Treasury Wine Estates (TWE) delivered an excellent set of first half numbers and remains a core long-term holding in my opinion. In fact, I am of the view TWE is the number one alcoholic beverage exposure in the world due to its unique nature as a pure premium wine exposure. All other alcoholic beverage stocks we look at either have lower margin beer or spirits in their portfolio, which reduces their attractiveness.

TWE shares had rallied hard so far in 2017, and it wasn’t unsurprising to see a slight pullback in the stock in reaction to confirmation of strong earnings. A classic ‘sell the fact’ response from the trading community and fast money which provides another buying opportunity for investors in what I believe is a structural global growth stock.

Let’s look at the highlights of the 1H result:

Reported net profit after tax $136.2m, more than double the prior year.

Reported Earnings Per Share (EPS) 18.5 cents per share, more than double prior year.

Reported EBITS $226.8m , up +59%, higher than full year 2015 EBITS.

All regions delivered double digit EBITS growth in 1HFY17

EBITS margin accretion reported: up +4.3ppts to 17.5%

Strong cash conversion at 104%

Interim dividend 13.0 cents per share, unfranked. 5 cents higher than the prior period (+63%)

High teens EBITS margin expected by FY18.

While expectations were high for the TWE result, the result clearly beat consensus expectations and has led to +4% to 6% upgrades to FY17 full year numbers by the analyst community. These consensus earnings forecast upgrades were essential for the outperformance of TWE shares to continue.

TWE consensus FY17 EPS forecasts: going up

Without doubt, the highlight of TWE’s very strong 1H17 result was its Asian performance. EBITs grew at +76% year on year and +39% half-on-half. Volumes grew +42%.

The analyst community and myself expect this to continue. There are a number of drivers of this and I will quote directly from Morgan Stanley research on these points.

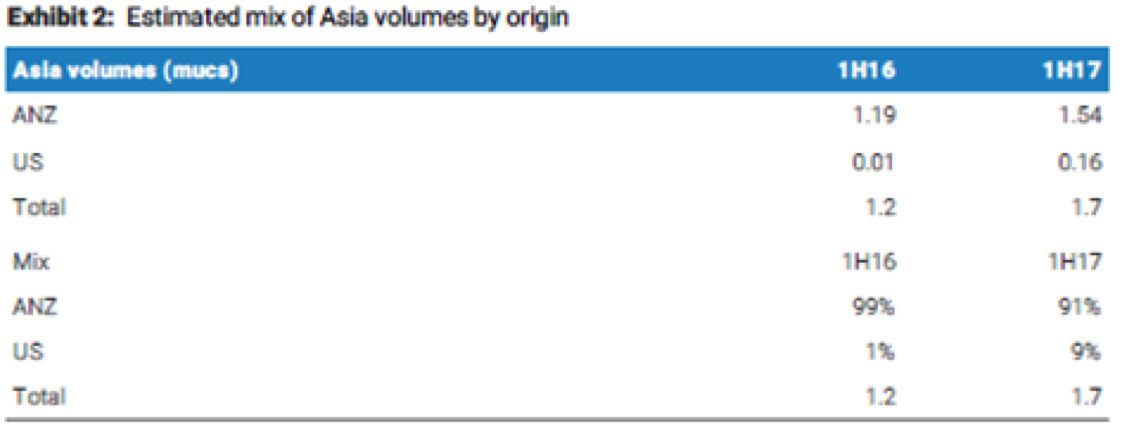

1. The launch of TWE’s American-made wine in November which still only represents a single-digit share of total Asia volume. As we show in the exhibit below, we think Asia ANZ-made wine is 10x the volume of US-made wine. Clearly there is a significant opportunity to grow US-made wine into Asia.

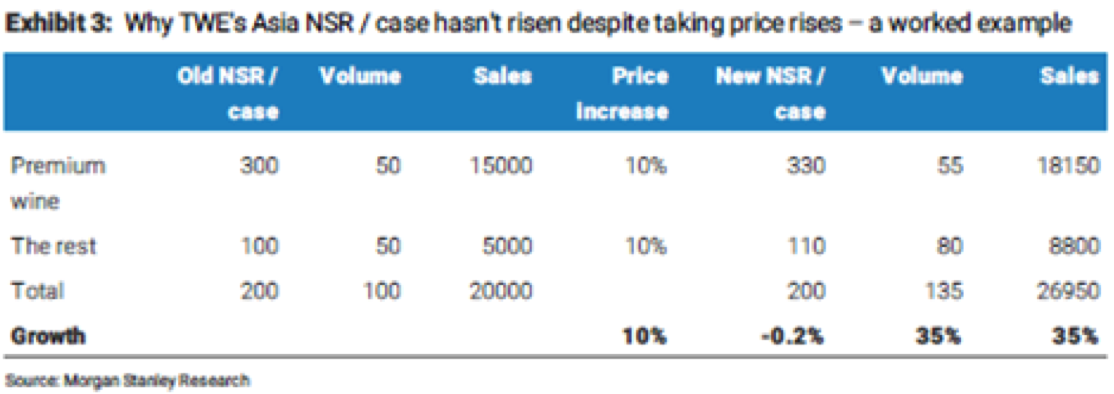

2. Price increases taken on flagship Penfolds and Wold Blass products. Asia NSR per case reduced from $130 to $128 on category mix, hence price rises aren’t as visible as they might have otherwise been.

We see structural growth into the Asian “masstige” market.

The other clear opportunity for TWE is turning around its US division.

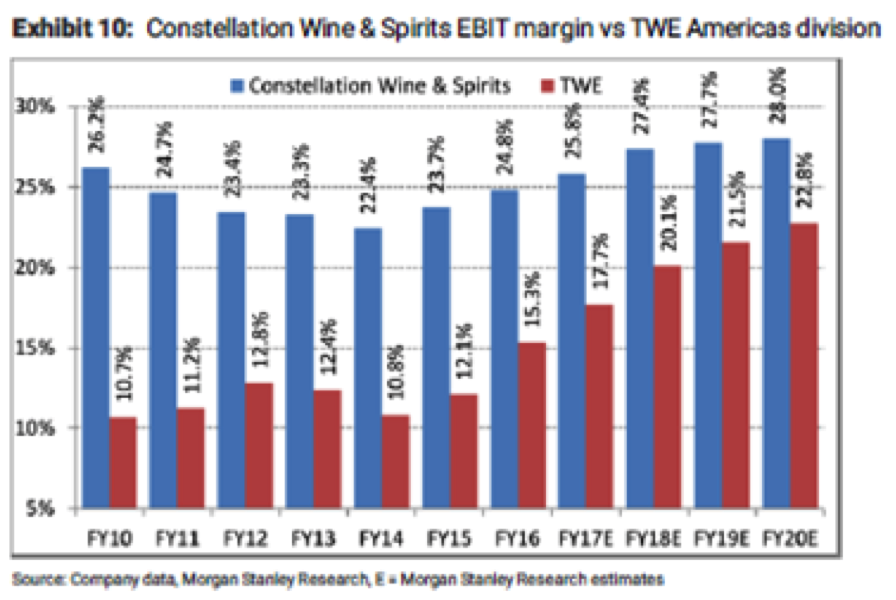

It’s worth noting that TWE’s US margins are currently well below peer Constellation Brands (STZ.US).

Constellation Brands recently gave the market guidance for its wine and spirits business for FY18 to 20. They expect low to mid-single digit volume growth, mid-single digit sales growth, and mid to high single digit EBIT growth. The company expects margins in the America’s business to expand to 28% by FY20. This compares with the 1HFY17 EBITS margins of 16%.

While Constellations business is larger in size, we believe that premiumisation, faster growth in the US wine category as well as supply chain initiatives and cost outs will help close some of the gap between Constellation’s margins and TWE’s, in favour of TWE.

Similarly, we wouldn’t be surprised to see TWE make another major US acquisition in the next few months to build scale. It’s interesting that CEO Michael Clarke will be splitting his time between the US and Australia from now on. My fund would support a TWE issue to buy more scale in the US.

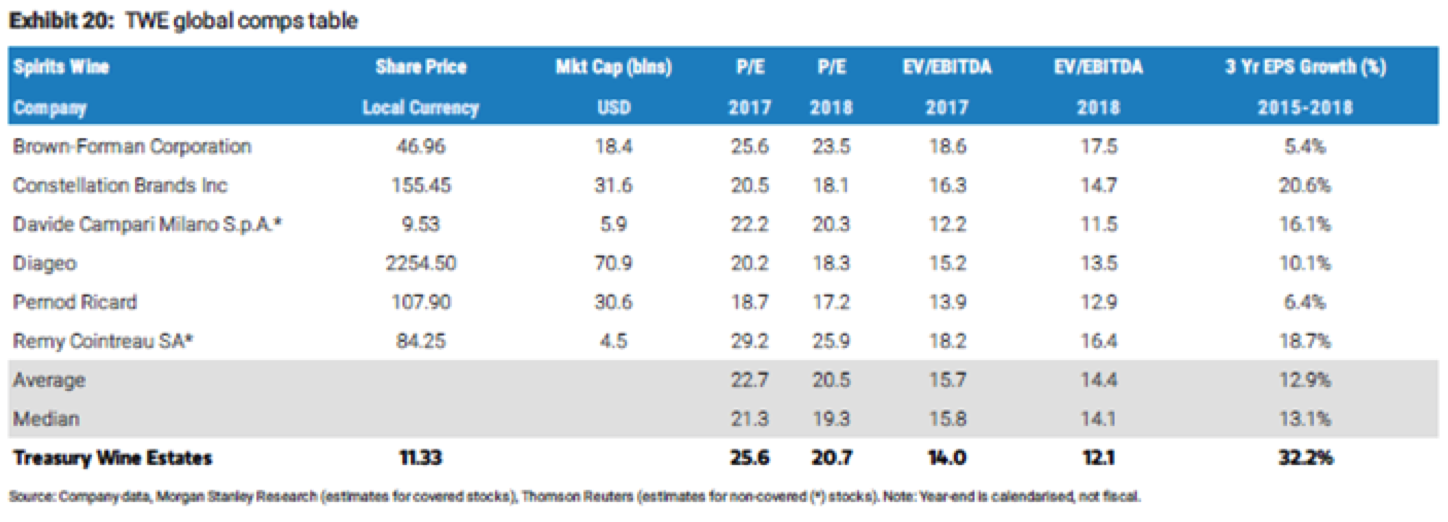

The table below compares investment metrics for TWE’s global peer group. You can see the stock ranks well on relative valuations and compound EPS growth forecasts

All in all, the TWE result was excellent and confirms my view that this is a structural growth stock in a structurally growing sector. Management continues to execute the growth strategy very well and shareholders are being rewarded with earnings and dividend growth.

I believe this is going to continue and I think the stock has the potential to surprise us all on where it heads to over the next three years. I am of the view it will be re-rated to a global luxury goods multiple, particularly given its increasing leverage to the high-end Asian consumer.

Morgan Stanley finished their post results research note with the following: I agree with this thesis.

We lift our price target from A$13 to A$14 on 2% EBIT upgrades across FY17-FY19e and on lifting our long-term (FY28) EBITS margin forecast from 26% to 27%. We view valuation as attractive at 22.5x FY18e P/E, which compares with global peers trading on 18-28x P/E in light of TWE’s expected FY16-FY20e EPS CAGR of c.20%. As consensus lifts earnings forecasts, we see the shares outperforming.

Let your winners run: TWE is a winner.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.