending is a combination of technology – the proprietary credit decision-making engine and the algorithms it uses – and traditional credit assessment skills. P2P lending platforms can play a role in opening-up another source of income, with which to diversify a yield portfolio more broadly. Investors must understand and accept that the investment is in consumer or business credit: this will provide a higher return than a term deposit or a government bond, but there is more risk than in those instruments. P2P lending is not guaranteed – although some P2P lenders have provision funds.

In Australia at present, the range of operating P2P platforms includes CoAssets, SocietyOne, RateSetter, Harmoney, Zagga, Moneyplace, Marketlend, MoneySpot, and True Pillars. Some (like Zagga) require investors to be “wholesale” investors, others accept minimum investment of $1000. Targeted returns are usually in the 6%–8% a year range, with returns on some loan types as high as 12%–15% a year – obviously, with higher risk.

P2P lending is not guaranteed, nor is it an inherently dodgy prospect. It is simply an investment exposure made possible by advances in financial technology.

2. Fine Art

Like many other “collectible” assets, fine art has always attracted some investment attention, being also uncorrelated with the traded stock, bond and property markets, and also a market that, while necessarily subjective, some knowledge can give an interested person an advantage.

In the right circumstances, art can be a perfectly sound and valid investment. It is a ‘real’ asset, it can help to diversify a well-constructed portfolio, it has capital gain potential and can also act as an inflation hedge.

A small proportion of SMSFs have owned art and other collectibles but the changes to the rules regarding “collectible” assets in SMSFs, which took full effect in 2016, hurt the sector. It virtually became too hard to hold these assets. However, in art specialist art investment consultants have sprung up to provide the missing element of recurrent income flow – through managing the rental of the investor’s art to galleries and for corporate display – while meeting all of the stringent ‘arm’s length’ and ‘no related-party use’ requirements of ownership. Beforehand, SMSF proprietors owning art were simply banking on capital gains on eventual sale – while paying insurance, storage and opportunity costs.

Through a specialist art investment consultancy such as Art Index, SMSFs can rent out their art and generate income returns in the range of 6%–9% a year, rather than just relying on the potential increase in value.

3. Unlisted property trusts and syndicates

With Australian listed real estate investment trusts (REITs) also prone to the price risk of the stock market, Australian property investors and SMSFs are increasingly keen to look at the unlisted market.

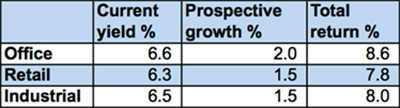

There, unlisted property trusts and syndicates offer income yields in the 6.3%–6.6% a year range, with distributions being paid from rental income, says property investment consultancy Atchison Consultants, with the ability for capital growth to augment this to 7.8%–8.6% a year.

Some of the trusts offer investment in portfolios, while some are syndicates that acquire a single designated property. These investments are illiquid, and thus investors must be very clear on their potential cash requirements while they invest, but for many, this is the attraction – the return is a ‘pure’ property return.

The trust will likely be geared, and investors must satisfy themselves that they are comfortable with this.

Like REITs, the unlisted trusts offer investment in areas of property that diversify investors away from residential property, with its (current) price risk and unappealing rental yields. Atchison Consultants sees the following returns – in % a year – as currently available in unlisted trusts and syndicates:

The minimum investment amounts for these sorts of vehicles are generally $5,000 to $20,000.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.