Five weeks ago, I wrote about Telstra under the heading “is Telstra buy, yet?” (see here). In response to the question, I concluded with the following:

“Well, I think it depends on who you are. If your priority is income, then around $4.50 to $4.60 isn’t too bad a level to get set at. But I also think you can be patient, I don’t get a sense that Telstra is going to run away from you. So, you can perhaps target multiple entry points.

“If your priority is growth, look elsewhere.”

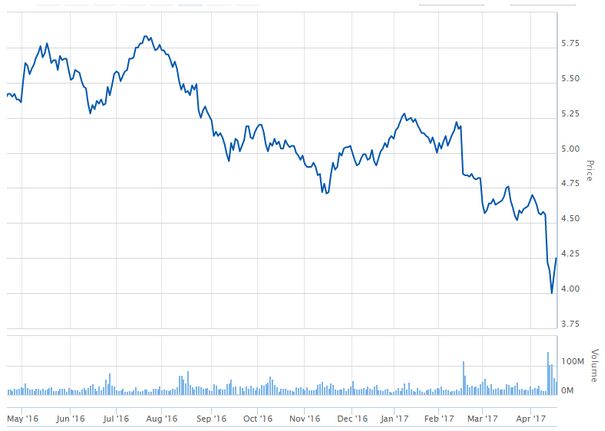

On Tuesday last week, Telstra touched $4.00 (very briefly), before rallying quite strongly to close Friday at $4.23. This is still, however, some way below the first entry point for income investors of $4.50 to $4.60. So, what’s changed?

Telstra Share Price – April 16 – April 17

Source: asx.com.au

TPG and the ACCC

There has really only been one change, and that is the announcement by TPG that it has outlaid $1.26bn to buy mobile spectrum in the key 700MHz range, and that it will spend another $600m over a three-year period to build a mobile network that covers 80% of the population. It will be Australia’s fourth mobile network, after Telstra, Optus and Vodafone.

Because Telstra has the largest share of the mobiles market, and earns a premium price from many customers, it is seen as the most exposed to a carrier like TPG that might fight hard on price to win customers. The mobiles business accounts for 39% of Telstra’s revenue, and a little over 40% of group EBITDA.

While many analysts think that $600m capital expenditure by TPG over three years won’t build much of a network, the threat was enough to send Telstra’s shares into a spin. This news has been compounded by ongoing discussion on whether the ACCC might declare domestic roaming.

This isn’t new news, but the decision is drawing closer. Last September, the ACCC commenced an inquiry into whether domestic roaming should be declared. If this occurred, Telstra would be required to provide access to its mobile towers to other carriers, such as Vodafone and TPG. This isn’t a big deal in the cities, but in regional and remote Australia where Telstra’s coverage is materially better, this would provide its competitors with a big lift and close the competitive gap. While Telstra would earn a fee from providing the roaming access, the fee would be set by the ACCC.

Some analysts argue that TPG’s initiative to build a network makes a declaration more likely, others say that this is proof that competition thrives and that the ACCC doesn’t need to intervene. The decision, however, gets closer, with some tipping an announcement within the next couple of weeks.

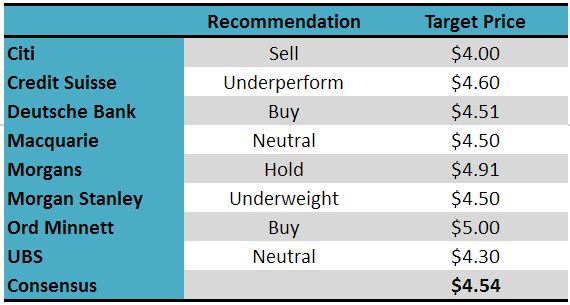

Further, in response to these influences, the analysts have cut their target prices. The consensus now sits at $4.54, compared with $4.82 last month (see below).

And there has been no update on how Telstra is addressing its NBN woes (see https://switzersuperreport.com.au/is-telstra-a-buy-yet/), or any outcomes from its capital allocation review.

The Brokers

With the price fall, broker sentiment has improved, although it remains negative over all. According to FNArena, of the eight major brokers, there are two buys, three neutrals and three sells.

The main concerns relate to the NBN earnings hole and Telstra’s ability to close it, the sustainability of the dividend, and the looming decision from the ACCC. Individual recommendations and target prices are as follows:

Broker Recommendations and Target Prices

The Brokers have Telstra trading on a multiple of 13.4 times forecast FY17 earnings and 12.6 times FY18 earnings. They forecast a dividend of 31.0c fully franked in FY17, and 31.1c in FY18. At a price of $4.23, this puts Telstra on a forecast dividend yield of 7.3% pa (10.5% pa grossed up).

Is the dividend sustainable?

Despite only generating $1.4bn in free cash flow in the first half, Telstra says it is on track to deliver $3.5bn to $4.0bn free cash flow for the full year. Free cash flow is the cash generated from operations less capital expenditure, but before payment of the dividend. Telstra’s dividend bill is around $3.6bn.

However, the problem for Telstra from a cash flow perspective is not FY17 or FY18, but in the later years when the NBN earnings hole grows deeper, and the impact of any new competitor such as TPG on its mobiles business is going to be felt. The issue for Telstra is whether it should cut the dividend now, allowing it to further increase capital expenditure or strengthen its balance sheet, or just continue to pay out at the same rate and work on its plan to address the earnings hole.

My guess is that the noise for a cut in the dividend from institutional shareholders and analysts will grow louder. Many will point to the BHP example, where the abandonment of its crazy progressive dividend policy was virtually the turning point in its share price decline.

The finalization of the capital allocation review may well be accompanied by an announcement that the dividend is being cut.

Bottom line

So, is Telstra a buy, yet, again?

I haven’t changed my view that growth-focused investors should look elsewhere.

For income investors who are filling up on Telstra, I think you can be patient and target the next buy level around $4.00. I think that there will be a massive amount of support around this level, and if you factor in a dividend cut from 31c to say 20c a share, which would give Telstra an extra $1.3bn to invest, it would still yield a handy 5% fully franked.

Should you chase Telstra? Well, my inclination is to be patient as I don’t think market sentiment has changed and a re-rating in the near term is unlikely. If one or more of the following happens, then it is a different ball game:

- Telstra announces a dividend cut (I think this would be a positive);

- The ACCC announces that it won’t declare or intervene in roaming services (probably unlikely, given the recent history of ACCC interventions going against Telstra); or

- Telstra shows credible progress on closing the NBN earnings hole.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.