A strong final week helped our portfolios add around 3% in March, as the Australian market broke through 5800 and finished firmly in the black. For the first quarter of 2017, both portfolios have returned more than 4%.

This is our third monthly review. On a relative basis, the income portfolio has underperformed the index this year by 0.69% and the growth portfolio by 0.15%.

The purpose of these portfolios is to demonstrate an approach to portfolio construction. As the rule sets applied are of critical importance, we provide a quick recap on these.

Portfolio recap

In January, we made some adjustments to our Australian share ‘Income Portfolio’ and ‘Growth-Oriented Portfolio’ (see here and here).

To construct the income portfolio, the processes we applied included:

- we used a ‘top down approach’ looking at the industry sectors;

- so that we are not overly exposed to a market move, we have determined that in the major sectors (financials and materials), our sector biases will not be more than 33% away from index;

- we require 15 to 20 stocks (less than 10 is insufficient diversification; over 25, it is too hard to monitor), and have set a minimum stock investment of $3,000;

- we confined our stock universe to the ASX 150;

- we have avoided stocks from industries where there is a high level of exogenous risk, such as airlines;

- for the income portfolio, we prioritised stocks that pay fully-franked dividends and have a strong earnings track record; and

- within a sector, the stocks are broadly weighted to their respective index weight, although there are some biases.

The growth-oriented portfolio takes a different approach in that it introduces biases that favour the sectors that we judge to have the best medium term growth prospects. Critically, it also confines the stock universe to the ASX 150 (there are many great growth companies outside the top 150).

Overlaying these processes are our predominant investment themes for 2017, which we expect to be:

- Interest rates remaining at low levels, although some upward movement in bond rates;

- The US Fed likely to increase US interest rates by 0.75%, but probably no move in Australia by the RBA;

- The Australian dollar at around 0.70 US cents to 0.75 US cents, but with risk of breaking down if the US dollar firms;

- Commodity prices remaining reasonably well supported;

- A positive lead from the US markets and President Trump;

- A moderate pick-up in growth in Australia back towards trend levels; and

- No material pick up in domestic inflation.

Performance

The income portfolio to 31 March is up by 4.13% and the growth-oriented portfolio by 4.68% (see tables at the end). Compared to the benchmark S&P/ASX 200 Accumulation Index (which adds back income from dividends), the income portfolio has underperformed the index by 0.69% and the growth-oriented portfolio by 0.15%.

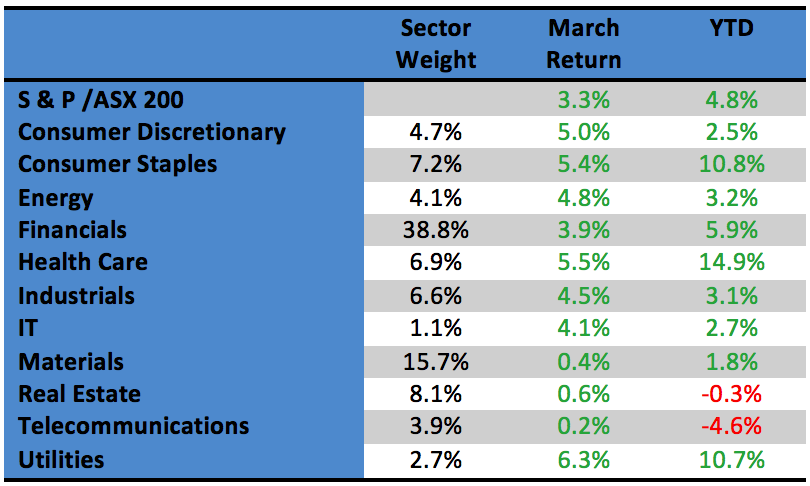

All sectors positive in March

All industry sectors on the S&P/ASX 200 finished with small gains in March, with health care the best at 5.5% and telecommunications the worst at 0.2% (see table below). Year-to-date, health care remains the best performing sector with a return of almost 15%, a reversal of a very disappointing final quarter of 2016.

Consumer staples, which was a laggard sector in 2015 and 2016 mainly on the back of the supermarket wars, continued its recent strong performance, adding 5.4% in March. This took first quarter gains to 10.8%.

The largest sector on the ASX, financials, which makes up 38.8% of the S&P/ASX 200 by market weight, returned 3.9% in March to be up by 5.9% for the year. A more stable capital outlook has led investors to re-assess this sector.

While the materials sector finished marginally positive in the month, year-to-date gains are below the broader market at just 1.8%, as the iron ore price (in particular) pulls back from recent highs. Including dividends, BHP is down 2% year-to-date, while RIO has returned 3.7%.

Finally, in a market where differences in sector performances are by historical standard quite small, the telecommunications sector is the worst performing sector this year, with a return of minus 4.6%. A disappointing profit report from Telstra, plus a market view that competition for mobile and NBN customers will compress margins, is leading some investors to reduce exposure to this sector.

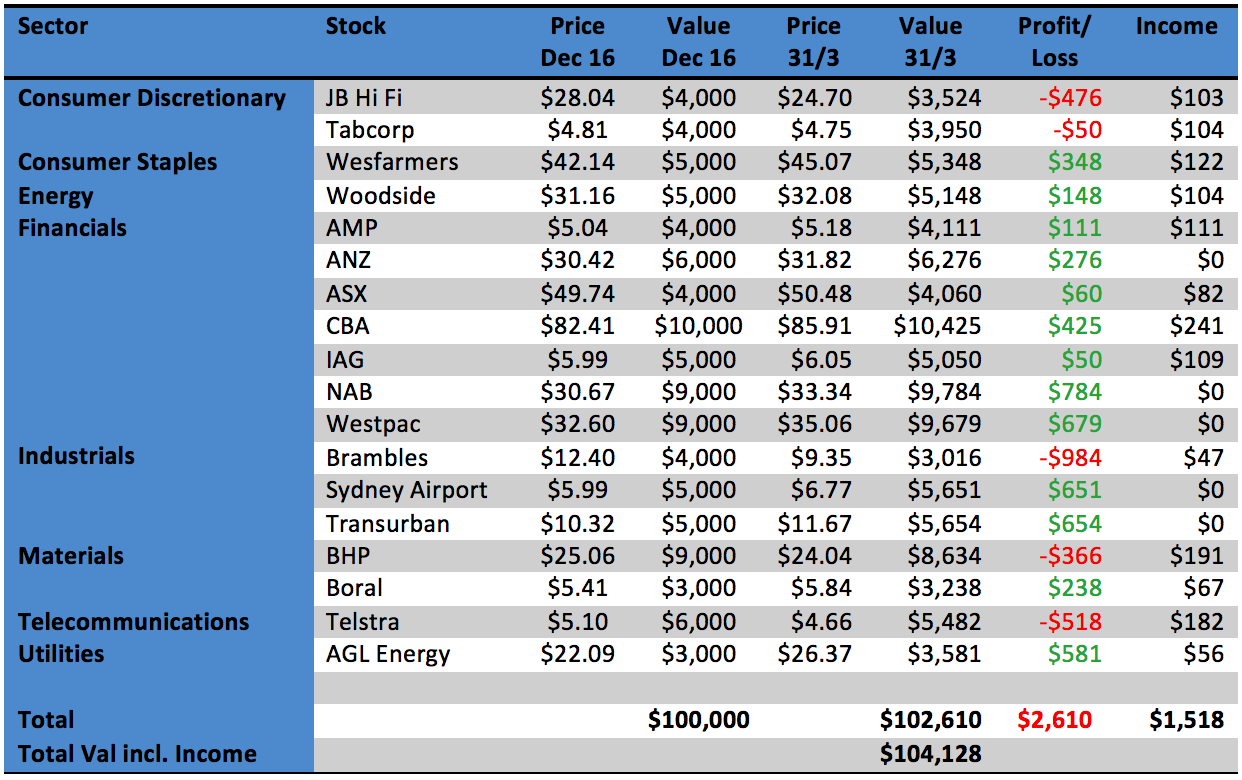

Income portfolio

The income portfolio is underweight materials stocks and marginally overweight financial stocks. Otherwise, the sector biases are relatively small. We have avoided real estate (potential impact of higher interest rates, plus lack of franking on real estate investment trusts), and healthcare (low dividends and pricing multiples).

The income portfolio is forecast to generate a yield of 4.90% in 2017, franked to 87.3%. The inclusion of Transurban and Sydney Airport, while adding to the defensive qualities of the portfolio, drags down the franking percentage.

In a bull market, we expect that the income-biased portfolio will underperform relative to the S&P/ASX200, due to the underweight position in the more growth-oriented sectors and the stock selection being more defensive, and conversely in a bear market, it should moderately outperform.

Year-to-date, the portfolio has returned 4.13% compared to the accumulation index return of 4.82%. While the portfolio has benefitted from its overweight position in financial stocks, it hasn’t been able to benefit from the performance of the healthcare sector. The performance of Brambles following disappointing profit guidance has impacted the return, as has the performance of Telstra, which is under considerable pressure to grow revenue. JB Hi-Fi, despite turning in one of the best results in the profit reporting season, has been impacted by the “Amazon” concerns that are affecting discretionary retailers. To some extent, these negative impacts have been offset by the performances of Transurban, Sydney Airport and AGL.

No changes to the portfolio are contemplated at this point in time, although we are keeping our exposure to Brambles under close review.

The income-biased portfolio per $100,000 invested (using prices as at the close of business on 31 March 2017) is as follows:

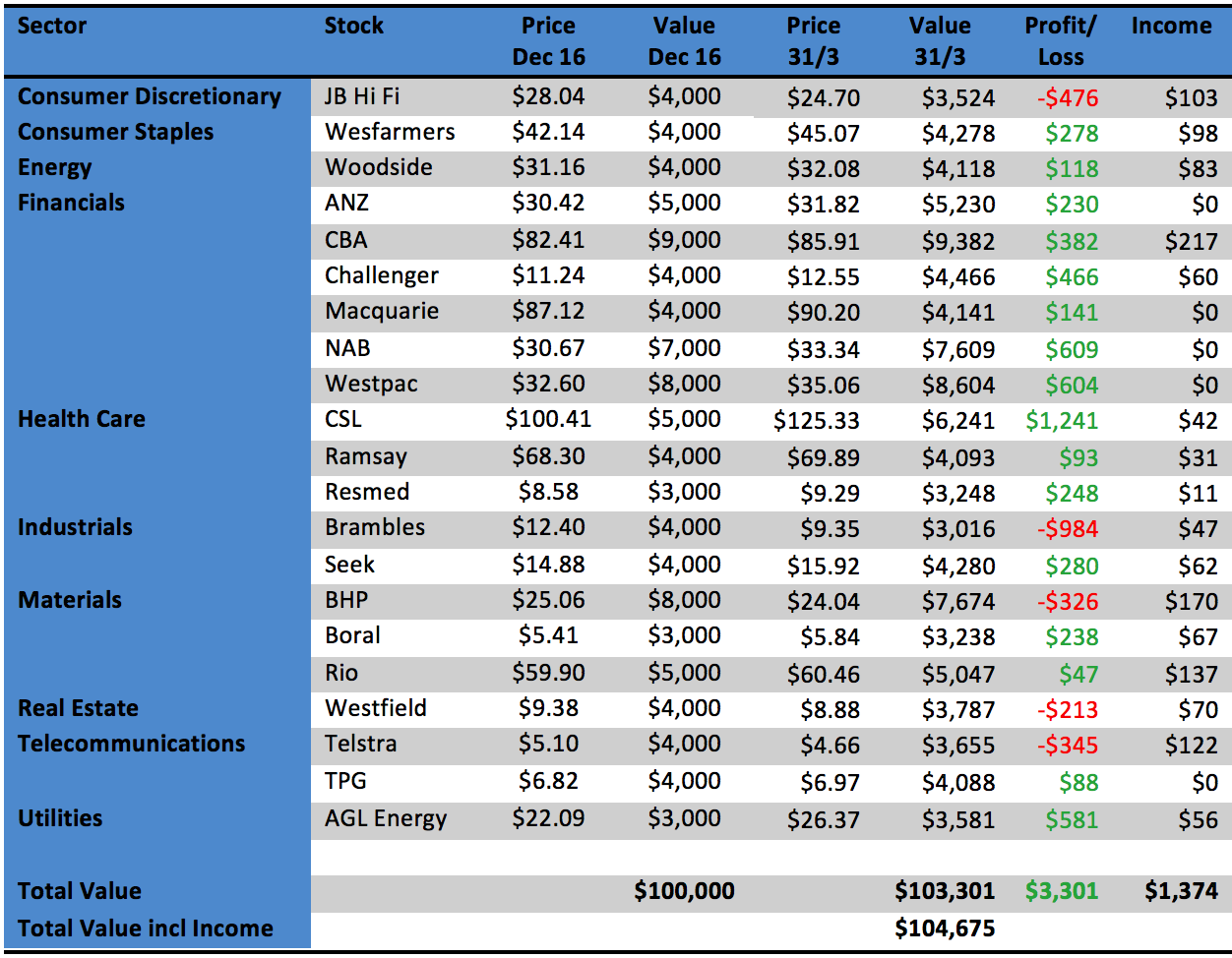

Growth portfolio

A critical construction decision with the growth portfolio has been to take a neutral sector bias in the materials sector. This has led to the inclusion of Rio (along with BHP and Boral).

Overall, the sector biases are relatively small. Despite healthcare underperforming in 2016 and many of the stocks trading on high multiples, we believe that the tailwinds are so strong that our sector position is materially overweight.

The other overweight position is in telecommunications, the only negative performing sector in 2016. The major underweight positions are in real estate and consumer staples.

The stock selection is biased to companies that will benefit from a falling Australian dollar – either because they earn a major share of their revenue offshore, and/or report their earnings in US dollar. While we expect that the Aussie dollar will remain well supported and trade in a fairly narrow range in the short term, the risk is that a strengthening US dollar causes it to break down.

Year-to-date, the portfolio has returned 4.68% compared to the accumulation index return of 4.82%. The overweight position in healthcare, in particular with CSL and Resmed, is adding to portfolio returns. On the negative side, the holding in Brambles is detracting most from the portfolio, together with the overweight position in telecommunications. Also, with the Aussie dollar above 75 US cents, our stock selection is yet to pay dividends.

No changes to the portfolio are contemplated at this point in time, although we are keeping our exposure to Brambles under close review.

Our growth-oriented portfolio per $100,000 invested (using prices as at the close of business on 31 March 2017) is as follows:

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.