What is the stock?

EML Payments Limited (EML:ASX) operates the technology behind prepaid gift and corporate cards. The company began in the retail sector before expanding into other verticals – the most successful being the winnings card for online bookmakers. More recently EML has successfully expanded into the UK, European and North American markets.

How long have you held the stock?

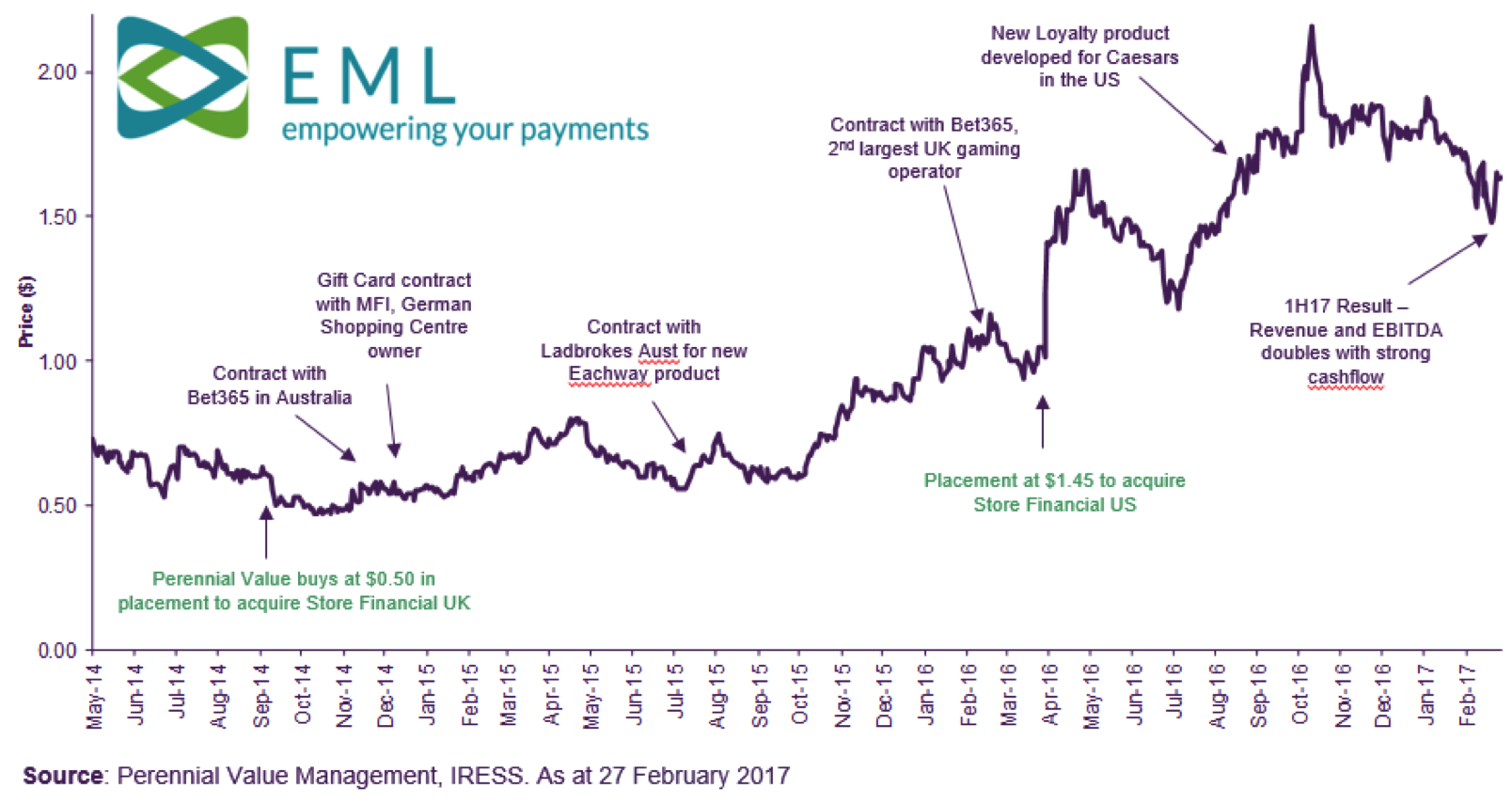

Our Smaller Companies Trust first invested via a placement at 50 cents in September 2014 with the proceeds used to fund the UK Acquisition.

Post the recent US Acquisition and contract wins, we have added the stock as a high conviction idea to both our Wealth Defender and Micro Cap Opportunities Trusts.

What do you like about it?

While earnings doubled in the 1HFY17 result, there are still multiple growth options from many regions, such as:

- UK gaming sector, this is 4 times larger than Australia where EML dominate

- Loyalty programs, Caesars in the US is the first significant customer

- B2B payments in the US, already handling over $1 billion in payments

- Salary Packaging Cards in Australia, due to regulatory change EML will become market leader from 1 July 2017 as the banks exit the sector

Despite EML becoming a more diverse business, it has been de-rated by the market recently, creating an attractive investment proposition.

How is it better than its competitors?

EML is more nimble and innovative than many large competitors.

What do you like about management?

MD Tom Cregan owns 8.1% of EML and has a strong track record in the industry. Through the UK and US acquisitions, he has also added to, and been able to retain, a strong management team.

What is your target price?

At $2.20, EML would be on a market multiple based on our FY19 earnings forecast.

At what point would you sell it?

We would reduce our position when the growth prospects of EML are fully captured by the market.

Where do you see the value?

The market seems to be overly concerned with the exposure of EML to the fluctuations in the British Pound (GBP) post Brexit. While this impacted earnings by 10% at the 1HFY17 result, earnings still doubled, as it was more than offset by growth in other areas of the business. Growth in Salary Packaging in Australia and the US business will further reduce the exposure to the GBP going forward.

We see EML as lower risk relative to several years ago, with a more diverse business across multiple verticals and regulatory environments.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.