Basing investment decisions on top-down trends and ignoring valuations is a portfolio killer. Investors fret about the impact of rising interest rates or other variables and ignore valuation.

Take Australian Real Estate Investment Trusts (AREITs). Expectations of higher interest rates are a headwind for AREITs, utilities, infrastructure and other interest rate-sensitive sectors. Higher rates make their yields relatively less attractive and increase debt-servicing costs

Commentators have for the past 12 months warned investors to beware the “bond proxies”; for example, large AREITs that are have annuity-like cashflows and are bought mostly for yield. Their argument: the bond proxies outperform when rates fall and underperform when investors expect rates to rise.

There’s truth in that logic, but valuations matter most: that is, has the security’s price already captured, perhaps excessively so, expectations of higher rates?

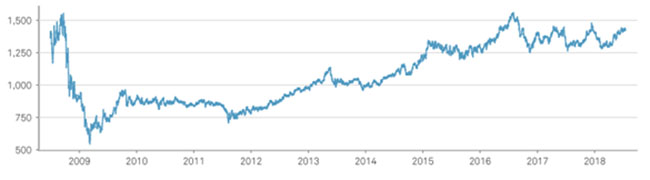

The S&P/ASX 200 AREIT sector’s total return of about 16% over one year compares to 13% for the S&P/ASX 200. Care is needed with the AREIT index, given the effect of the Rodamco-Unibail takeover of Westfield, a key index constituent this year. But it’s fair to say that index has held up better in the past few months than the AREIT bears expected.

Chart 1: S&P/ASX 200 AREIT index

Source: S&P

Be picky

That’s not to say investors should boost AREIT exposure. It’s hard to see the sector significantly outperforming the market, given expectations of another two US interest rate rises this year, and a higher Australian Government Bond 10-year yield.

Rather, select AREITs look interesting on valuation grounds after unit price falls. I wrote favourably about Westfield Corporation for the Switzer Report before its takeover and included another giant retail landlord, Vicinity Centres, in the takeover portfolio last week.

Niche AREITs are also worth consideration. Australia’s AREIT market mostly consists of trusts that hold office, industrial or retail property. A new breed of AREITs has emerged on ASX this decade through the initial public offering (IPO) market. They own data centres, childcare centres, retail warehouses, bulky goods, farms and other specialist properties.

Australia has relatively few niche property trusts compared to key REIT markets overseas. Unlike the United States, we do not have prison or student accommodation REITs. Prison REITs have ethical investment considerations: is it right to make money off incarceration? Student housing REITS would make sense in Australia given the size of our international education sector.

Nor does Australia have many self-storage, data centre or multi-family REITs that own lots of residential apartments and houses. I suspect that will change in the next decade as more niche REITs emerge to consolidate fragmented property sub-sectors.

Several niche AREITs have starred

I have identified promising niche AREITs for this report in the past five years: National Storage REIT in self-storage (NSR), ARENA REIT in childcare centres (ARF), Folkestone Education Trust (FET); Aventus Retail Property Fund in retail supercentres (AVN), Asia Pacific Data Centre Group (AJD); BWP Trust in hardware properties (BWP); and Rural Funds Group in farming (RFF).

National Storage, probably the pick of the niche AREITs, has a total return of 22% over one year. BWP Trust is up 19% and Arena is up 13%. Folkestone has delivered 10%; and Rural Funds Group and Aventus have returned 7% in 12 months.

The three-year performance is mixed: National Storage and BWP Trust have had single-digit returns over this period and the rest have mostly produced solid or strong gains. Asia Pacific Data has a 20% annualised three-year return; Rural Funds has delivered 31%.

There’s more growth in niche REITs – and risk – given they are targeting fragmented sectors or sector with higher growth prospects.

I still like the thematic behind National Storage. The REIT, Australia’s largest self-storage owner-operator with 127 centres, is a long-term play on population growth and urbanisation. As more people live in cramped city apartments, demand for storage space will rise.

The local self-storage market is highly fragmented. The top three operators have an estimated 25% share of a $12-billion market. Supply of self-storage facilities is constrained because large centres, in inner-city locations, are dear to build.

National Storage can continue to grow through acquisitions and organically. A more transient labour market and homeowners renting storage space when they renovate or move, are demand drivers for storage, as is growth in online retailing. Smaller online retailers are renting self-storage space to house their inventory – a trend that is evident overseas.

Against this, a housing slowdown could reduce property turnover and storage demand. Longer term, the industry has low product differentiation, brand loyalty, low pricing power and has faced savage pricing wars over the year. Still, the tailwinds for National Storage REIT over the next five years should offset these challenges.

National Storage looks fully valued after recent price gains, which partly came on the back of news of the company’s debt refinancing. An average price target of $1.52, based on the consensus of six broking firms, suggests is it expensive. Morningstar values the REIT at $1.50.

I would not be surprised to see a larger US REIT snap up National Storage, given its market-leading position. Either way, the REIT has good medium-term growth prospects and is one to watch on any significant price pullback this year.

Chart 2: National Storage REIT (NSR)

Source: ASX

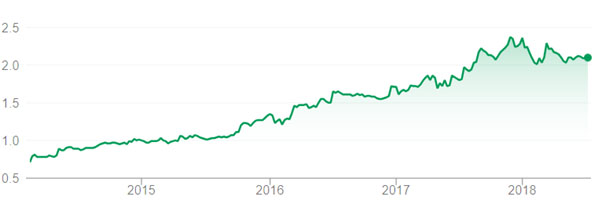

Rural Funds Group (RFF) is among my favoured niche AREITs. The $515-million property trust has starred over the past three years, its unit price doubling.

The well-run AREIT owns a portfolio of 38 agricultural assets that are leased to farmers. Half of the assets are for almond farms, a fifth for poultry and the rest across cattle, vineyards, cotton and other sectors. Most of its key properties are in the southern states.

Like National Storage, Rural Funds Group has plenty of acquisition opportunities, as it buys and consolidates smaller farms. It has made at least eight acquisitions since 2014 and will make more as its looks to complete a $149.5-million equity capital raising in July. Rural Funds is acquiring five feedlots and cropping land for $52.7 million from JBS Australia.

The trust is almost providing a $75-million guarantee to a subsidiary to enable JBS to replace an existing agreement for the supply of cattle and for its grain feed business.

Three main factors support my positive view on Rural Funds. First, its diversification across sectors and states means it is less affected by a climatic event in one area. I would like to see Rural Funds reduce its almonds exposure over time, but that has worked well for it to date.

Second, Rural Fund’s Weighted Average Lease Expiry (WALE) at 12.5 years is among the longest in the AREIT sector. Locking tenants into lengthy leases increases Rural Fund Group’s earnings and distribution certainty and reduces its risk profile. Tenants include some of ASX’s largest listed agricultural companies.

Third, I like how Rural Funds is buying larger farms and investing in them to improve performance through better water points, cultivation area, pastoral improvements or access. Done well, the strategy eventually leads to higher market rents when leases are reviewed.

Rural Funds has a higher risk profile than larger REITs, despite its long-term leases. It pays out less of its earnings as distributions (79%) compared to many REITs. However, I like that Rural Funds is reinvesting more of its profit to drive growth, but conservative income investors might prefer REITs with higher distribution payout ratios and yield.

Rural Funds has a reasonable amount of debt for its size; the gearing ratio is 37.4%. That is manageable given an interest cover ratio of 4.8 times and the trust’s lease profile.

Long-term investors might wait to see where Rural Fund’s price settles after the capital raising (the offer price is $1.95 per new unit). I suspect there could be modest price weakness in the next few months given the raising and after a strong price rally last year.

Rural Funds is due for a longer period of price consolidation or a pullback, but remains one of the higher-quality niche AREITs and a contender for portfolio watchlists.

A handful of brokers who cover the trust (too small to rely on) have an average price target of $2.14. That looks reasonable over 12 months.

Rural Funds would look more attractive at or below $1.95. At the current $2.02, the trust is expected to yield about 5% in FY19, using consensus estimates.

Chart 2: Rural Funds Group (RFF)

Source: ASX

Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor All prices and analysis at July 18, 2018.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.