It is not often that you get such divergent views from stockbroker analysts about a highly traded company. UBS says that buy now, pay later company Zip Co (Z1P) is a ‘sell’ and has a target price of just $1.00, 38.6% below where it closed yesterday at $1.63. Meanwhile, Ord Minnett and Morgans both have ‘buy’ recommendations and target prices near $4.00, implying potential upside of 145%.

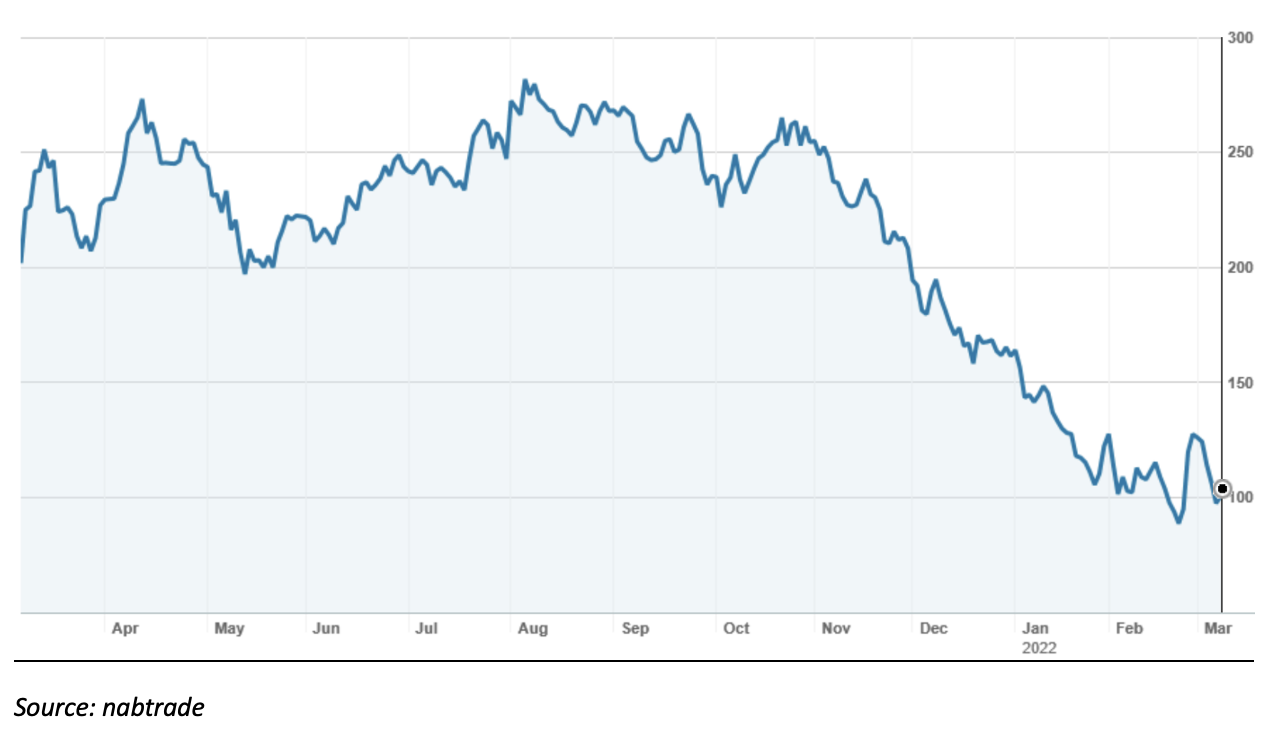

And $4.00 is still less than half the price Zip was trading at 12 months ago. It has been absolutely smashed, losing 81.4% over the last 12 months and 62.4% since the start of 2022.

Zip Co (Z1P) – last 12 months

But it is not the only payments company to be smashed. The whole global payments sector has ‘de-rated’ as investors switch out of “high growth, low earnings” companies and “over-hyped” sectors. Global leader PayPal, for example, is down 58.0% over the last 12 months and 49.7% since the start of the year.

PayPal Holdings (PYPL) – last 12 months

Block Inc (formerly called Square), which acquired Zip’s most direct competitor in Australia, Afterpay, has fared relatively better – losing 50.2% over the last 12 months and 37.7% since the start of the year.

Block (SQ) – last 12 months

So what do the brokers say about Zip?

UBS was disappointed with Zip’s first-half result where higher bad debts, higher operating costs and a small deterioration in margin led to a loss of $108.1 million for the period (EBITDA). This was despite some very impressive growth in business metrics (see below). Paraphrasing the UBS research report, FNArena wrote:

UBS updates forecasts to allow for Zip Co’s unexpected -$108m negative 1H cash earnings (EBTDA), when the broker had forecast breakeven. In addition, the $150m-$200m capital raising and proposed merger with Sezzle (SZL) are taken into account.

As a result, the target price is slashed to $1 from $5.20 reflecting lower long-term profit forecasts, dilution from the capital raise and the application of a higher discount rate. The latter reflects a longer path to breakeven and overall uncertainty.

Referring to the acquisition/merger of Sezzle, FNArena’s summary of Ord Minnett’s view is:

Ord Minnett sees sound strategic merit in Zip Co’s proposed merger with Sezzle (SZL). The US active customers will jump to around 8m from 5.7m providing greater network effects, as well as providing increased value add to new merchants.

Following the recently completed $148.7m placement, the broker estimates current cash reserves should see the company through to positive cash earnings (EBTDA) in FY25. Management has a shorter time frame (FY24) to reach cash earnings profitability.

The all scrip merger with Sezzle will see Zip’s business shift to focus on the US. 60% of transaction turnover will be generated from the US, with Australia accounting for 38% and other countries 2%. Customers will increase from 9.9 million to 13.3 million and merchants from 81.8K to 128.8K. In the key US market, where Sezzle was predominately based, the number of merchants will jump from 18.5K to 60.5K.

Financially, the transaction is expected to generate about $130 million of EBITDA in FY24. $60-$80 million is estimated to be cost synergies, the rest from increased earnings as Zip rolls out its entire product range to the Sezzle merchants and customers.

While disappointed with the first-half financial result (the size of the loss came as a surprise), the major brokers are generally positive about the merger. On consensus, the target price for Zip is $2.59, some 58.9% higher than yesterday’s close. The table below shows the individual recommendations and target prices.

Broker Recommendations and Target Prices

Bottom line

Bottom line

I don’t know whether anyone really knows how to value a company like Zip. I like to believe that a company that traded over $10.00 last April has to be interesting less than 12 months later at $1.63. Moreso because the company has done nothing wrong in that period. It may not be a “blue-chip”, but it is the number two local player and will be the number 4 or 5 in the US in the rapidly expanding buy now, pay later segment. Over the last 12 months, revenue grew by 89%, transaction turnover by 93%, the number of transactions by 147%, customers by 74% and the number of merchants by 113%.

I am comforted that the company took the opportunity to raise $148.7 million of new capital in conjunction with the all scrip merger with Sezzle, and will raise more by way of a share purchase plan to retail shareholders. This means that the company shouldn’t have to come near the market again for some time.

I am comforted that the founders, Larry Diamond and Peter Gray, have bought shares on market in the last week, along with most of the non-executive Directors.

I am comforted by the public commitment of Management to “refine their priorities with a focus on accelerating our path to profitability”.

A speculative buy.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.